|

|

|

|

|||||

|

|

|

Bristol Myers Squibb BMY and Amgen AMGN are among the largest global biotechnology companies with broad and diverse portfolios.

Bristol Myers Squibb is focused on discovering, developing and delivering transformational therapies across oncology, hematology, immunology, cardiovascular, neuroscience and other serious diseases.

Meanwhile, Amgen boasts one of the largest portfolios in the biotech industry, with a strong presence in oncology, cardiovascular disease, inflammation, bone health and rare diseases.

Both biotech giants have built strong footholds in their respective target markets and have consistently delivered value to shareholders. Against this backdrop, selecting one stock over the other is no easy task. A closer examination of their fundamentals, growth prospects, key challenges and valuation metrics can help investors make a more informed decision.

BMY’s Growth Portfolio comprises drugs like Opdivo, Opdivo Qvantig, Orencia, Yervoy, Reblozyl, Camzyos, Breyanzi, Opdualag, Zeposia, Abecma, Sotyku, Krazati and Cobenfy.

The recent performance of this portfolio has been strong, maintaining top-line growth for BMY.

Opdivo sales in the United States are being driven by a strong launch in MSI-high colorectal cancer and continued growth in first-line non-small cell lung cancer, while international sales are supported by label expansion of the drug across multiple markets.

The approval of Opdivo Qvantig (nivolumab and hyaluronidase-nvhy) injection for subcutaneous use has boosted BMY’s immuno-oncology portfolio. The initial uptake has been strong and the launch is going well in the United States across all indicated tumor types.

Bristol Myers now expects global Opdivo sales, together with Qvantig, to increase in the high single-digit to low double-digit range in 2025 (previous guidance: mid to high single-digit range in 2025), driven by strong performance year to date.

The stellar performance of the thalassemia drug Reblozyl, for which BMY has a collaboration agreement with Merck MRK, has significantly boosted BMY’s top line. BMY is now annualizing over $2 billion in Reblozyl sales. Revenue growth continues to be strong, primarily due to demand in first-line RS-positive and RS-negative settings as well as improved duration of therapy.

Breyanzi sales are now annualizing over $1 billion, reflecting strong growth in large B-cell lymphoma and expansion in new indications approved last year.

Cardiovascular drug Camzyos sales continue to increase on robust demand.

The FDA approval for xanomeline and trospium chloride (formerly KarXT), an oral medication for the treatment of schizophrenia, in adults (under the brand name Cobenfy), is a significant boost for the company.

The initial uptake is encouraging, with sales of $105 million year to date. Cobenfy is expected to contribute meaningfully to BMY’s top line in the coming years as the company looks to expand the drug’s label into other indications.

However, while BMY is progressing with its growth portfolio, its legacy portfolio is being adversely impacted due to continued generic impact on Revlimid, Pomalyst, Sprycel and Abraxane.

The decline in sales of legacy drugs has adversely impacted the top line. BMY continues to expect the legacy portfolio to decline approximately 15-17% in 2025.

The legacy portfolio also comprises blood thinner medicine Eliquis, for which BMY has a worldwide co-development and co-commercialization agreement with pharma giant Pfizer PFE. Eliquis is the biggest contributor to the top line.

With a vast global footprint, Amgen’s diverse portfolio has positioned it well in the evolving biotech industry with a strong presence in the oncology, cardiovascular disease, inflammation, bone health and rare diseases markets.

Growth products like Evenity, Vectibix, Nplate and Kyprolis and Blincyto have performed well on consistent label expansions. Robust growth from these products has stabilized the company’s revenue base in the face of declining sales from legacy drugs.

However, increasingly competitive pressure is negatively impacting the sales of many products. In the coming quarters, Prolia and Xgeva sales are anticipated to decrease due to the impact of biosimilars entering the market.

Nonetheless, Repatha, a key drug in Amgen’s arsenal, is driving the growth trajectory. The approval of Tezspire/tezepelumab to treat severe asthma has also strengthened the company’s portfolio.

Amgen is evaluating Repatha, Uplizna, Tepezza and Tavneos for additional indications. Amgen also has promising candidates in its pipeline, which represent significant commercial potential. Amgen is conducting a broad phase III program on MariTide across obesity, obesity-related conditions and type-II diabetes.

Amgen also boasts a strong biosimilars portfolio. Approvals of Wezlana and Pavblu have strengthened this portfolio.

With a robust cash balance, Amgen is continually seeking strategic deals to expand its business. The acquisition of Horizon Therapeutics has significantly expanded Amgen's rare disease business by adding several rare disease drugs, including Tepezza, Krystexxa and Uplizna, to its portfolio.

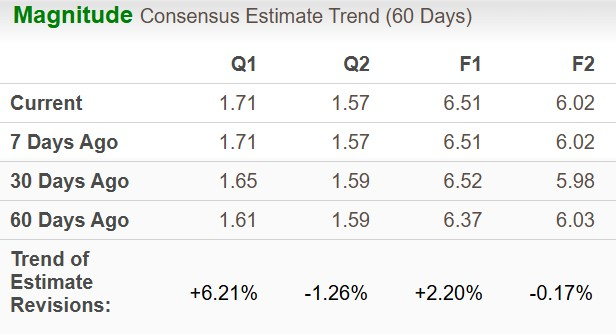

The Zacks Consensus Estimate for BMY’s 2025 sales implies a year-over-year decrease of 0.8%, while that for earnings per share (EPS) suggests a year-over-year increase of 466.09%. EPS estimates for 2025 have moved north in the past 60 days, but the same for 2026 has moved south during the said time frame.

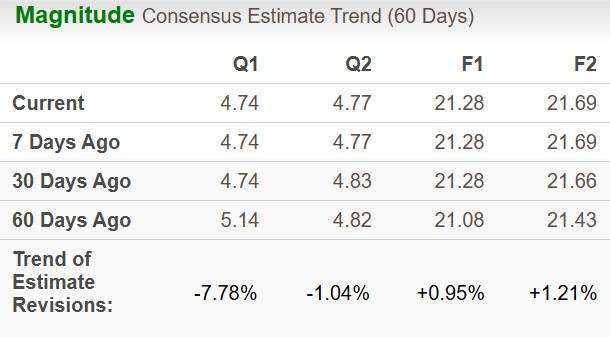

The Zacks Consensus Estimate for AMGN’s 2025 sales implies a year-over-year increase of 8.78%, and that for EPS suggests a year-over-year improvement of 7.26%. EPS estimates for 2025 and 2026 have moved north in the past 60 days.

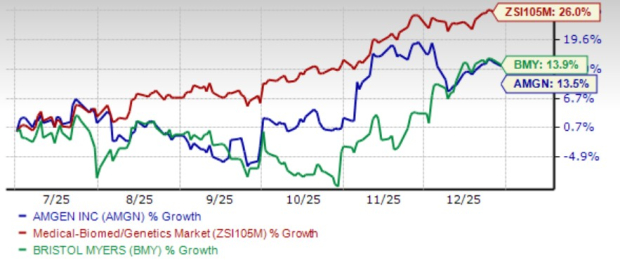

From a price-performance perspective, BMY has fetched slightly better returns than AMGN in the past six months. Shares of AMGN have gained 13.5%, while those of BMY have gained 13.9%. The industry has surged 26% in the said period.

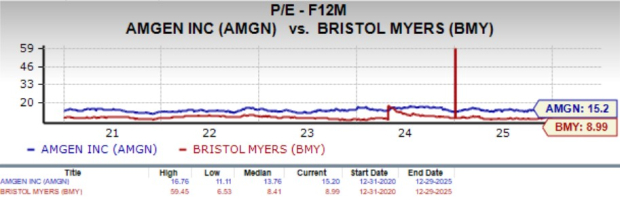

From a valuation standpoint, as the biotech industry has very few players with approved drugs, we use the P/E ratio of the large-cap pharma industry to compare these companies. Going by the same, AMGN is more expensive than BMY. AMGN’s shares currently trade at 15.2X forward earnings, higher than 8.99X for BMY but lower than 17.58X for the industry.

AMGN and BMY’s attractive dividend yield is a strong positive for investors. However, BMY’s dividend yield of 4.54% is higher than AMGN’s 2.86%.

Large biotech companies are generally considered safe havens for investors interested in this sector.

However, with both AMGN and BMY currently carrying a Zacks Rank #3 (Hold), choosing one stock over the other is a complex task. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

AMGN’s strong and diverse portfolio should enable it to maintain growth. Key drugs like Evenity and Repatha, as well as newer drugs like Tavneos and Tezspire, continue to drive growth and offset the revenue decline from oncology biosimilars and legacy drugs like Enbrel.

BMY’s efforts to revive the top line in the face of generic challenges for key drugs are commendable. The company has rebounded quite well in the second half of 2025 and newer drugs are now driving revenue growth.

However, AMGN is a better pick at present (despite its pricey valuation) as we believe there is room for growth buoyed by solid fundamentals and recent positive estimate revisions.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 5 hours |

Bristol Myers, NVIDIA join forces to build life sciences most powerful AI factory

BMY

Pharmaceutical Technology

|

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite