|

|

|

|

|||||

|

|

|

Nutanix has gotten torched over the last six months - since July 2025, its stock price has dropped 34% to $50.84 per share. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Following the drawdown, is now the time to buy NTNX? Find out in our full research report, it’s free for active Edge members.

Originally pioneering hyperconverged infrastructure to break down traditional data center silos, Nutanix (NASDAQ:NTNX) provides a unified software platform that enables organizations to run applications and manage data across private, public, and hybrid cloud environments.

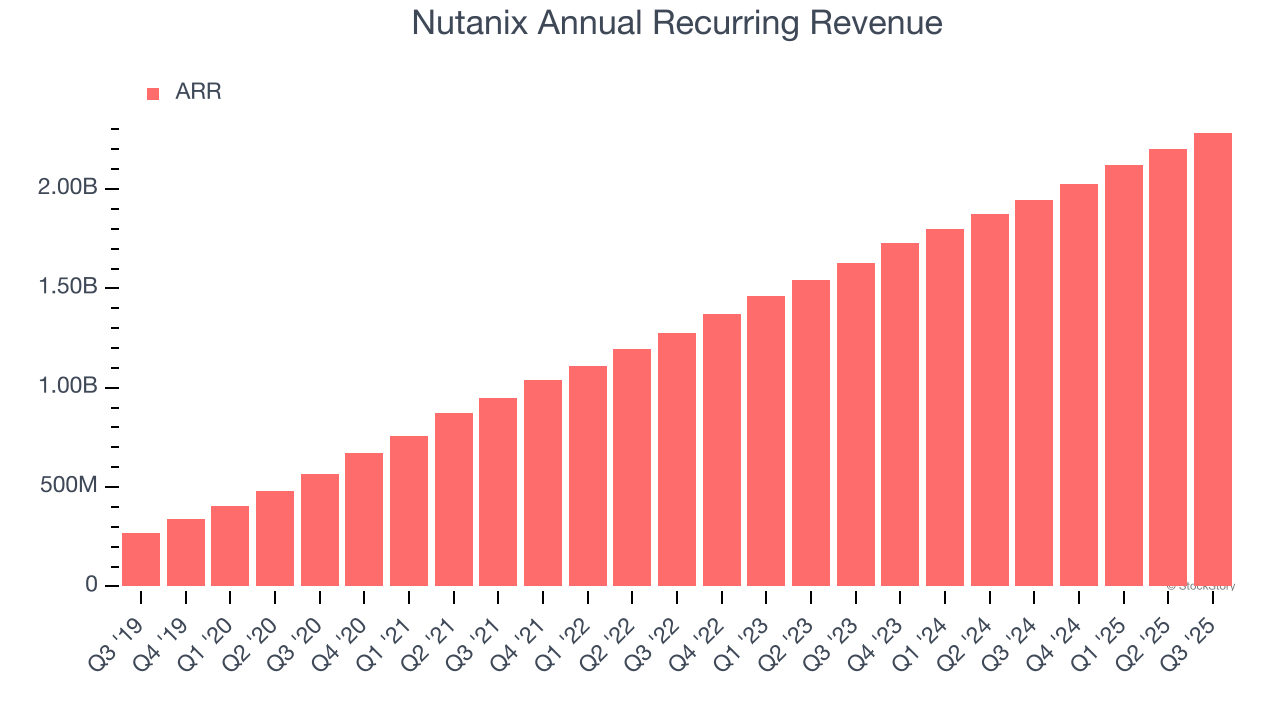

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Nutanix’s ARR punched in at $2.28 billion in Q3, and over the last four quarters, its year-on-year growth averaged 17.6%. This performance was solid, reflecting the company’s ability to maintain strong customer relationships and secure longer-term commitments. Its growth also contributes positively to Nutanix’s predictability and valuation, as investors typically prefer businesses with recurring revenue.

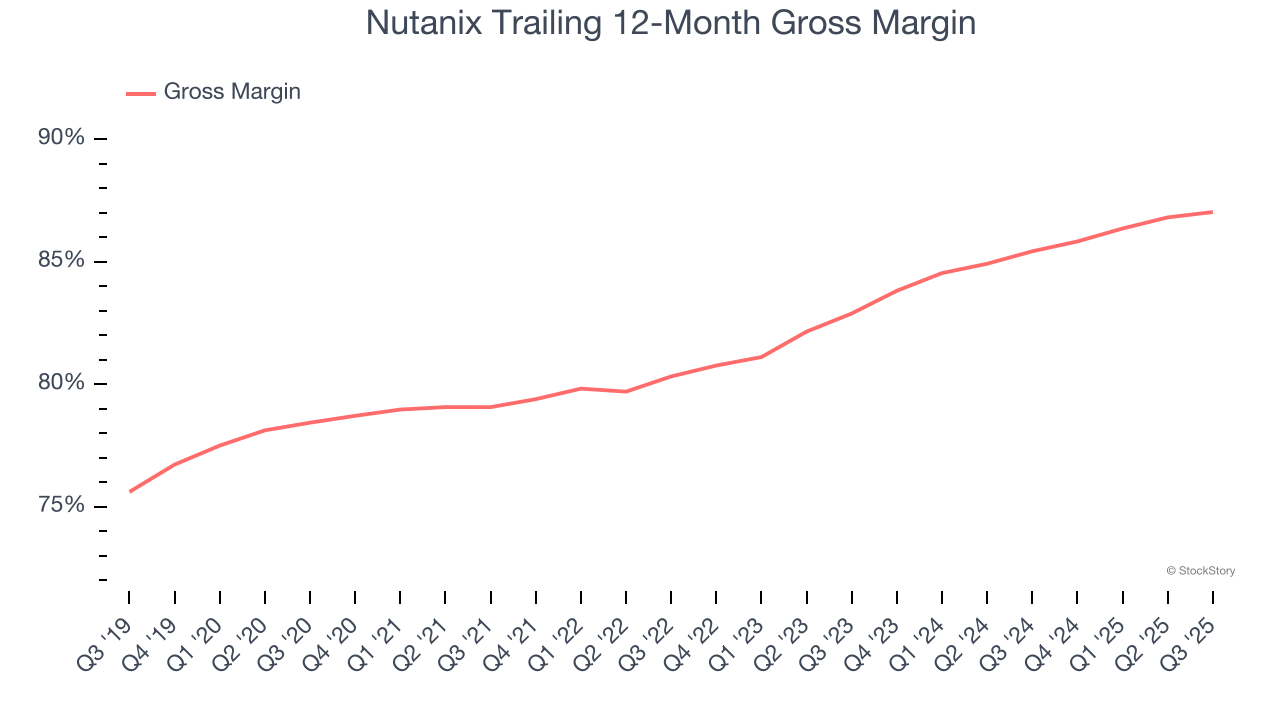

What makes the software-as-a-service model so attractive is that once the software is developed, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Nutanix’s gross margin is one of the highest in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 87% gross margin over the last year. Said differently, roughly $87.03 was left to spend on selling, marketing, and R&D for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Nutanix has seen gross margins improve by 4.1 percentage points over the last 2 year, which is very good in the software space.

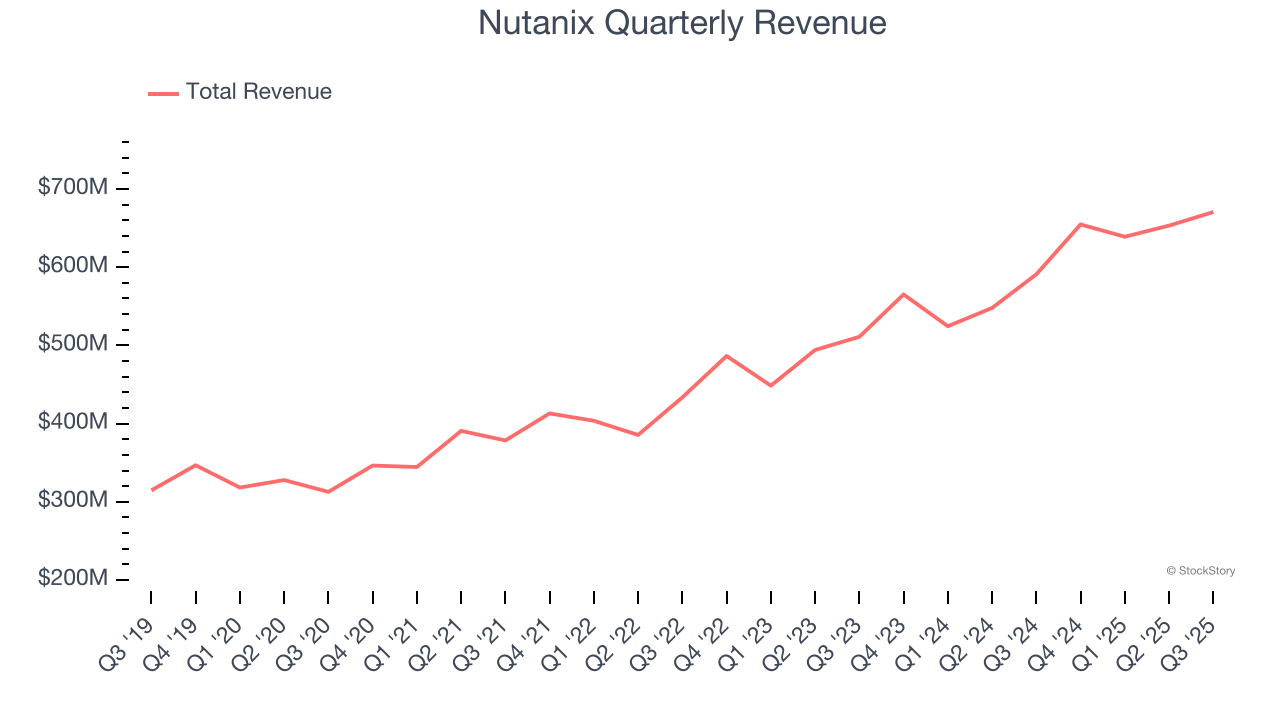

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Nutanix grew its sales at a 14.9% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the software sector, which enjoys a number of secular tailwinds. Luckily, there are other things to like about Nutanix.

Nutanix has huge potential even though it has some open questions. With the recent decline, the stock trades at 5.1× forward price-to-sales (or $50.84 per share). Is now the right time to buy? See for yourself in our full research report, it’s free for active Edge members.

Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jun-01 | |

| May-28 | |

| May-27 | |

| May-27 | |

| Apr-10 | |

| Apr-02 | |

| Mar-31 | |

| Mar-24 | |

| Mar-23 | |

| Mar-23 | |

| Mar-05 | |

| Mar-05 | |

| Feb-27 | |

| Feb-26 |

Apart From Nvidia, Stocks to Watch Thursday: Zoom, Trade Desk, Warner, Paramount

NTNX

The Wall Street Journal

|

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite