|

|

|

|

|||||

|

|

|

Mercury General has had an impressive run over the past six months as its shares have beaten the S&P 500 by 27%. The stock now trades at $90.58, marking a 37.1% gain. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Mercury General, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons why MCY doesn't excite us and a stock we'd rather own.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Mercury General’s revenue to rise by 2.4%, a deceleration versus its 15.1% annualized growth for the past two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

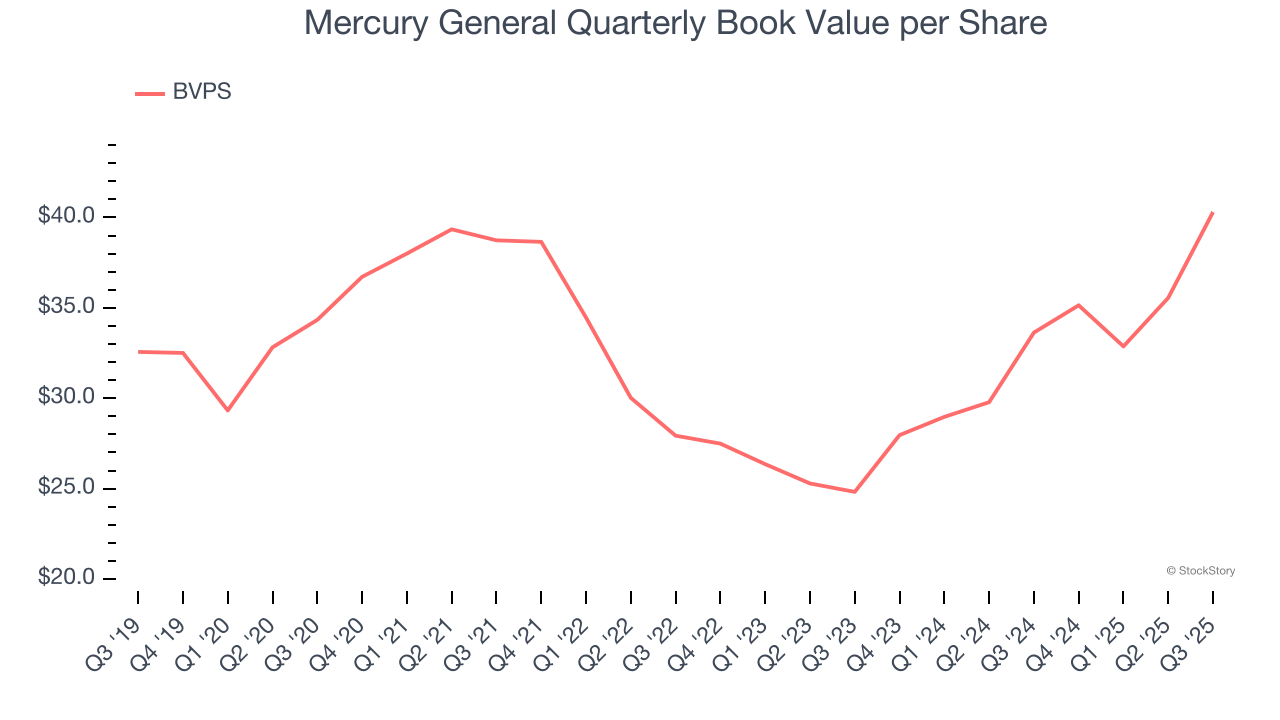

For insurers, book value per share (BVPS) is a vital measure of financial health, representing the total assets available to shareholders after accounting for all liabilities, including policyholder reserves and claims obligations.

Although Mercury General’s BVPS increased by a meager 3.3% annually over the last five years, the good news is that its growth has recently accelerated as BVPS grew at an incredible 27.4% annual clip over the past two years (from $24.82 to $40.30 per share).

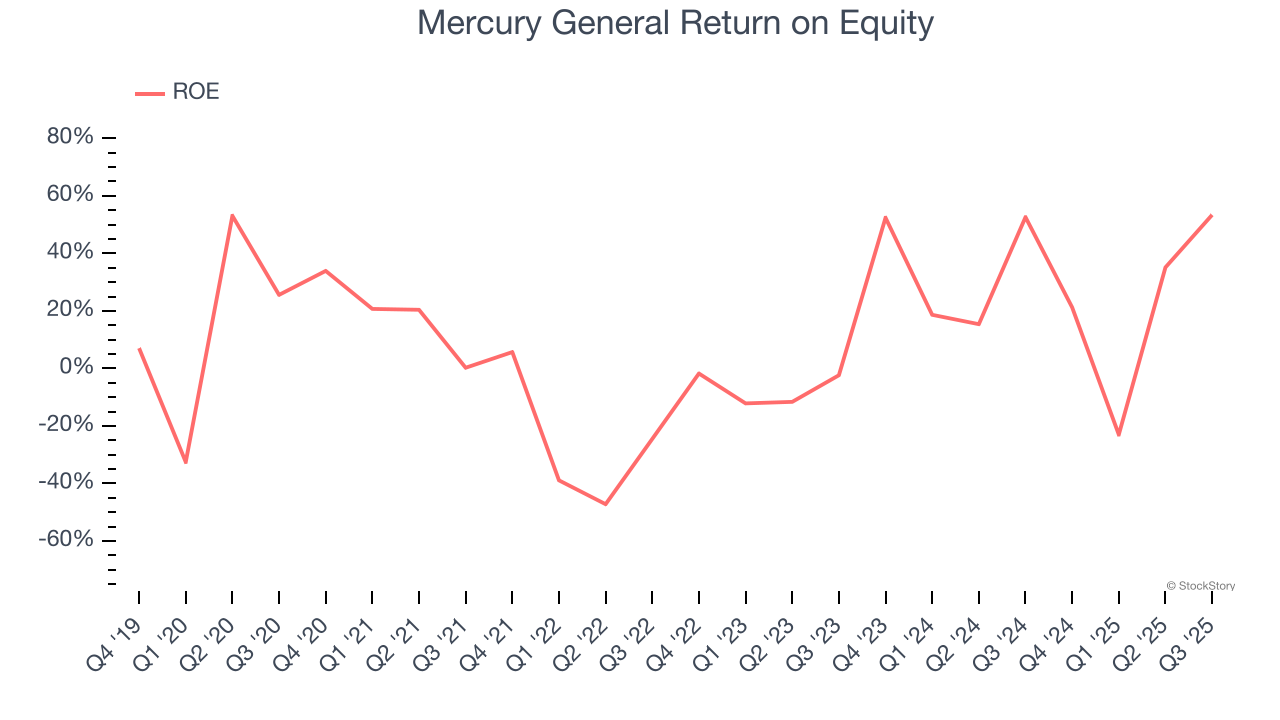

Return on equity, or ROE, represents the ultimate measure of an insurer's effectiveness, quantifying how well it transforms shareholder investments into profits. Over the long term, insurance companies with robust ROE metrics typically deliver superior shareholder returns through a balanced approach to capital management.

Over the last five years, Mercury General has averaged an ROE of 8.4%, uninspiring for a company operating in a sector where the average shakes out around 12.5%.

Mercury General isn’t a terrible business, but it isn’t one of our picks. With its shares beating the market recently, the stock trades at 2.1× forward P/B (or $90.58 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward the Amazon and PayPal of Latin America.

Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| 11 hours | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Jul-30 | |

| Jul-28 | |

| Jul-23 | |

| Jul-21 | |

| Jul-14 | |

| Jul-09 | |

| Jul-07 | |

| Jul-07 | |

| Jul-01 | |

| Jun-29 | |

| Jun-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite