|

|

|

|

|||||

|

|

|

Over the last six months, Disney’s shares have sunk to $114.05, producing a disappointing 7.4% loss - a stark contrast to the S&P 500’s 10.1% gain. This might have investors contemplating their next move.

Is now the time to buy Disney, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Even though the stock has become cheaper, we're cautious about Disney. Here are three reasons you should be careful with DIS and a stock we'd rather own.

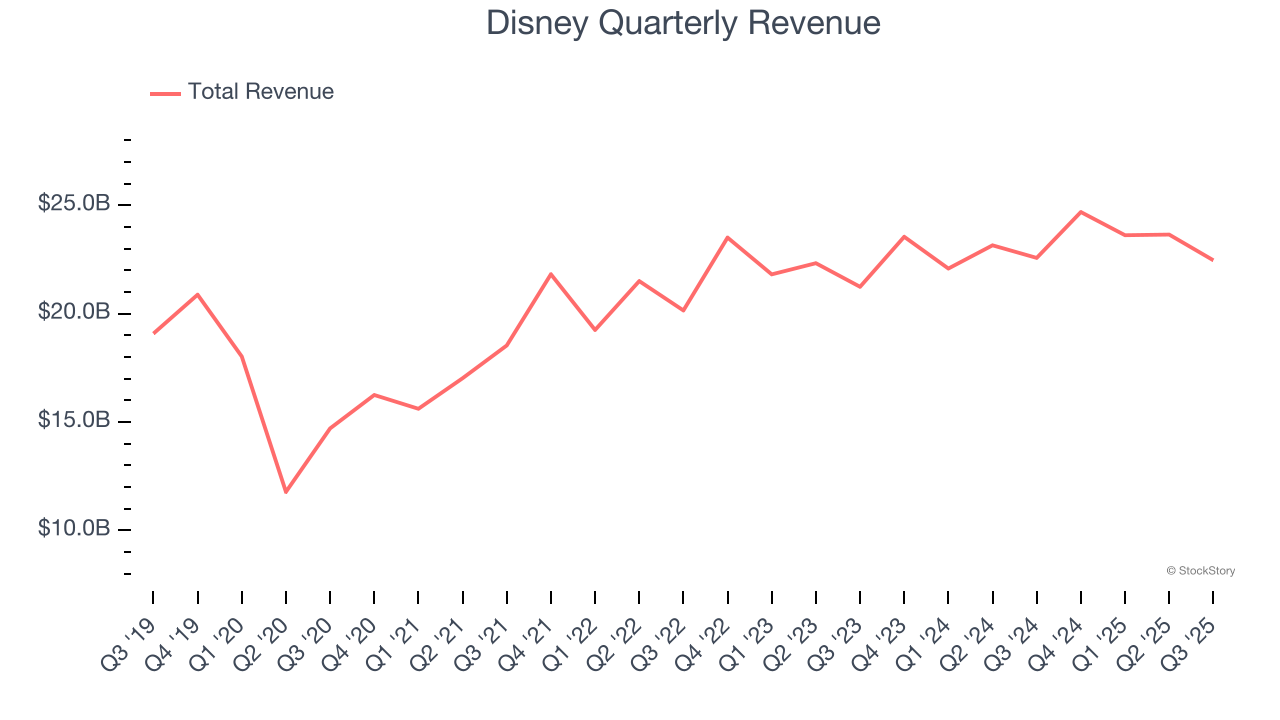

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Disney’s sales grew at a weak 7.6% compounded annual growth rate over the last five years. This was below our standard for the consumer discretionary sector.

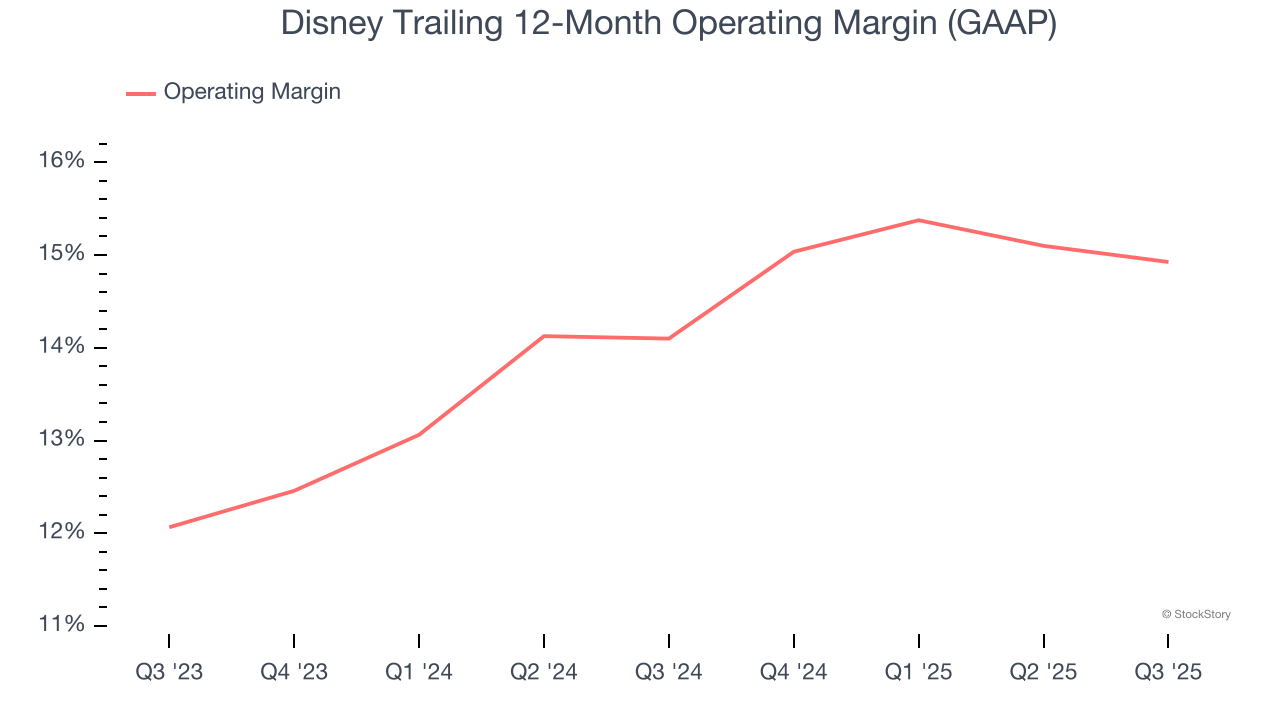

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Disney’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 14.5% over the last two years. This profitability was inadequate for a consumer discretionary business and caused by its suboptimal cost structure.

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict Disney’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 10.7% for the last 12 months will decrease to 9.9%.

Disney falls short of our quality standards. After the recent drawdown, the stock trades at 16.9× forward P/E (or $114.05 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are better investments elsewhere. Let us point you toward an all-weather company that owns household favorite Taco Bell.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| 6 hours | |

| 12 hours | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite