|

|

|

|

|||||

|

|

|

Over the past six months, Texas Capital Bank has been a great trade, beating the S&P 500 by 5.4%. Its stock price has climbed to $93.01, representing a healthy 17.1% increase. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Texas Capital Bank, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

We’re happy investors have made money, but we don't have much confidence in Texas Capital Bank. Here are three reasons why TCBI doesn't excite us and a stock we'd rather own.

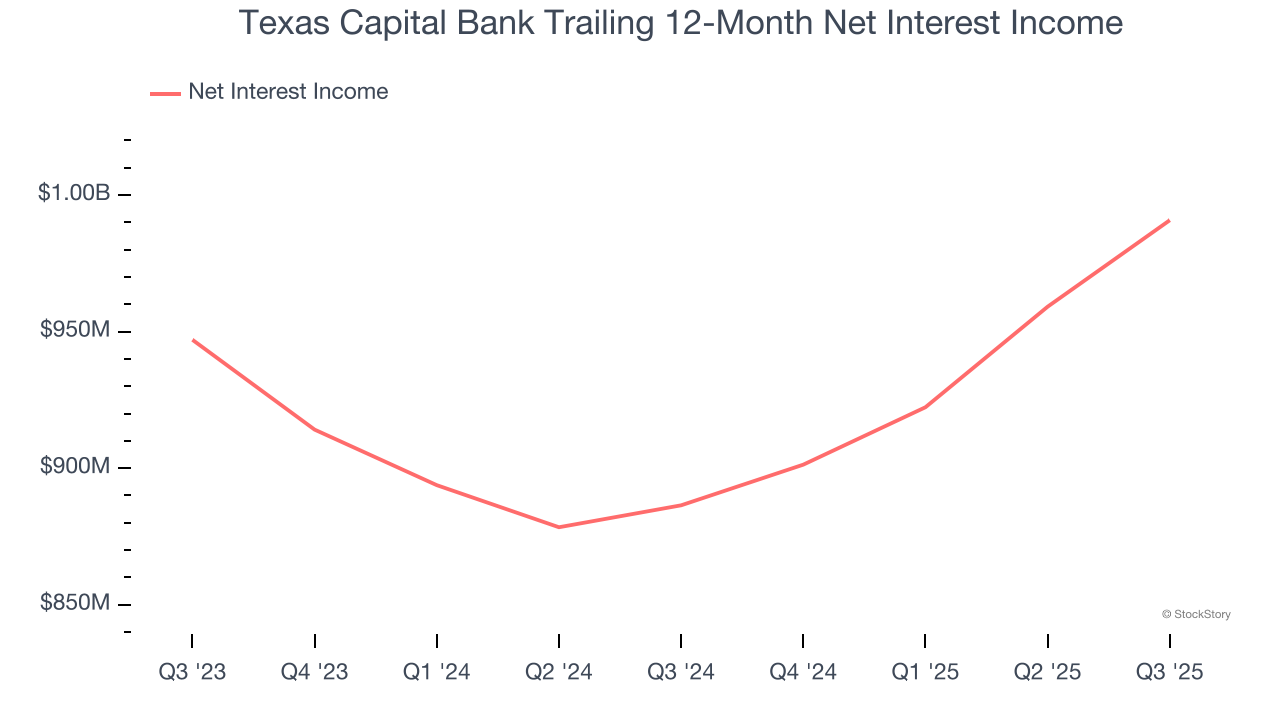

Our experience and research show the market cares primarily about a bank’s net interest income growth as one-time fees are considered a lower-quality and non-recurring revenue source.

Texas Capital Bank’s net interest income has grown at a 2.1% annualized rate over the last five years, much worse than the broader banking industry and in line with its total revenue. Its growth was driven by an increase in its net interest margin, which represents how much a bank earns in relation to its outstanding loans, as its loan book shrank throughout that period.

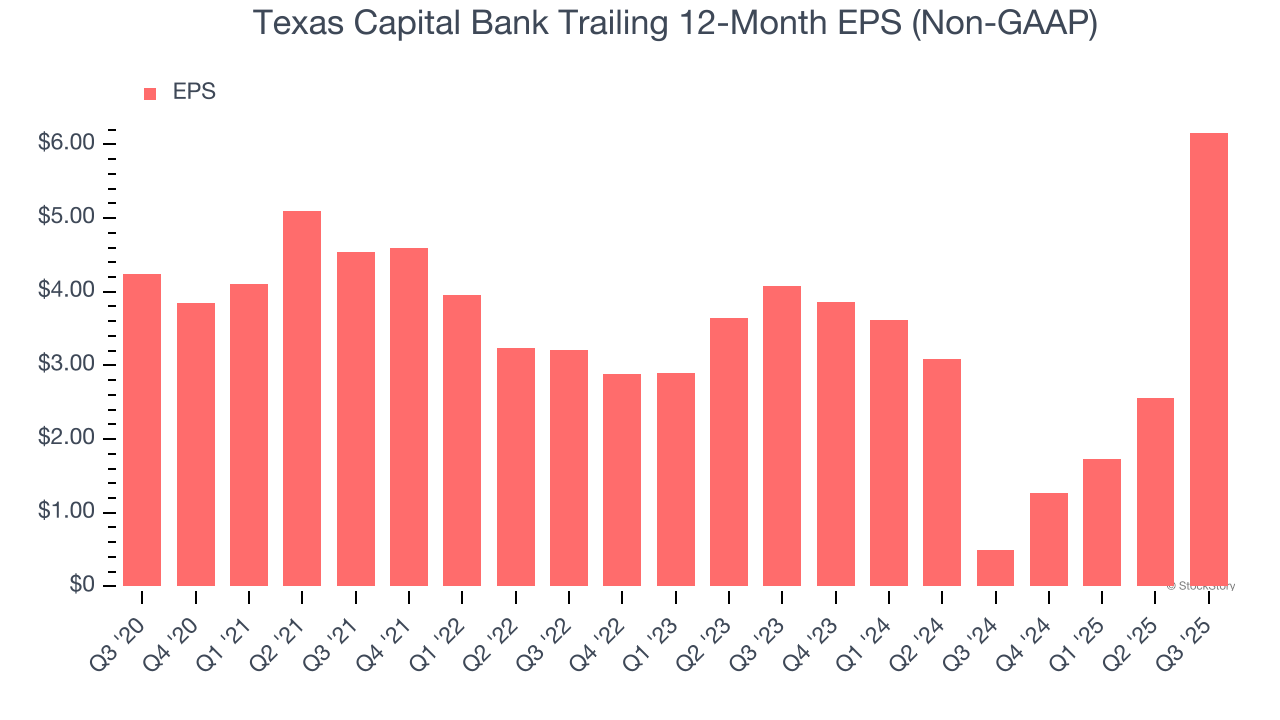

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Texas Capital Bank’s EPS grew at an unimpressive 7.8% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 2.8% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

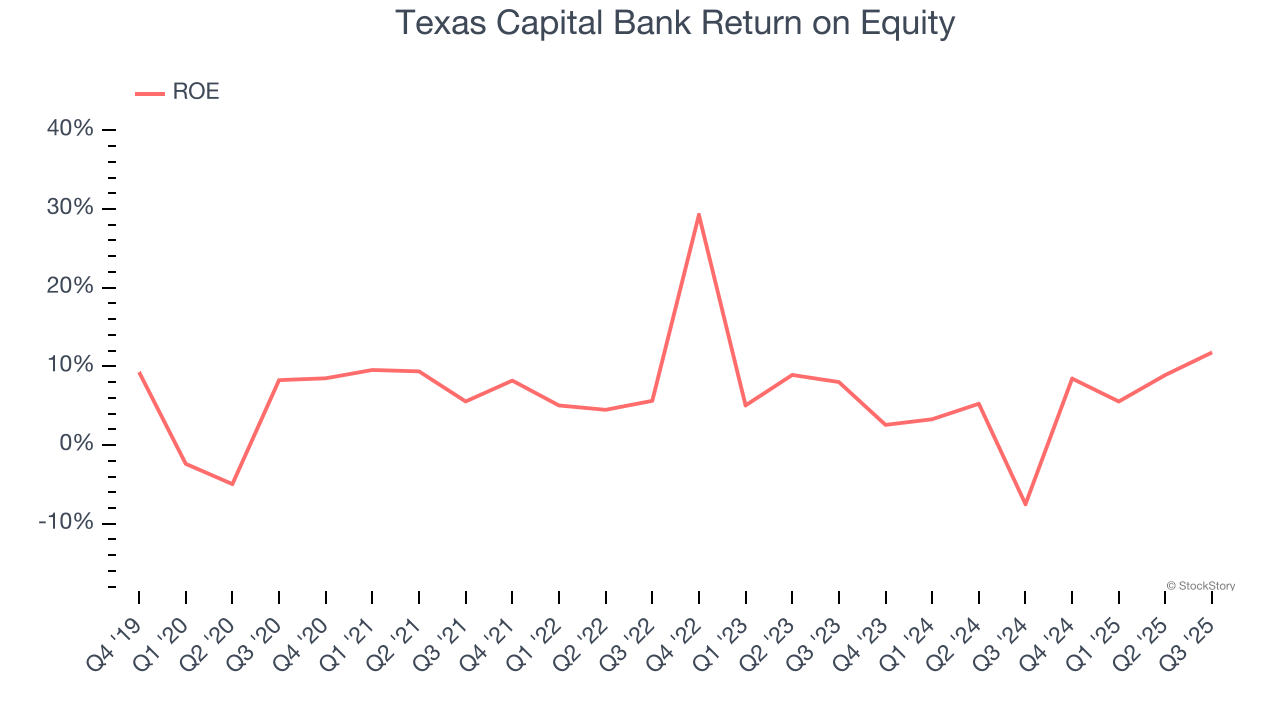

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, Texas Capital Bank has averaged an ROE of 7.3%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

Texas Capital Bank’s business quality ultimately falls short of our standards. With its shares outperforming the market lately, the stock trades at 1.2× forward P/B (or $93.01 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-13 | |

| Jul-13 | |

| Jul-08 | |

| Jun-30 | |

| May-05 | |

| Apr-24 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite