|

|

|

|

|||||

|

|

|

Citigroup has had an impressive run over the past six months as its shares have beaten the S&P 500 by 25.6%. The stock now trades at $118.69, marking a 35.5% gain. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Citigroup, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons why C doesn't excite us and a stock we'd rather own.

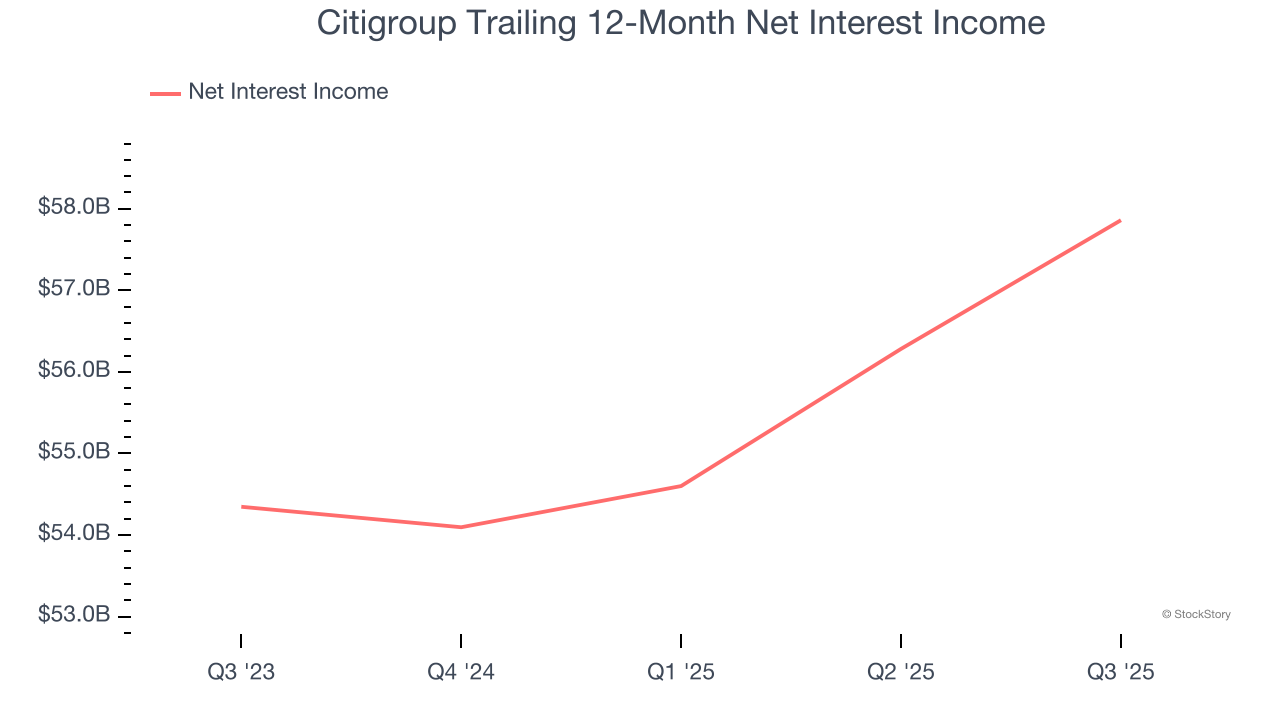

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Citigroup’s net interest income has grown at a 5.9% annualized rate over the last five years, worse than the broader banking industry.

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Citigroup’s net interest income to rise by 3.2%, close to its 3.2% annualized growth for the past two years.

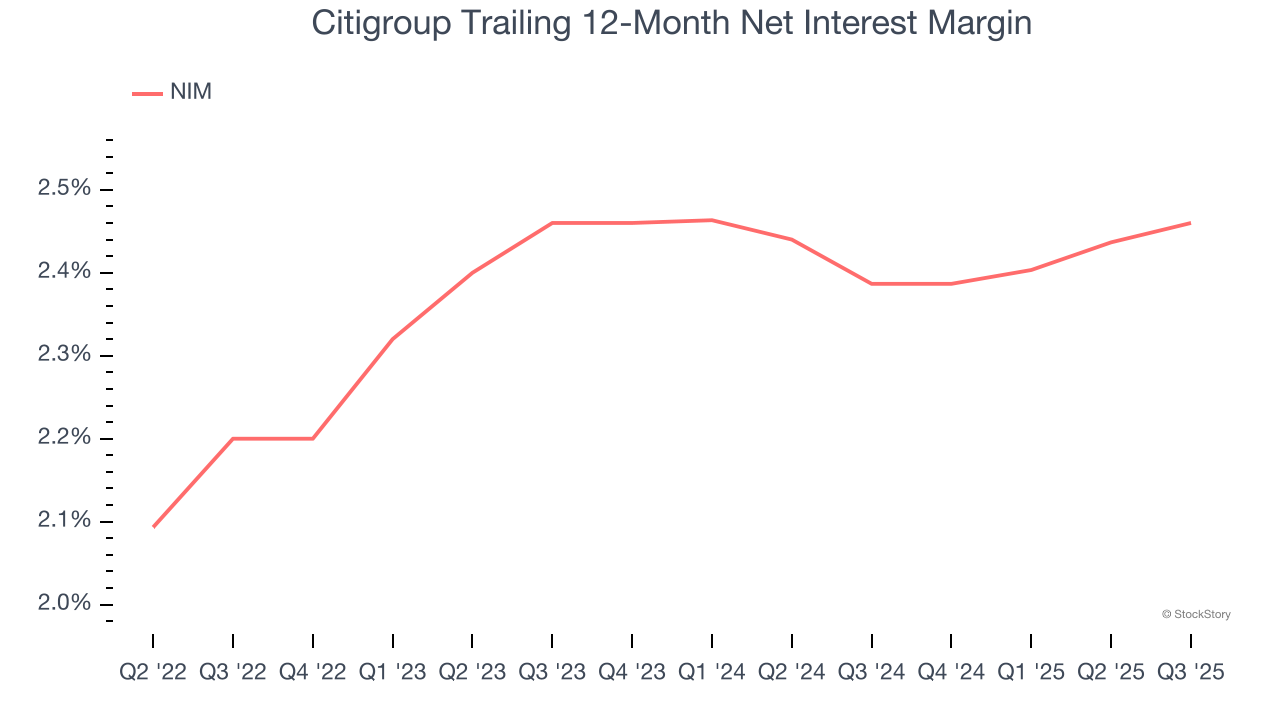

Net interest margin (NIM) serves as a critical gauge of a bank's fundamental profitability by showing the spread between interest income and interest expenses. It's essential for understanding whether a firm can sustainably generate returns from its lending operations.

Over the past two years, we can see that Citigroup’s net interest margin averaged a poor 2.4%, meaning it must compensate for lower profitability through increased loan originations.

Citigroup doesn’t pass our quality test. With its shares outperforming the market lately, the stock trades at 1.1× forward P/B (or $118.69 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find more timely opportunities elsewhere. We’d recommend looking at the most entrenched endpoint security platform on the market.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite