|

|

|

|

|||||

|

|

|

ScanSource currently trades at $39.84 per share and has shown little upside over the past six months, posting a small loss of 4.7%. The stock also fell short of the S&P 500’s 11.7% gain during that period.

Is there a buying opportunity in ScanSource, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

We don't have much confidence in ScanSource. Here are three reasons why SCSC doesn't excite us and a stock we'd rather own.

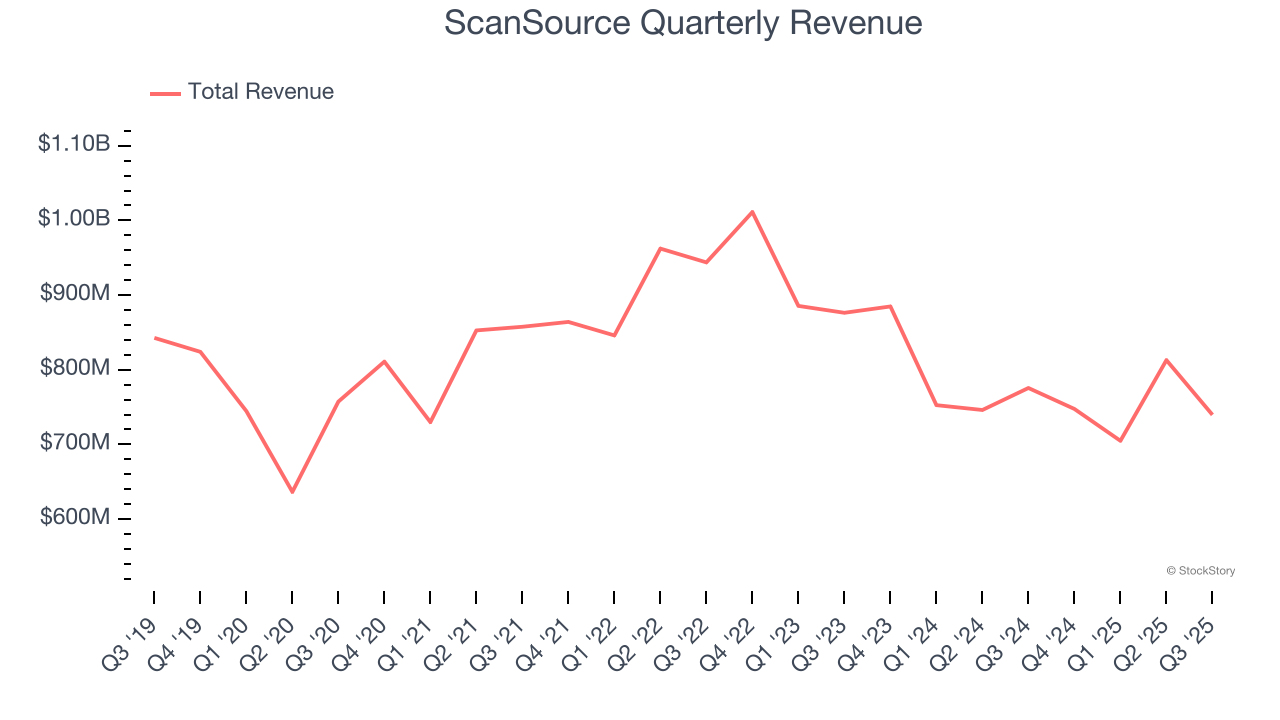

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, ScanSource struggled to consistently increase demand as its $3.00 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of poor business quality.

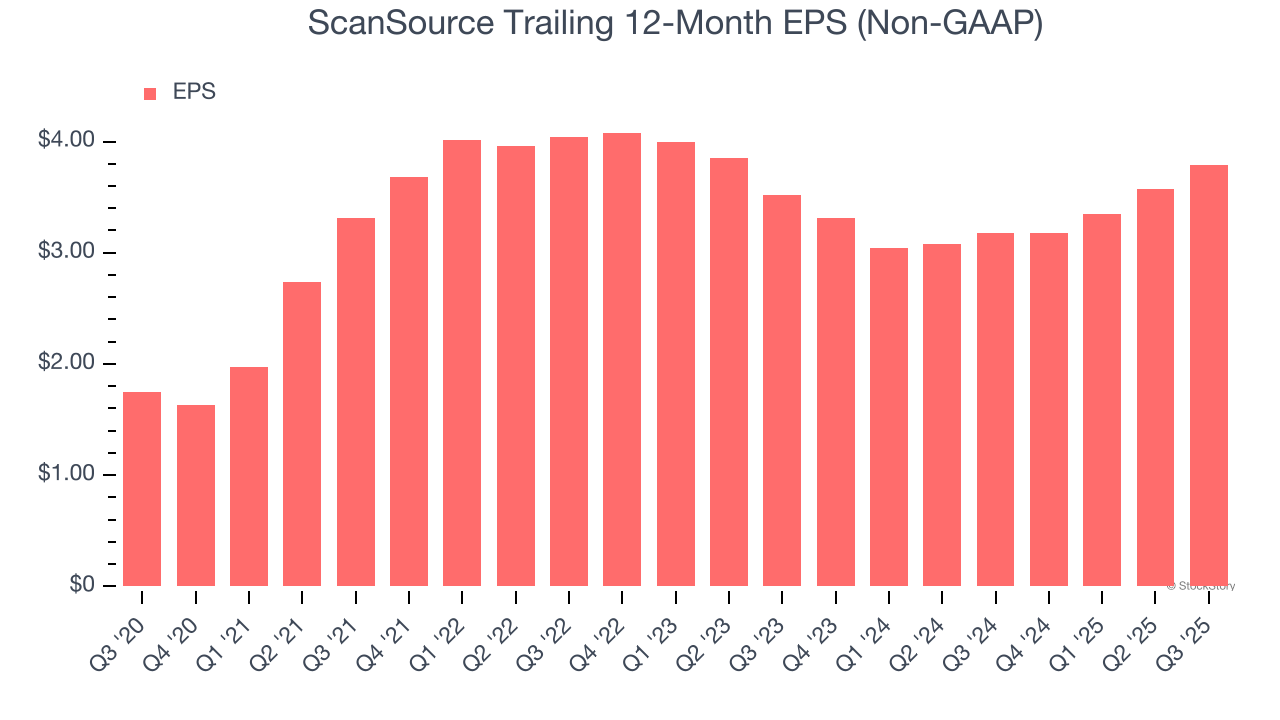

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

ScanSource’s EPS grew at a weak 3.8% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its 11.1% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

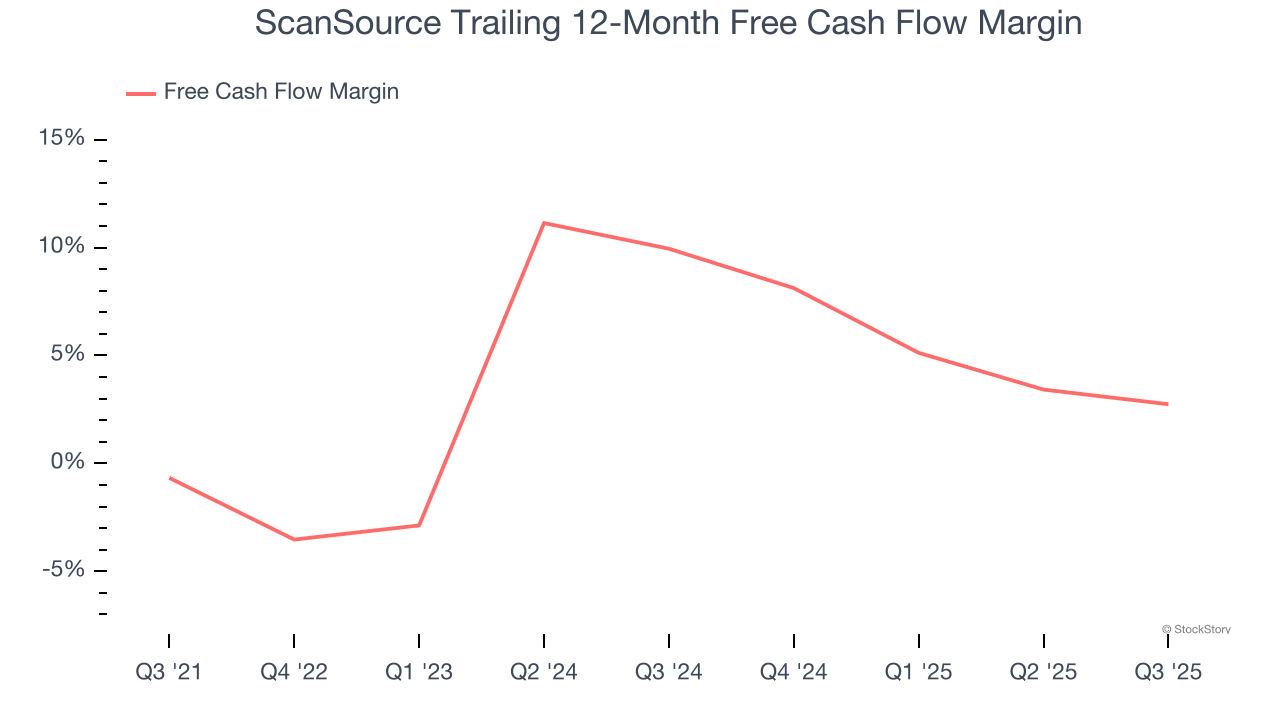

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

ScanSource has shown weak cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.6%, subpar for a business services business.

ScanSource falls short of our quality standards. With its shares trailing the market in recent months, the stock trades at 9.3× forward P/E (or $39.84 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment. We’d suggest looking at the most dominant software business in the world.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jun-30 | |

| May-07 | |

| May-07 | |

| May-07 | |

| May-07 | |

| Apr-21 | |

| Apr-16 | |

| Mar-16 | |

| Mar-06 | |

| Mar-05 | |

| Mar-04 | |

| Feb-25 | |

| Feb-06 | |

| Feb-05 | |

| Feb-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite