|

|

|

|

|||||

|

|

|

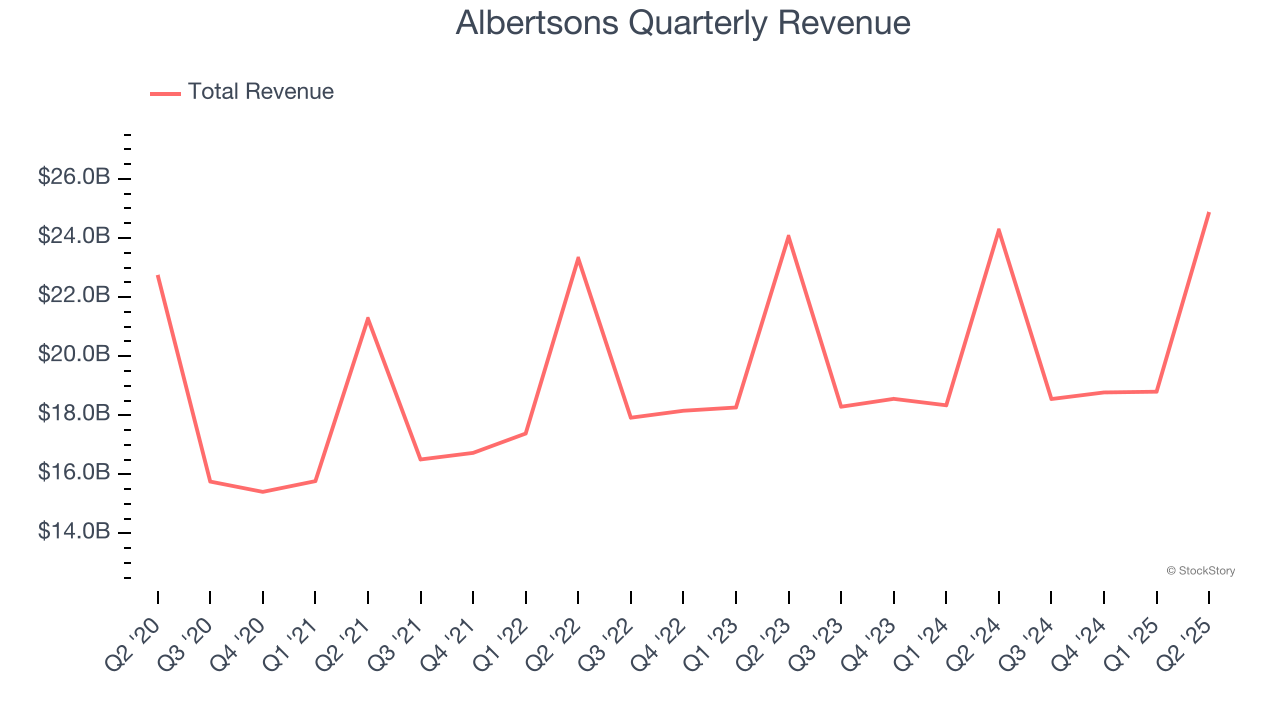

Grocery retailer Albertsons (NYSE:ACI) beat Wall Street’s revenue expectations in Q2 CY2025, with sales up 2.5% year on year to $24.88 billion. Its non-GAAP profit of $0.55 per share was in line with analysts’ consensus estimates.

Is now the time to buy Albertsons? Find out by accessing our full research report, it’s free for active Edge members.

"In the second quarter, we delivered solid operating and financial results while continuing to invest in our core business and elevate the customer experience," said Susan Morris, Chief Executive Officer.

With over 20 well-known grocery banners spanning 34 states, Albertsons (NYSE:ACI) operates food and drug retail stores across the US, offering groceries, pharmacy services, and own-brand products under banners like Safeway, Jewel-Osco, and Vons.

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $81.01 billion in revenue over the past 12 months, Albertsons is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because there is only so much real estate to build new stores, placing a ceiling on its growth. For Albertsons to boost its sales, it likely needs to adjust its prices or lean into foreign markets.

As you can see below, Albertsons’s 3.1% annualized revenue growth over the last three years was sluggish as its store footprint remained unchanged.

This quarter, Albertsons reported modest year-on-year revenue growth of 2.5% but beat Wall Street’s estimates by 0.6%.

Looking ahead, sell-side analysts expect revenue to grow 3.5% over the next 12 months, similar to its three-year rate. This projection is above average for the sector and suggests its newer products will help support its historical top-line performance.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

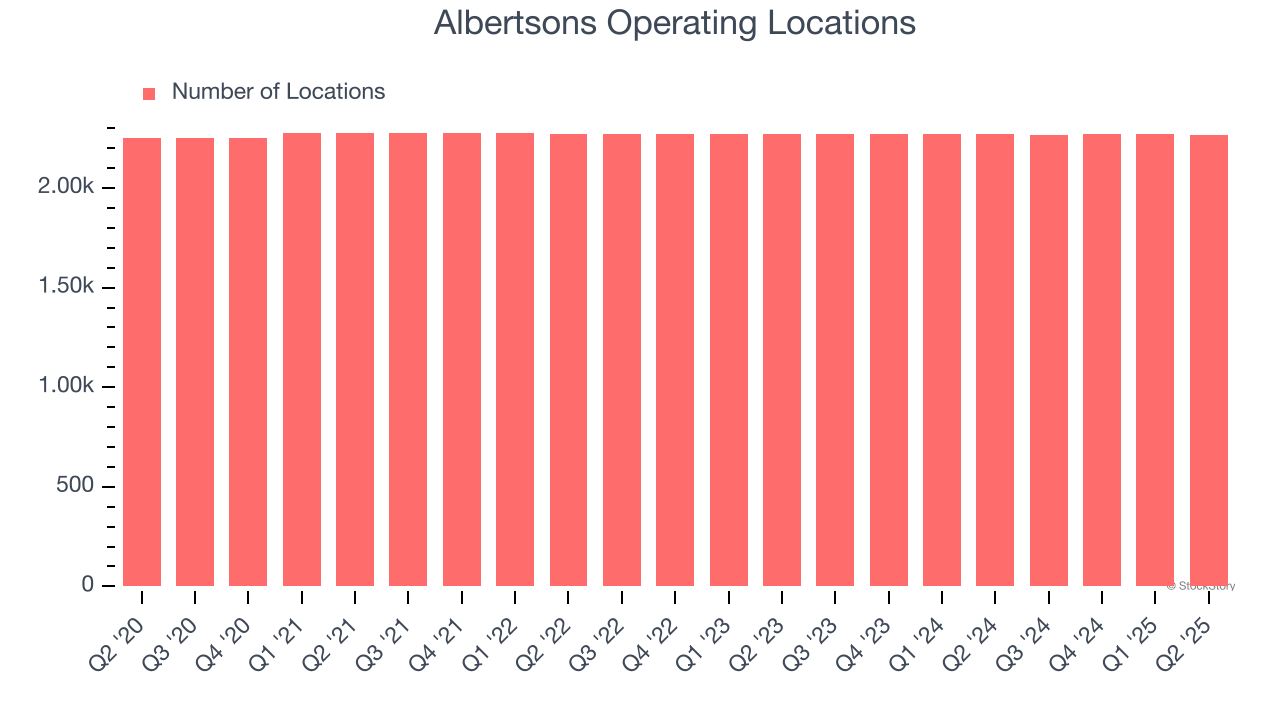

A retailer’s store count often determines how much revenue it can generate.

Albertsons operated 2,264 locations in the latest quarter, and over the last two years, has kept its store count flat while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

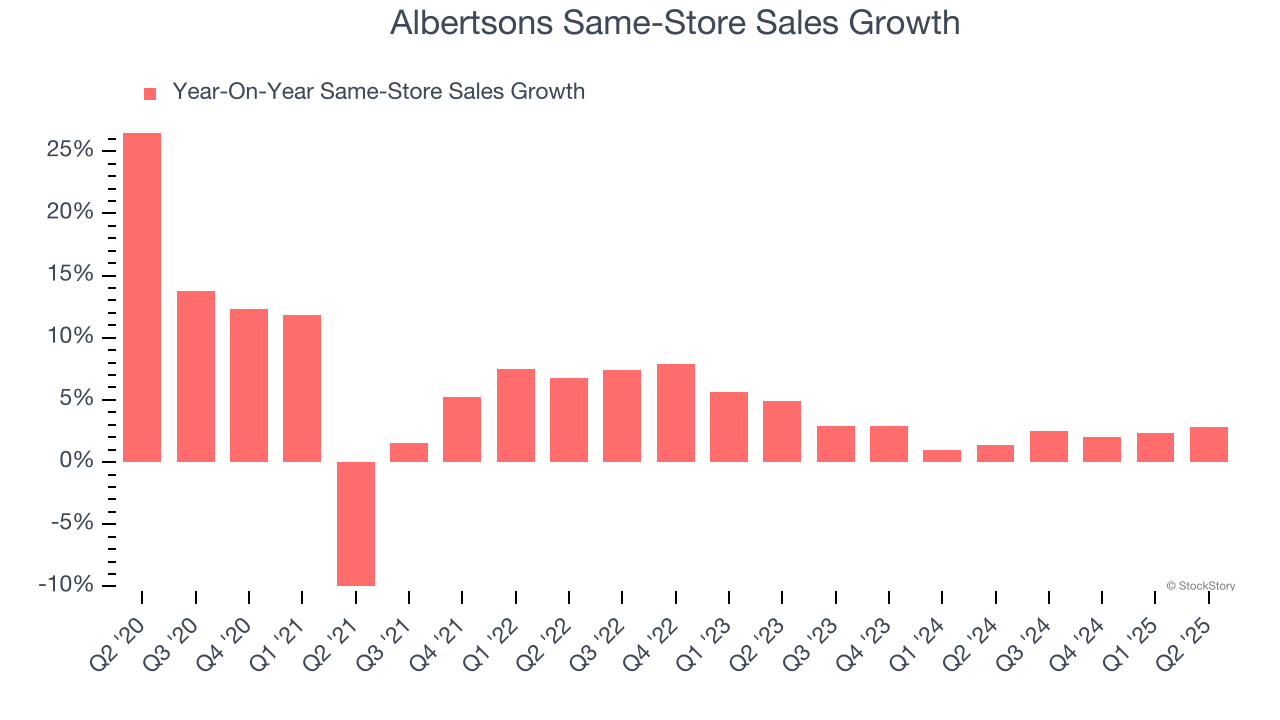

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Albertsons’s demand rose over the last two years and slightly outpaced the industry. On average, the company’s same-store sales have grown by 2.2% per year. Given its flat store base over the same period, this performance stems from not only increased foot traffic at existing locations but also higher e-commerce sales as demand shifts from in-store to online.

In the latest quarter, Albertsons’s same-store sales rose 2.8% year on year. This performance was more or less in line with its historical levels.

It was encouraging to see Albertsons beat analysts’ EBITDA expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its gross margin missed. Overall, this print had some key positives. The stock remained flat at $17.25 immediately following the results.

Is Albertsons an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| May-15 | |

| May-13 | |

| May-05 | |

| May-01 | |

| Apr-30 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-27 | |

| Apr-27 | |

| Apr-24 | |

| Apr-23 | |

| Apr-20 | |

| Apr-16 | |

| Apr-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite