|

|

|

|

|||||

|

|

|

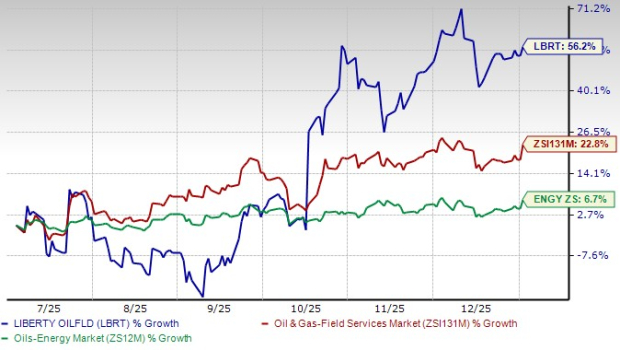

Over the past six months, Liberty Energy Inc. LBRT has significantly outperformed both the Field Services Oil and Gas sub-industry and the broader oil and energy sector. LBRT’s shares have surged 56.2%, far surpassing the Oil & Gas-Field Services Market (ZS131M), which saw growth of 22.8%. Meanwhile, the broader Oil-Energy Market showed a modest growth of only 6.7%. This impressive growth for LBRT highlights its strong performance in a competitive market.

With operations in major basins across North America, such as the Permian, Eagle Ford and Marcellus Shales, LBRT is vital to the growth of the U.S. energy sector. Headquartered in Denver, the company has a strategic edge, especially with the involvement in sand mining for proppant used in hydraulic fracturing, giving it better control over the supply chain.

Additionally, LBRT's focus on cutting-edge technologies and data analytics allows it to enhance the efficiency and safety of the hydraulic fracturing process, offering clients valuable insights. Recently, the company expanded its portfolio with the acquisition of IMG Energy Solutions, a developer of distributed power systems.

Given its industry position and scale, LBRT garners significant attention from investors. While the company has many strengths, there are also risks to consider before making investment decisions. Let’s dive into the factors that influence LBRT stock's performance and the potential challenges it faces moving forward.

Strong Technological Edge in Core Business: LBRT demonstrates industry-leading operational technology through its digiPrime fleets and StimCommander software. The Innovative energy firm reports record-breaking efficiency metrics in the third quarter, including a 30% reduction in maintenance costs for its proprietary pumps and a 65% improvement in fluid injection rate delivery through automation. This technological superiority translates directly into lower costs and higher reliability for customers, creating a sustainable competitive advantage that should support market share retention and premium service pricing through industry cycles.

Strategic Expansion Into High-Demand Power Market: LBRT is successfully executing a strategic pivot to capitalize on structural power demand, particularly from data centers and industrial reshoring. LBRT has more than doubled its sales pipeline in 90 days and is securing equipment to deliver more than 1 gigawatt of capacity by 2027. This positions the company to benefit from the urgent need for reliable, on-site power generation driven by AI computational loads and grid reliability challenges, establishing a substantial new long-term growth driver alongside its traditional business.

Robust Pipeline of Long-Term Contract Opportunities: Management expressed high confidence in converting its multi-gigawatt sales pipeline into firm contracts, with negotiations focused on partnerships lasting 15 years or more. The company has already issued letters of intent and term sheets for several gigawatts of capacity needs. This visibility into potential long-duration, take-or-pay energy service agreements provides a foundation for predictable future revenue streams and attractive returns on invested capital in the power segment.

Operational Resilience During Market Downturns: Despite industry-wide activity declines and pricing pressure, LBRT maintained full fleet utilization and achieved the highest combined average daily pumping efficiency in its history during the third quarter. This outperformance relative to the market demonstrates the company's ability to navigate cyclical downturns through superior service quality and customer relationships, positioning it for a stronger recovery when market conditions improve.

Favorable Exposure to Growing Natural Gas Demand: While near-term oil completions have softened, LBRT highlighted encouraging long-term fundamentals for natural gas, supported by LNG export capacity expansion and rising power consumption. The company's positioning in gas-prone basins and its efficient fleet technology align well with this structural demand trend, providing a natural hedge and growth runway beyond the current oil market cycle.

Aggressive Capital Spending Amid Cash Flow Decline: The company reported $113 million in net capital expenditures for the third quarter and guides to $525-$550 million for full-year 2025. This substantial investment rate coincides with declining operating cash flows, contributing to a $99 million increase in net debt during the quarter. The high capex burden could strain the balance sheet if the market downturn persists longer than anticipated or the power project returns take longer to materialize.

Deteriorating Balance Sheet and Liquidity Metrics: LBRT ended the third quarter with a cash balance of only $13 million and net debt of $240 million, representing a significant quarter-over-quarter increase. Total liquidity stood at $146 million. This weakening financial position, combined with substantial ongoing capital commitments, raises concerns about financial flexibility, especially if the completions market recovery is delayed or power project deployments encounter unexpected costs.

Rising Project Costs and Supply-Chain Inflation: Management indicated that estimated capital costs for installed power generation have increased to $1.5-$1.6 million per megawatt, attributing this to both pricing pressures from high global demand and project scope variability. Ongoing supply-chain constraints for long-lead equipment present additional risks to project timelines and economics, potentially eroding the attractive returns management has projected for the power business.

Customer Concentration Risk in Power Segment: The power business' success depends heavily on securing contracts with a concentrated group of large hyperscale data center operators. The chief financial officer noted that approximately 70% of the data center market is controlled by just 6-7 large clients. This high customer concentration creates counterparty risk, where the loss of a single major customer or shift in their strategic direction could significantly impact the growth trajectory and utilization of LBRT's substantial power capacity investments.

Macroeconomic and Commodity Price Vulnerability: LBRT's forecast for a complete activity recovery in late 2026 is explicitly contingent on supportive commodity futures prices. A prolonged period of low oil and gas prices, potentially caused by weaker global demand or sustained OPEC+ production, would delay the anticipated cyclical rebound, maintaining pressure on pricing, profitability and cash flow in the company's still-dominant core business segment.

LBRT has a strong technological edge in core business, demonstrated by its industry-leading fleets and software, which improve efficiency and reliability while reducing costs. The company is also strategically expanding into the high-demand power market, positioning itself to benefit from growth in data centers and industrial reshoring. Additionally, LBRT has a robust long-term contract pipeline, providing visibility into future revenue streams.

However, aggressive capital spending amid declining cash flows and a deteriorating balance sheet raises concerns, especially as rising project costs and customer concentration in its power segment could pose further risks. Given this mix of strengths and potential challenges, investors should wait for a more opportune entry point instead of adding this Zacks Rank #3 (Hold) stock to their portfolios.

Investors interested in the energy sector might look at some better-ranked stocks like Oceaneering International OII, Antero Midstream AM and Baytex Energy BTE, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Oceaneering International is valued at $2.48 billion. The company is a global provider of engineered services and products to the offshore energy, aerospace and defense industries. OII specializes in underwater robotics, remotely operated vehicles and subsea engineering solutions for offshore oil and gas exploration and production.

Antero Midstream is valued at $8.54 billion. It is a leading midstream energy company that provides natural gas gathering, compression and transportation services. Antero Midstream primarily operates in the Appalachian Basin, focusing on connecting producers with downstream markets, and manages a portfolio of infrastructure assets, including pipelines and processing plants.

Baytex Energy is valued at $2.54 billion. It is an oil and gas company that engages in the exploration, development and production of crude oil and natural gas in North America. Baytex Energy has operations in both the heavy oil sector of Alberta, Canada, and in the Eagle Ford shale of Texas, balancing its portfolio between conventional and unconventional energy resources.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite