|

|

|

|

|||||

|

|

|

Carnival Corporation & plc CCL closed fiscal 2025 with clear signs of improved revenue flow-through, an important development amid evolving demand and capacity dynamics across the cruise industry. Management highlighted that operating income per available lower berth day reached its highest level in nearly two decades, underscoring the company’s ability to convert revenue growth into profitability.

This improvement reflects the nature of Carnival’s operating model, where a significant portion of ship-level expenses is largely set once vessels are deployed. As occupancy, pricing and onboard spending strengthened during fiscal 2025, costs were spread across a higher revenue base. Management noted that this supported meaningful margin expansion, even as the company absorbed higher dry-dock activity, destination-related investments and ongoing inflationary pressures.

Carnival also pointed to ongoing sourcing efficiencies, operational discipline and scale benefits as contributing factors. Cruise costs excluding fuel increased at a measured pace relative to revenue growth, allowing incremental yield gains to translate into stronger operating performance. Management emphasized that cost mitigation initiatives continued to offset inflation, aiding in preserving margins as operations scaled.

Looking ahead, the improved conversion of revenues into profitability likely supports a more balanced earnings profile for Carnival. While demand trends and industry capacity remain key variables, the company’s ability to generate higher profitability from its existing fleet highlights growing efficiency within the operating model. As revenues build on a moderately growing cost base that remains well-controlled relative to revenue growth, flow-through dynamics are becoming a more visible and durable element of Carnival’s earnings profile.

Shares of Carnival have gained 9.8% in the past three months compared with the industry’s growth of 2.5%. In the same time frame, other industry players like Royal Caribbean Cruises Ltd. RCL and Norwegian Cruise Line Holdings Ltd. NCLH have declined 11% and 5.6%, respectively, while OneSpaWorld Holdings Limited OSW has gained 1.9%.

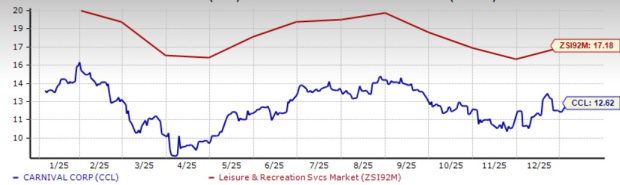

CCL stock is currently trading at a discount. It is currently trading at a forward 12-month price-to-earnings (P/E) multiple of 12.62, well below the industry average of 17.18. Conversely, industry players, such as Royal Caribbean, Norwegian Cruise and OneSpaWorld have P/E ratios of 15.6, 8.43 and 18.49, respectively.

The Zacks Consensus Estimate for Carnival’s fiscal 2025 earnings per share has been revised upward, increasing from $2.40 to $2.47 over the past 30 days. This upward trend indicates strong analyst confidence in the stock’s near-term prospects.

The company is likely to report solid earnings, with projections indicating a 9.8% rise in fiscal 2026. Conversely, industry players like Royal Caribbean, Norwegian Cruise and OneSpaWorld are likely to witness a rise of 32.5%, 15.9% and 20%, respectively, year over year in 2026 earnings.

CCL stock currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-03 | |

| Aug-03 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite