|

|

|

|

|||||

|

|

|

Penumbra, Inc.’s PEN robust product portfolio expansion is poised to drive growth in the upcoming quarters. Additionally, the company’s global expansion efforts are thriving. Meanwhile, unfavorable foreign exchange and a dull macroeconomic scenario may pose operational risks for PEN.

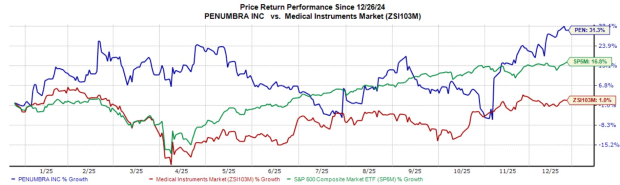

In the past year, shares of this Zacks Rank #3 (Buy) company have risen 31.3% compared with the industry’s 1% growth and the S&P 500 composite’s 16.8% increase.

The global healthcare provider company has a market capitalization of $12.37 billion. PEN beat on earnings in each of the trailing four quarters, the average surprise being 11.6%.

Strong Portfolio Expansion: Penumbra is advancing its proprietary thrombectomy technologies across the United States and internationally, with consistent revenue growth driven by strong adoption of its CAVT (computer assisted vacuum thrombectomy) portfolio. The company recorded its largest sequential increase so far in 2025 in the number of VTE (Pulmonary Embolism and Deep Vein Thrombosis) cases treated, indicating accelerating adoption during the third quarter. Meanwhile, Ruby XL began shipping at the end of second-quarter 2025, expanding Penumbra’s peripheral embolization portfolio to cover approximately 20% of the market previously untapped.

In stroke, RED 72 (SILVER LABEL) has seen strong physician uptake in its first full quarter on the market in Q2, while RED 43 continues to lead in distal occlusions.

Global Expansion Continues: Penumbra derives a meaningful portion of its revenues internationally (24.5% in 2024) and expects to materially expand both revenues and profitability across its international operations over the next several years. With China-related headwinds easing and double-digit growth from other international regions, the company’s international business has returned to growth, with sales increasing 6.6% in the third quarter.

Internationally, Penumbra is seeing early traction from the launch of its thrombectomy portfolio in Europe and plans to broaden access to its most advanced vascular technologies over time. More recently, the company expanded its CAVT footprint into Europe and additional non-U.S. markets, building on earlier European launches of the RED 72 SILVER LABEL catheter for stroke and its computer-orchestrated thrombectomy platforms, Lightning 12 and Lightning 7.

Macroeconomic Concerns: Outside the United States, Penumbra sells its products to healthcare providers through direct sales organizations and distributors in select international markets. The wide presence makes its operations vulnerable to macroeconomic risks, including disruptions to global trade resulting from changes in trade agreements or tariffs. While PEN has been able to offset much of the impact through favorable product mix and productivity improvements, selling, general and administrative (SG&A) expenses still rose 20.9% year over year in the third quarter of 2025, largely due to targeted hiring in the company’s commercial and market access teams.

Image Source: Zacks Investment Research

Foreign Exchange Impacts Sales: A significant portion of Penumbra’s sales and costs is exposed to changes in foreign exchange rates. In 2024, approximately 24% of the company's consolidated revenues came from the non-U.S. markets. PEN’s operations use multiple foreign currencies, including the euro and Japanese yen. Changes in those currencies relative to the U.S. dollar will impact its sales, cost of sales and expenses, and consequently, net income.

In the past 30 days, the Zacks Consensus Estimate for Penumbra’s 2025 earnings has moved north 1 cent to $3.78.

The Zacks Consensus Estimate for 2025 revenues is pegged at $1.38 billion, indicating a 15.7% rise from the year-ago reported number.

Some better-ranked stocks in the broader medical space are BrightSpring Health Services BTSG, lllumina ILMN and Insulet PODD.

BrightSpring Health Services has an estimated long-term earnings growth rate of 53.3% compared with the industry’s 15.5% growth. Its earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 45.1%. BTSG shares have surged 93.9% against the industry’s 0.1% decline over the past year.

BTSG sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Illumina, currently sporting a Zacks Rank #1, has an earnings yield of 3.7% compared to the industry’s -7.9% yield. Shares of the company have lost 10.8% over the past year against the industry’s 9.9% growth. ILMN’s earnings outpaced estimates in three of the trailing four quarters and missed on one occasion, the average surprise being 6.7%.

Insulet, currently carrying a Zacks Rank #2 (Buy), has an earnings yield of 3.9% against the industry’s -0.9% yield. Shares of the company have lost 7.8% compared with the industry’s 2.6% decline. PODD’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 17.8%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-22 | |

| Jul-20 | |

| Jul-20 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-10 | |

| Jul-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite