|

|

|

|

|||||

|

|

|

The U.S. housing industry is still under pressure as affordability remains a hurdle for potential buyers. Sterling Infrastructure, Inc. STRL is also facing the effect of this softer housing environment within its Building Solutions segment. In the third quarter of 2025, segment revenues declined 1% year over year, and legacy residential revenues fell 17% as the company noted that home demand remains weak because buyers continue to struggle with affordability challenges. The broader market received limited relief from policy support. On Dec. 10, 2025, the Federal Reserve cut interest rates by 0.25 percentage points, but higher mortgage costs, tight supply and price pressures still hold back demand, suggesting only gradual improvement heading into 2026.

Against this backdrop, the focus shifts to whether strength in E-Infrastructure can offset housing weakness in 2026. In the third quarter of 2025, the company underscored the growing importance of its E-Infrastructure Solutions segment, which serves data centers, manufacturing facilities and other mission-critical projects. Revenues from this segment (representing roughly 60% of total revenues) reached $417.1 million, reflecting approximately 58% growth from the year-ago period, highlighting strong demand and the increasing scale of customer investments. Data centers remain a key growth engine, while semiconductor and manufacturing megaprojects are expected to add meaningful opportunities in 2026 and 2027.

As of Sept. 30, 2025, the company reported a signed backlog of $2.6 billion, up 64% from the prior year, and total potential work above $4 billion when including awards and future phases, with E-Infrastructure representing most of this pipeline. Overall, continued housing softness remains a drag. However, the scale, margin profile and visibility of E-Infrastructure activity suggest that this strength can help balance housing pressure and support performance heading into 2026.

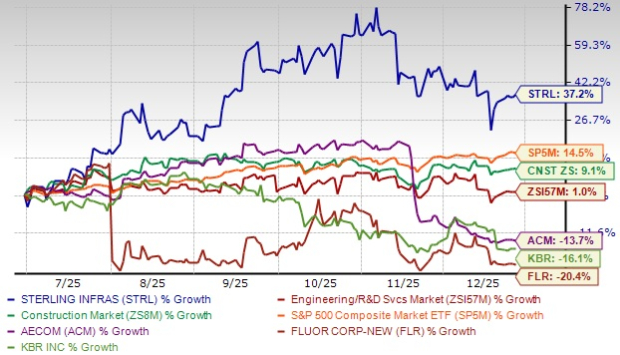

Shares of this Texas-based infrastructure services provider have surged 37.2% in the past six months, outperforming the Zacks Engineering - R and D Services industry’s 1% growth. The stock has further outperformed the broader Construction sector and the S&P 500, which have advanced 9.1% and 14.5%, respectively in the same period.

In the same time frame, other industry players like AECOM ACM, Fluor Corporation FLR and KBR, Inc. KBR have declined 13.7%, 20.4% and 16.1%, respectively.

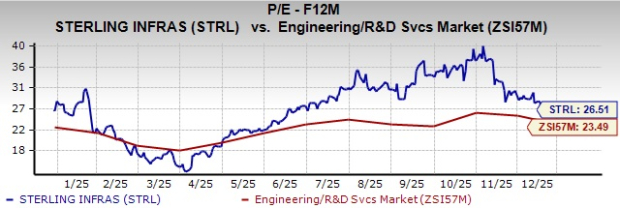

STRL stock is currently trading at a premium compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 26.51, as shown in the chart below.

Meanwhile, industry players, such as AECOM, Fluor and KBR, have P/E multiples of 16.92, 18.18 and 9.65, respectively.

For 2026, estimates for STRL’s earnings have increased in the past 60 days to $11.95 from $10.98 per share. The revised estimated figures indicate 14.6% year-over-year growth.

The company currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| 4 hours | |

| 4 hours | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite