|

|

|

|

|||||

|

|

|

ANI Pharmaceuticals’ ANIP stock has risen 21% in the past six months, all thanks to the encouraging financial performance of the company during the first nine months of 2025.

In November, ANIP reported Q3 beats on both sales and earnings — continuing a trend of quarterly outperformance seen throughout 2025. Along with these results, the company has raised its full-year 2025 guidance with each earnings report, reflecting management’s confidence and operational consistency.

ANI Pharmaceuticals now expects full-year sales of $854-$873 million (previously: $818-$843 million) and EPS in the range of $7.37-$7.64 (up from $6.98-$7.35). This updated guidance suggests annual growth of 39-42% in sales and 42-47% in earnings.

Let’s examine the company’s fundamentals to gain a deeper understanding of how to approach the stock amid this price rise.

So far in 2025, the company’s rare disease franchise has added $291 million to the top line. This number has more than doubled compared with the year-ago period, driven by increased demand for the ACTH-based injection Cortrophin Gel. ANI Pharmaceuticals expects to close 2025 with about half of its overall revenues coming from the sale of its rare disease products.

A major portion of the franchise’s revenues was generated from Cortrophin Gel. Sales of this drug have surged 70% year over year to $236 million in the first nine months of 2025. This uptick was driven by increased demand across all specialties — neurology, rheumatology, nephrology and ophthalmology — aided by an expanded sales force and broader prescriber adoption. ANIP expects to close 2025 with the drug’s sales between $347 million and $352 million, reflecting a 75-78% increase over the prior year.

We expect this momentum to continue in 2026, further supported by new clinical studies (including a phase IV study in acute gouty arthritis) and ANIP’s ongoing efforts to deepen specialty penetration.

The rare disease portfolio is also expected to receive a boost in sales from the recently acquired ophthalmology drugs Iluvien and Yutiq, which were added through the September 2024 acquisition of Alimera Sciences. Although sales of both drugs were impacted in 2025 due to ongoing reimbursement challenges, particularly reduced Medicare access and continued utilization of remaining inventory at physician offices, ANI Pharmaceuticals expects sales growth to recover in 2026. This is supported by an expanded ophthalmology sales effort, improved patient access and a significantly larger addressable patient population — about 10 times the size of current usage.

ANI Pharmaceuticals delivered encouraging growth in its generics segment during the first nine months of 2025, with revenues increasing 27% year over year to over $283 million. This uptick was supported by healthy core volumes, incremental contributions from recent launches and a temporary boost from a partnered generic introduced late in the third quarter. The product benefited from a short window of limited competition, helping Q3 results exceed expectations that had previously factored in a sequential decline.

With additional competing products introduced in Q4, the company expects generics revenues to fall from third-quarter levels. Competitive pressures across the generics landscape remain elevated. The expanding presence of biosimilars is enhancing the negotiating leverage of payers and providers, often translating into steeper pricing concessions to secure formulary access. These conditions could weigh on pricing power and margins, particularly in more cost-sensitive therapeutic categories.

In addition, competition from established generic players like Teva Pharmaceutical TEVA and Amneal Pharmaceuticals AMRX may drive higher spending on commercial and support activities, contributing to near-term cost headwinds.

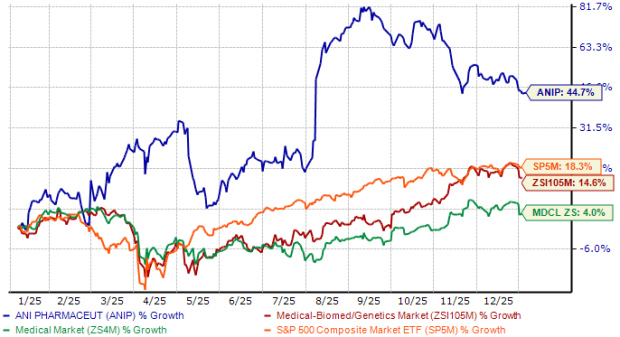

Shares of ANIP have surged 45% in the past year compared with the industry’s 15% growth. The stock has also outperformed the sector and the S&P 500 during the same period, as shown in the chart below.

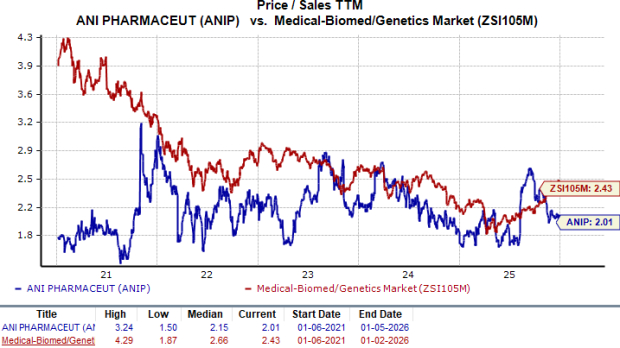

The company is trading at a discount to the industry. Going by the price/sales (P/S) ratio, the stock currently trades at 2.01 times trailing 12-month sales value, lower than 2.43 times for the industry.

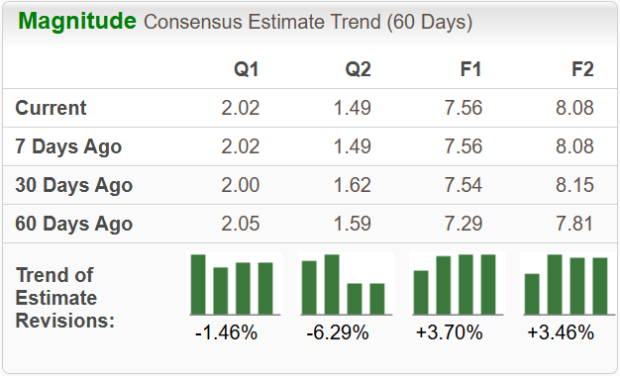

Estimates for ANI Pharmaceuticals’ 2025 and 2026 EPS have increased over the past 60 days.

ANI Pharmaceuticals continues to build momentum within its rare disease portfolio, with recent quarters highlighting disciplined execution and improving operating trends. Although competitive pressures in the generics segment are expected to increase in the near term, the business should remain a reliable source of revenue growth, supported by targeted launches and a solid U.S.-based manufacturing infrastructure.

Looking ahead, the company’s growth profile remains favorable, driven by continued strength in Cortrophin Gel and rising adoption of its ophthalmology products. These factors position ANI Pharmaceuticals to maintain earnings durability while further expanding its presence in higher-margin specialty areas.

Taken together, ANI Pharmaceuticals appears well placed to support sustained profitability and long-term value creation. This outlook is further supported by the stock’s current Zacks Rank #1 (Strong Buy). Despite a stellar performance last year, ANIP continues to trade below industry valuation benchmarks, leaving scope for additional upside if execution remains consistent.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-21 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-13 | |

| Jul-10 |

Teva and Polpharma Biologics sign global deal for ocrelizumab biosimilar

TEVA

Pharmaceutical Technology

|

| Jul-09 | |

| Jul-09 | |

| Jul-08 |

Teva draws up mid-stage study plans for vitiligo asset on Phase Ib success

TEVA

Clinical Trials Arena

|

| Jul-07 | |

| Jun-29 | |

| Jun-18 | |

| Jun-18 | |

| Jun-18 | |

| Jun-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite