|

|

|

|

|||||

|

|

|

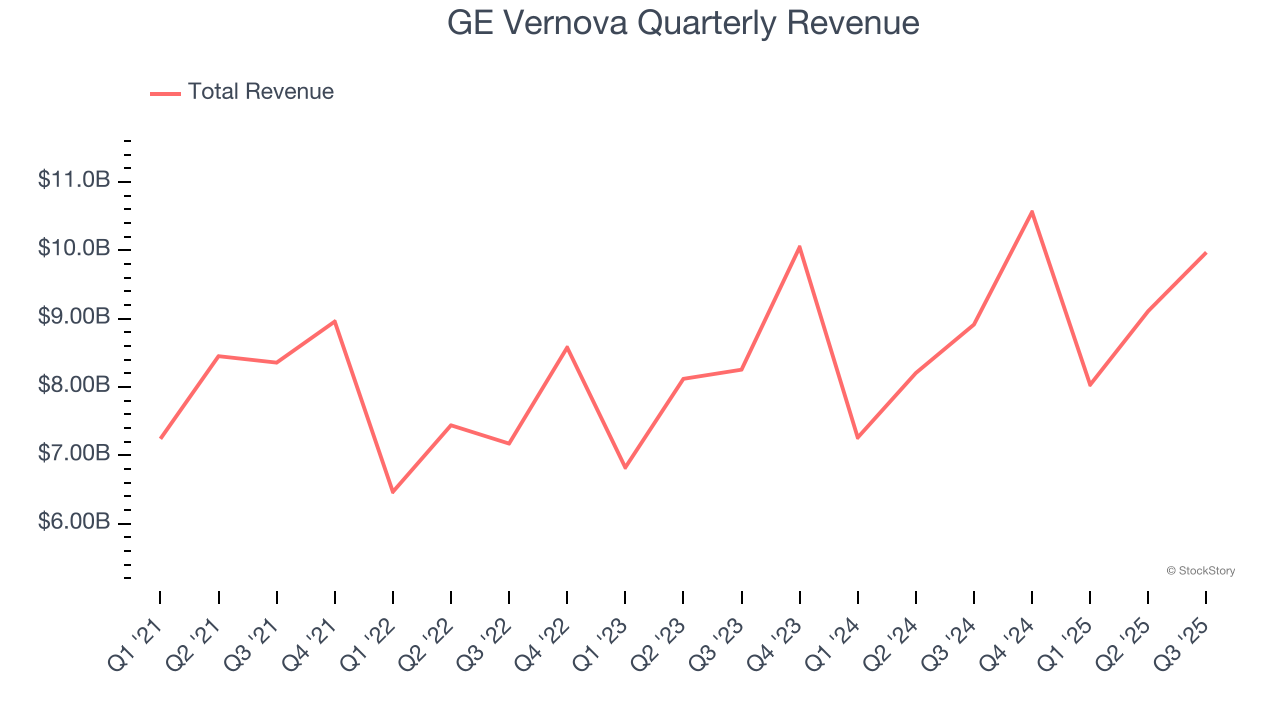

Energy transition company GE Vernova (NYSE:GEV) reported Q3 CY2025 results exceeding the market’s revenue expectations, with sales up 11.8% year on year to $9.97 billion. On the other hand, the company’s full-year revenue guidance of $36.5 billion at the midpoint came in 1.8% below analysts’ estimates. Its GAAP profit of $1.64 per share was 11.5% below analysts’ consensus estimates.

Is now the time to buy GE Vernova? Find out by accessing our full research report, it’s free for active Edge members.

Born from the energy business of industrial giant General Electric in a 2023 spin-off, GE Vernova (NYSE:GEV) designs, manufactures, and services power generation equipment and grid technologies to help customers build more reliable and sustainable electric systems.

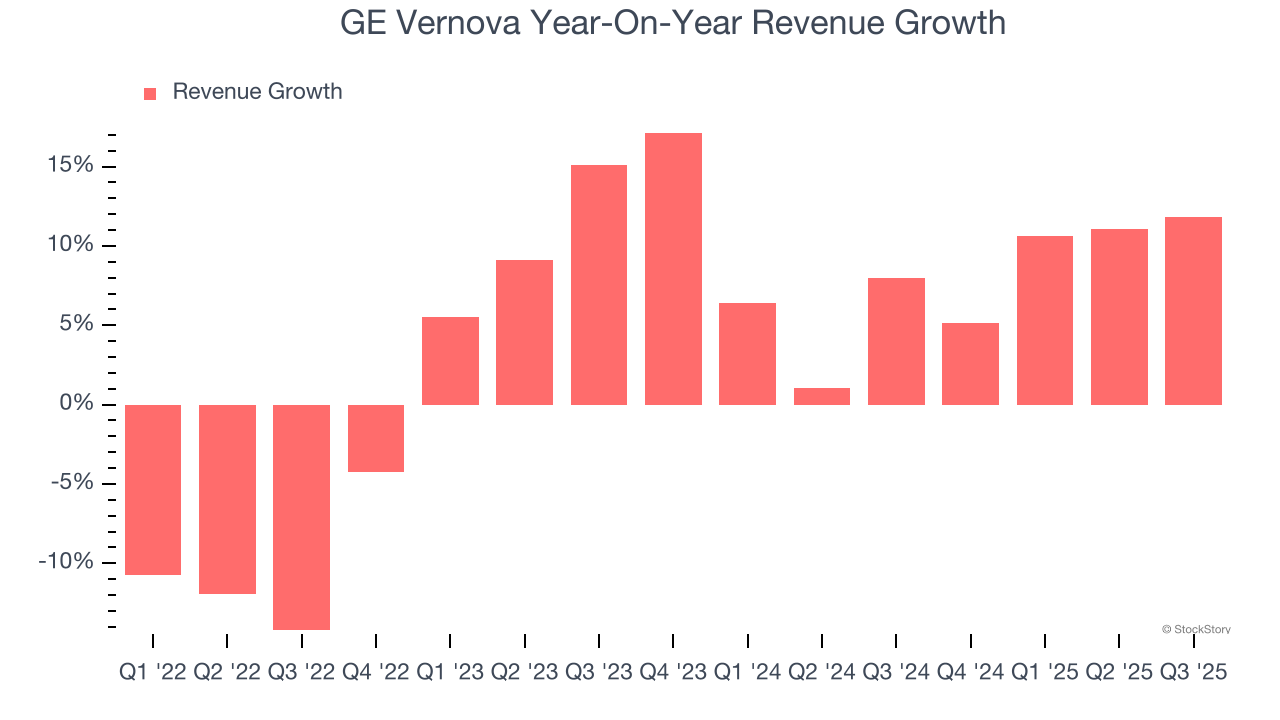

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last four years, GE Vernova grew its sales at a sluggish 3% compounded annual growth rate. This wasn’t a great result compared to the rest of the industrials sector, but there are still things to like about GE Vernova.

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. GE Vernova’s annualized revenue growth of 8.9% over the last two years is above its four-year trend, suggesting some bright spots.

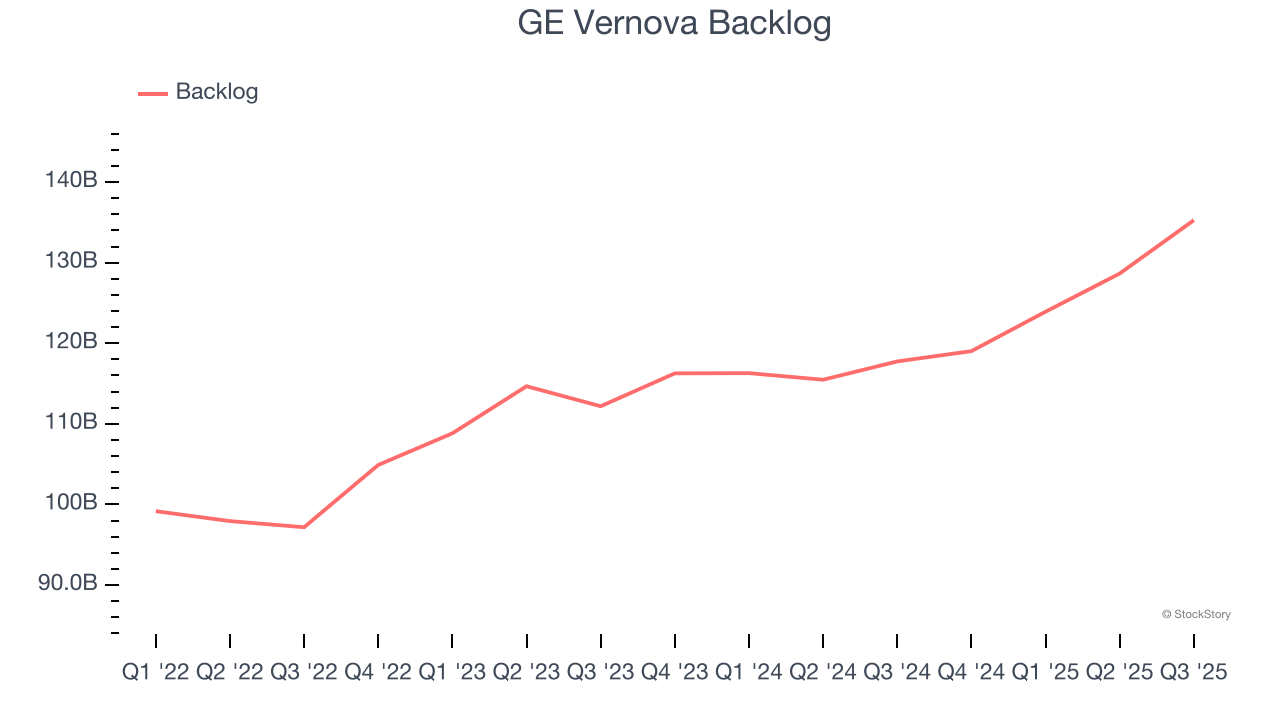

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. GE Vernova’s backlog reached $135.3 billion in the latest quarter and averaged 7.3% year-on-year growth over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies GE Vernova was operating efficiently but raises questions about the health of its sales pipeline.

This quarter, GE Vernova reported year-on-year revenue growth of 11.8%, and its $9.97 billion of revenue exceeded Wall Street’s estimates by 8.9%.

Looking ahead, sell-side analysts expect revenue to grow 6.4% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

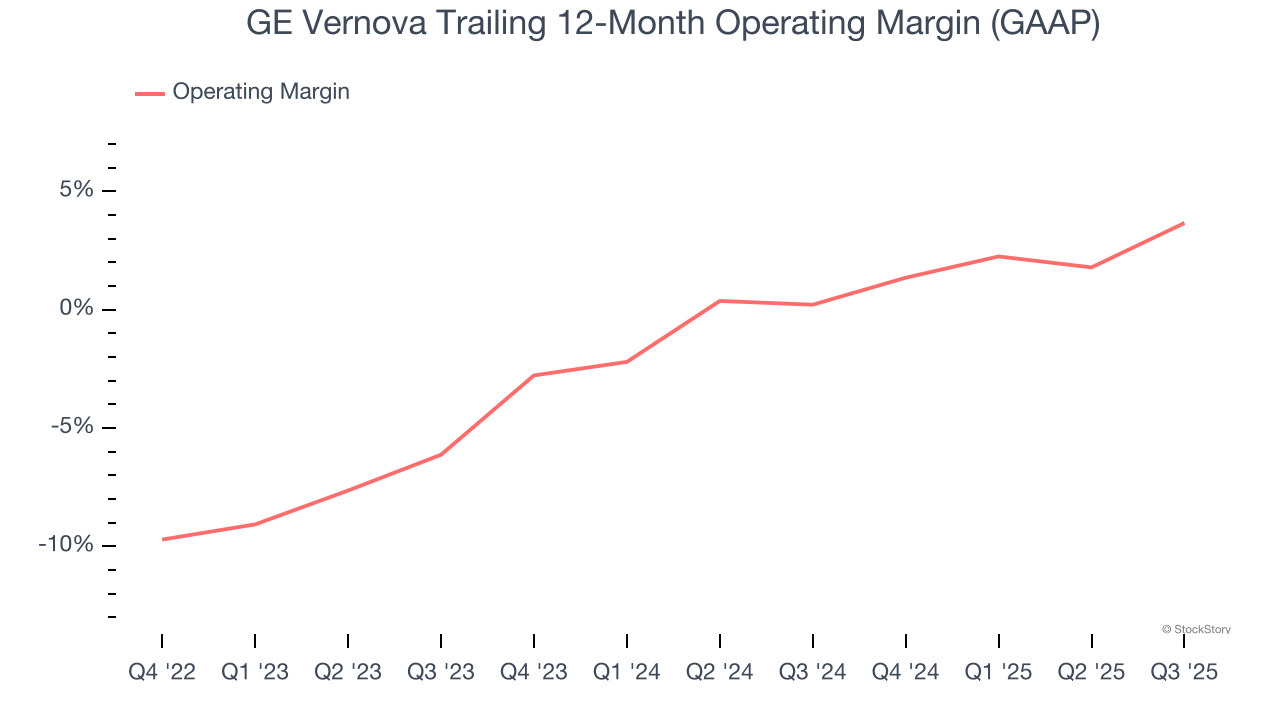

Although GE Vernova was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 2% over the last four years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, GE Vernova’s operating margin rose by 12.6 percentage points over the last four years, as its sales growth gave it operating leverage. Still, it will take much more for the company to show consistent profitability.

This quarter, GE Vernova generated an operating margin profit margin of 3.7%, up 7.7 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

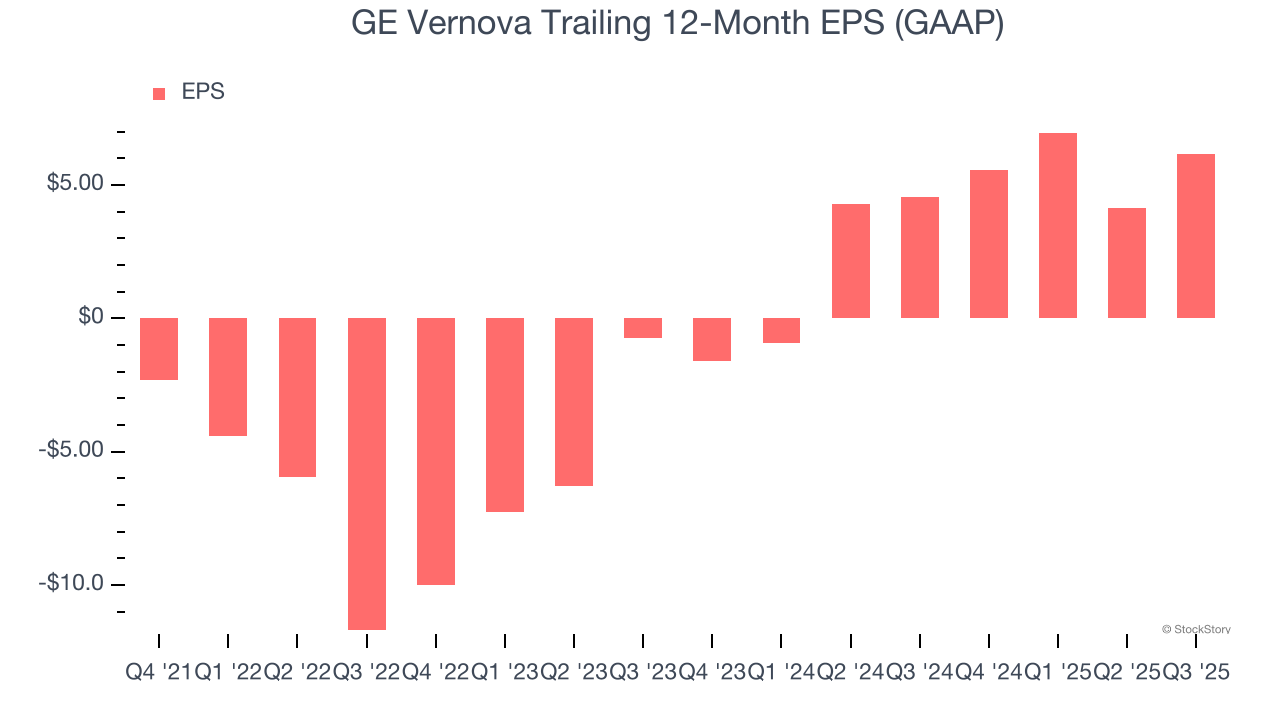

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

GE Vernova’s full-year EPS flipped from negative to positive over the last four years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For GE Vernova, its two-year annual EPS growth of 220% was higher than its four-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q3, GE Vernova reported EPS of $1.64, up from negative $0.35 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects GE Vernova’s full-year EPS of $6.14 to grow 89.5%.

We were impressed by how significantly GE Vernova blew past analysts’ adjusted operating income expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its EPS missed and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock remained flat at $663.58 immediately following the results.

Sure, GE Vernova had a solid quarter, but if we look at the bigger picture, is this stock a buy? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 | |

| Mar-24 | |

| Mar-23 | |

| Mar-23 | |

| Mar-23 | |

| Mar-20 | |

| Mar-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite