|

|

|

|

|||||

|

|

|

As the Q3 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the data storage industry, including Snowflake (NYSE:SNOW) and its peers.

Data is the lifeblood of the internet and software in general, and the amount of data created is accelerating. As a result, the importance of storing the data in scalable and efficient formats continues to rise, especially as its diversity and associated use cases expand from analyzing simple, structured datasets to high-scale processing of unstructured data such as images, audio, and video.

The 4 data storage stocks we track reported a strong Q3. As a group, revenues beat analysts’ consensus estimates by 2.6% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 3.7% on average since the latest earnings results.

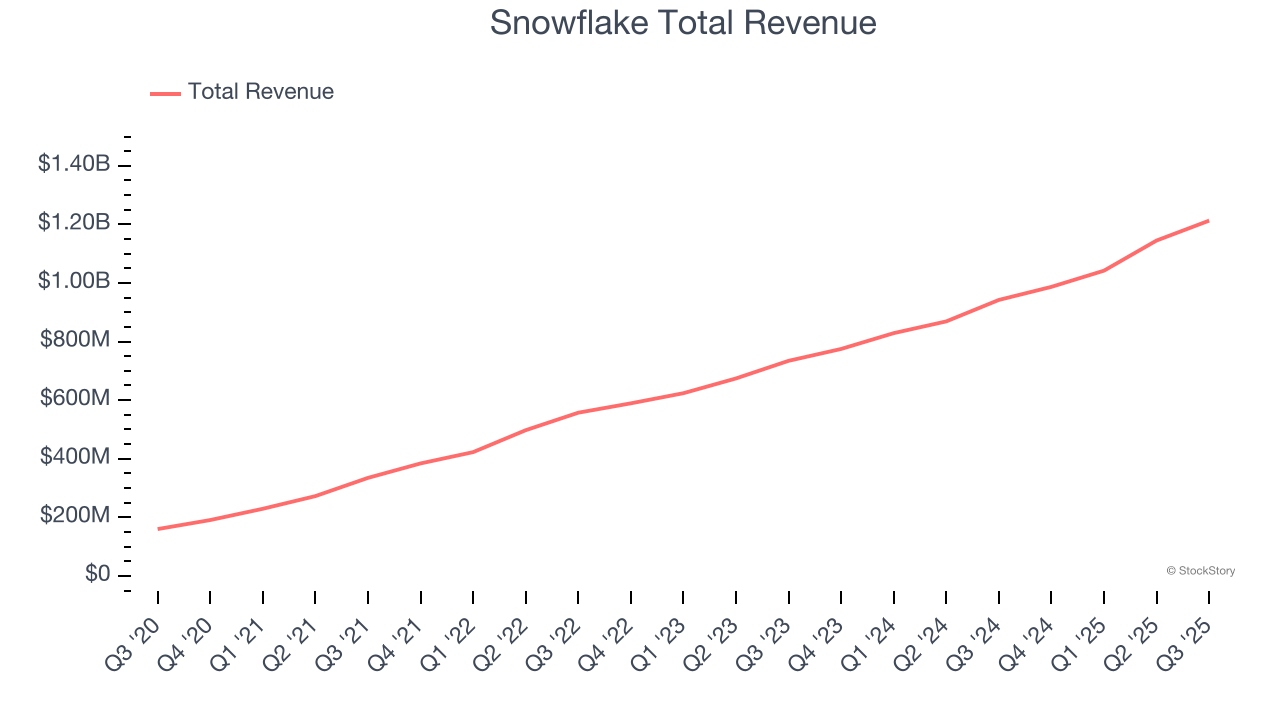

Named after the unique architecture of its data warehouse which resembles a snowflake pattern, Snowflake (NYSE:SNOW) provides a cloud-based data platform that enables organizations to consolidate, analyze, and share data across multiple cloud providers.

Snowflake reported revenues of $1.21 billion, up 28.7% year on year. This print exceeded analysts’ expectations by 2.4%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ EBITDA estimates and a decent beat of analysts’ revenue estimates.

Snowflake scored the fastest revenue growth of the whole group. The company added 34 enterprise customers paying more than $1 million annually to reach a total of 688. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 15.9% since reporting and currently trades at $223.80.

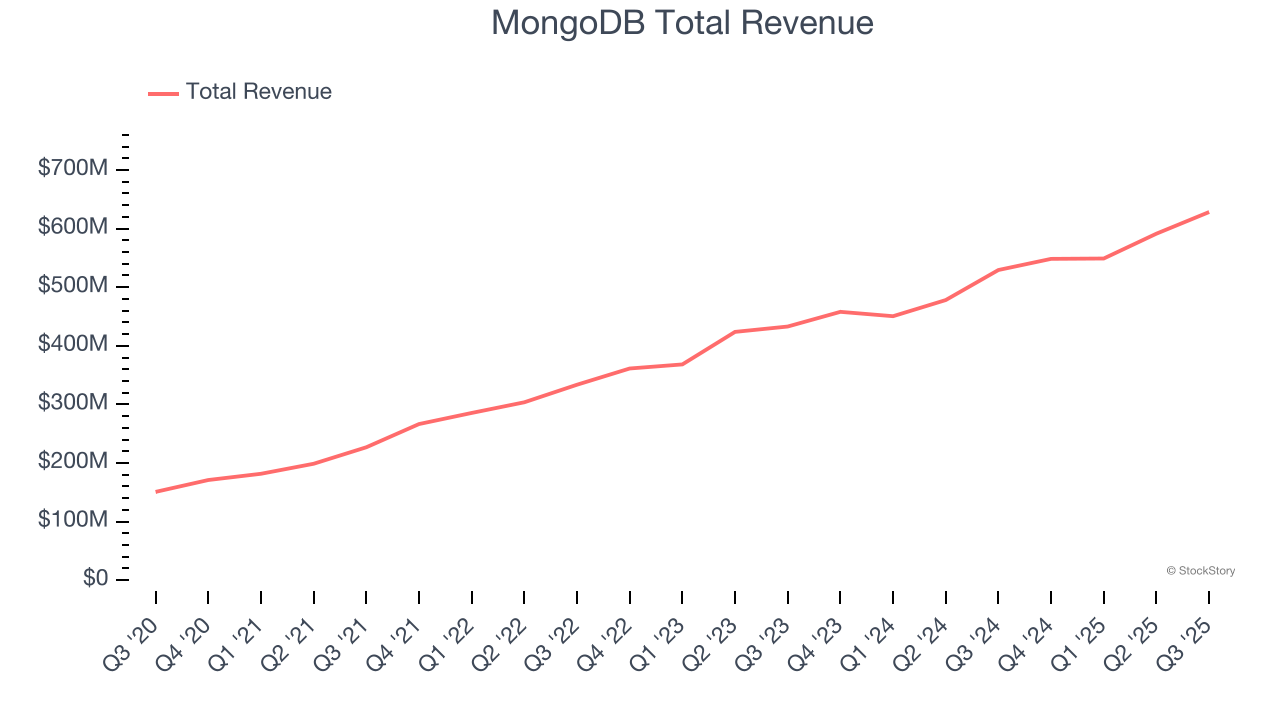

Named after "humongous database," reflecting its ability to handle massive data loads, MongoDB (NASDAQ:MDB) provides a flexible document-based database platform that helps developers build, deploy, and maintain modern applications more efficiently.

MongoDB reported revenues of $628.3 million, up 18.7% year on year, outperforming analysts’ expectations by 5.7%. The business had an exceptional quarter with a solid beat of analysts’ billings estimates and EPS guidance for next quarter exceeding analysts’ expectations.

MongoDB pulled off the biggest analyst estimates beat and highest full-year guidance raise among its peers. The company added 130 enterprise customers paying more than $100,000 annually to reach a total of 2,694. The market seems happy with the results as the stock is up 32.5% since reporting. It currently trades at $437.25.

Is now the time to buy MongoDB? Access our full analysis of the earnings results here, it’s free for active Edge members.

Born from the need to create ironclad protection in an increasingly dangerous digital world, Commvault (NASDAQ:CVLT) provides data protection and cyber resilience software that helps organizations secure, back up, and recover their data across on-premises, hybrid, and multi-cloud environments.

Commvault reported revenues of $276.2 million, up 18.4% year on year, exceeding analysts’ expectations by 1.1%. Still, it was a mixed quarter as it posted a miss of analysts’ EBITDA estimates.

Commvault delivered the weakest performance against analyst estimates and weakest full-year guidance update in the group. As expected, the stock is down 27.2% since the results and currently trades at $126.71.

Read our full analysis of Commvault’s results here.

Built for simplicity in a world of complex cloud solutions, DigitalOcean (NYSE:DOCN) provides a simplified cloud computing platform that enables developers and small businesses to quickly deploy and scale applications.

DigitalOcean reported revenues of $229.6 million, up 15.7% year on year. This print topped analysts’ expectations by 1.4%. Aside from that, it was a satisfactory quarter as it also recorded a solid beat of analysts’ EBITDA estimates but EPS guidance for next quarter missing analysts’ expectations significantly.

DigitalOcean had the slowest revenue growth among its peers. The stock is up 25.6% since reporting and currently trades at $48.75.

Read our full, actionable report on DigitalOcean here, it’s free for active Edge members.

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

| 1 hour | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-26 | |

| Mar-26 | |

| Mar-26 | |

| Mar-25 | |

| Mar-24 | |

| Mar-24 | |

| Mar-24 | |

| Mar-19 | |

| Mar-18 | |

| Mar-18 | |

| Mar-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite