|

|

|

|

|||||

|

|

|

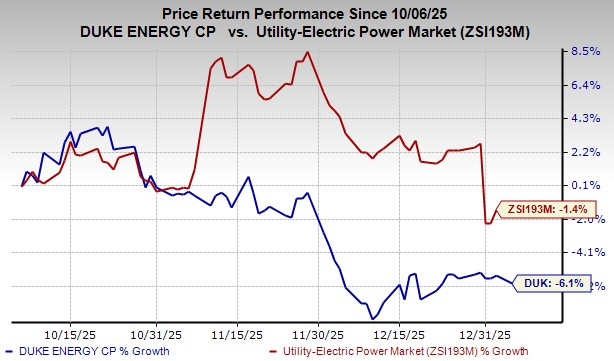

Duke Energy DUK shares have declined 6.1% over the past three months compared with the Zacks Utility-Electric Power industry’s deterioration of 1.4%. The company faces financial pressure from rising leverage and interest expenses.

Some other operators in the same industry, NextEra Energy NEE and DTE Energy DTE, also face risks related to higher debt levels. NextEra Energy’s long-term debt, as of Sept. 30, 2025, was $84.17 billion, up from $72.4 billion on Dec. 31, 2024. DTE Energy’s long-term debt, as of Sept. 30, 2025, was $24.5 billion, up from $20.7 billion as of Dec. 31, 2024.

Shares of NEE and DTE have declined 1.1% and 9.2%, respectively, over the past three months.

Given Duke Energy’s current stock price underperformance, what should investors do now? Let’s find out through certain factors.

Duke Energy’s elevated leverage continues to pressure its financial profile by increasing overall financial risk and driving up borrowing costs. The company’s long-term debt rose to $79.3 billion as of Sept. 30, 2025, from $76.34 billion at the end of 2024. This higher debt burden has translated into rising financing costs, with interest expense increasing nearly 7% year over year to $2.69 million during the first nine months of 2025. Duke Energy could face reduced financial flexibility and higher costs of capital, which may weigh on future earnings and cash flows.

Unfavorable weather events like storms and hurricanes often take place in service territories. This, in turn, causes outages for millions of customers as well as damaged infrastructure. During 2024, hurricanes Debby, Helene and Milton significantly affected Duke Energy Carolinas, Duke Energy Progress and Duke Energy Florida’s territories. Approximately 3.5 million customers were affected across Duke Energy's system by Hurricane Helen, 70,000 customers by Hurricane Debby and more than 1 million customers by Hurricane Milton. As of Sept. 30, 2025, the total cumulative operations and maintenance expense incurred for restoration and rebuilding of infrastructure associated with the hurricanes was nearly $789 million.

Duke Energy is gaining momentum through its broad energy mix, ongoing investments in modern technology and infrastructure. By combining renewable resources, such as solar and wind, with conventional sources like nuclear, coal and natural gas, the company ensures reliable services for its customers.

DUK is rapidly advancing its clean-energy transition by planning to cut coal generation to under 5% by 2030 and fully eliminate coal by 2035, supported by retiring 58 coal units totaling 8,000 megawatt (MW). The company has also committed to net-zero methane emissions by 2030 and net-zero carbon emissions by 2050. To support this shift, it aims to add more than 7,500 MW of new, lower-emission natural-gas generation by 2030.

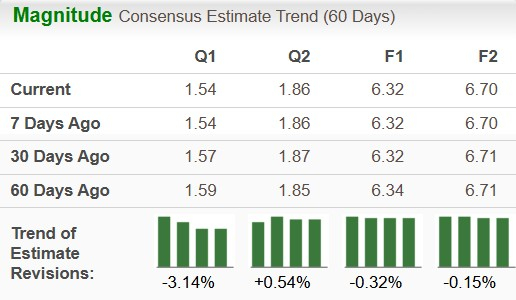

The Zacks Consensus Estimate for DUK’s 2026 earnings per share (EPS) has declined 0.15% in the past 60 days. DUK’s long-term (three to five years) earnings growth rate is 6.87%.

The Zacks Consensus Estimate for NextEra Energy’s 2026 EPS has increased 0.5% in the past 60 days. NEE’s long-term earnings growth rate is 8.08%. The Zacks Consensus Estimate for DTE Energy’s 2026 EPS has declined 0.13% in the past 60 days. DTE’s long-term earnings growth rate is 7.06%.

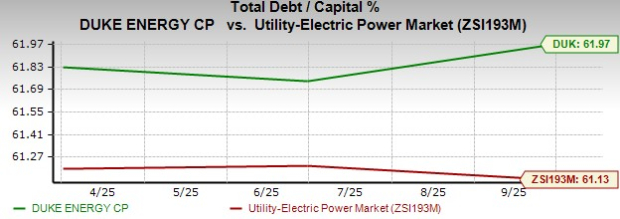

Currently, the company’s total debt to capital is 61.97%, higher than the industry’s average of 61.13%.

The company’s current ratio is 0.63. A current ratio less than one indicates that the company's current liabilities are greater than its current assets, which means it may struggle to meet its short-term obligations.

The consistently strong performance of the company has enabled it to reward its shareholders through annual dividend rate hikes. Currently, its annual dividend is $4.26 per share. The company’s current dividend yield of 3.65% is better than the industry’s average of 2.92%.

Duke Energy’s targeted dividend payout ratio is in the range of 60-70%. It is anticipated that the company will continue to increase its dividend in the future, driven by its sustained earnings growth. Check Duke Energy’s dividend history here.

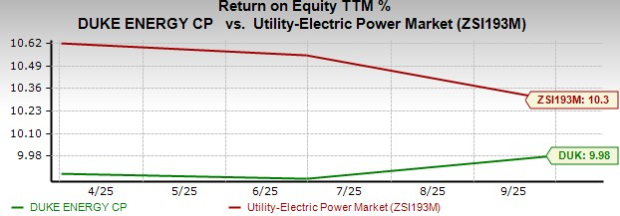

Duke Energy’s trailing 12-month return on equity of 9.98% is lower than the industry average of 10.3%. Return on equity, a profitability measure, reflects how effectively a company utilizes its shareholders’ funds to generate income.

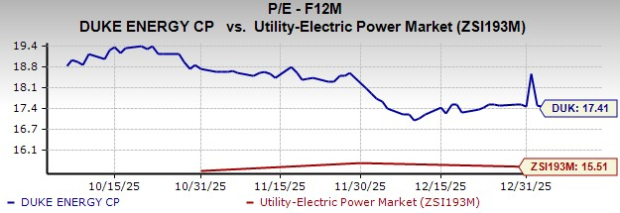

Duke Energy is currently trading at 17.41X, a premium compared to its industry’s 15.51X on a forward 12-month P/E basis.

Duke Energy is accelerating its clean-energy transition through a diverse power mix, major infrastructure investments and a long-term commitment to modern technologies. However, the company faces risks related to high debt levels and rising costs from severe weather events.

Given DUK’s premium valuation, lower ROE, higher debt level and lower current ratio, the investors may consider avoiding this Zacks Rank #4 (Sell) stock at the moment.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite