|

|

|

|

|||||

|

|

|

Molson Coors Beverage Company’s TAP outlook is mainly shaped by one central issue: declining volumes. While pricing actions, mix improvement and cost discipline continue to provide some cushion, the company is operating in a beer industry that remains structurally soft, particularly in the United States. In the third quarter of 2025, consolidated net sales declined 3.3% year over year, reflecting the difficulty of offsetting lower shipment volumes despite modest pricing gains. Management has reiterated that the industry slowdown is cyclical, but the persistence of volume pressure raises questions about how durable earnings recovery can be if demand remains weak into 2026.

The numbers underline why volume is the key risk. In third-quarter 2025, Molson Coors’ brand volumes fell roughly 4%-5%, while the U.S. beer industry itself declined by about 4.7%. Earlier in the year, the pressure was even more pronounced, with first-half volumes down at a high-single-digit pace, exacerbated by weaker distributor shipments and reduced contract brewing.

Although net price realization improved by around 1%-2%, it was not enough to fully offset volume declines, leading management to guide 2025 net sales to a 3%-4% decline and underlying pretax income to fall 12%-15%. These dynamics highlight the limits of pricing in a contracting category.

Molson Coors’ volume challenges are not purely company-specific but reflect broader industry and macro trends. Beer consumption in the United States continues to face pressure from shifting consumer preferences, higher living costs and softer demand among lower-income consumers, while European markets remain sluggish.

Against this backdrop, Molson Coors is leaning on restructuring, portfolio prioritization and investment behind core and premium brands to stabilize performance. Still, unless industry volumes show meaningful improvement, volume decline is likely to remain the biggest drag on the company’s 2025 outlook, overshadowing otherwise solid execution on pricing, cost control and balance-sheet strength.

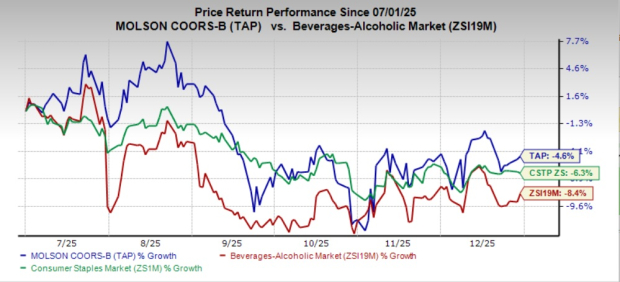

Shares of this Zacks Rank #3 (Hold) company have lost 4.6% in the past six months compared with the Zacks Beverages - Soft Drinks industry’s decline of 8.4% and the broader Consumer Staples sector’s fall of 6.3%.

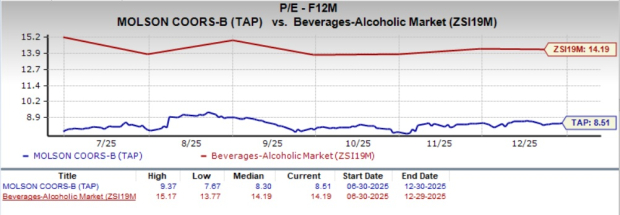

Molson Coors shares are currently trading at a forward 12-month price-to-earnings (P/E) multiple of 8.51X, at a discount compared with the industry’s average of 14.19X. The stock is undervalued compared with its industry peers, offering compelling value to investors looking for exposure to the beverage segment.

The Vita Coco Company, Inc. COCO develops, markets and distributes coconut water products under the Vita Coco brand name in the United States, Canada, Europe, the Middle East, Africa and the Asia Pacific. COCO currently flaunts a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Vita Coco's current fiscal-year sales and earnings implies growth of 18% and 15%, respectively, from the year-ago reported figures. Vita Coco delivered a trailing four-quarter earnings surprise of 30.4%, on average.

Monster Beverage Corporation MNST engages in the development, marketing, sale and distribution of energy drink beverages and concentrates in the United States and internationally. MNST currently sports a Zacks Rank #1.

The Zacks Consensus Estimate for Monster Beverage's current fiscal-year sales and earnings implies growth of 9.7% and 22.8%, respectively, from the year-ago actuals. MNST delivered a trailing four-quarter earnings surprise of 5.5%, on average.

United Natural Foods, Inc. UNFI distributes natural, organic, specialty, produce and conventional grocery and non-food products in the United States and Canada. At present, United Natural flaunts a Zacks Rank of 1.

The Zacks Consensus Estimate for United Natural’s current fiscal-year sales and earnings implies growth of 9.7% and 22.8%, respectively, from the year-ago reported figures. UNFI delivered a trailing four-quarter earnings surprise of 5.5%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-03 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-27 | |

| Jul-25 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite