|

|

|

|

|||||

|

|

|

Mattel has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 6.5% to $21.31 per share while the index has gained 10.8%.

Is now the time to buy Mattel, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

We're swiping left on Mattel for now. Here are three reasons you should be careful with MAT and a stock we'd rather own.

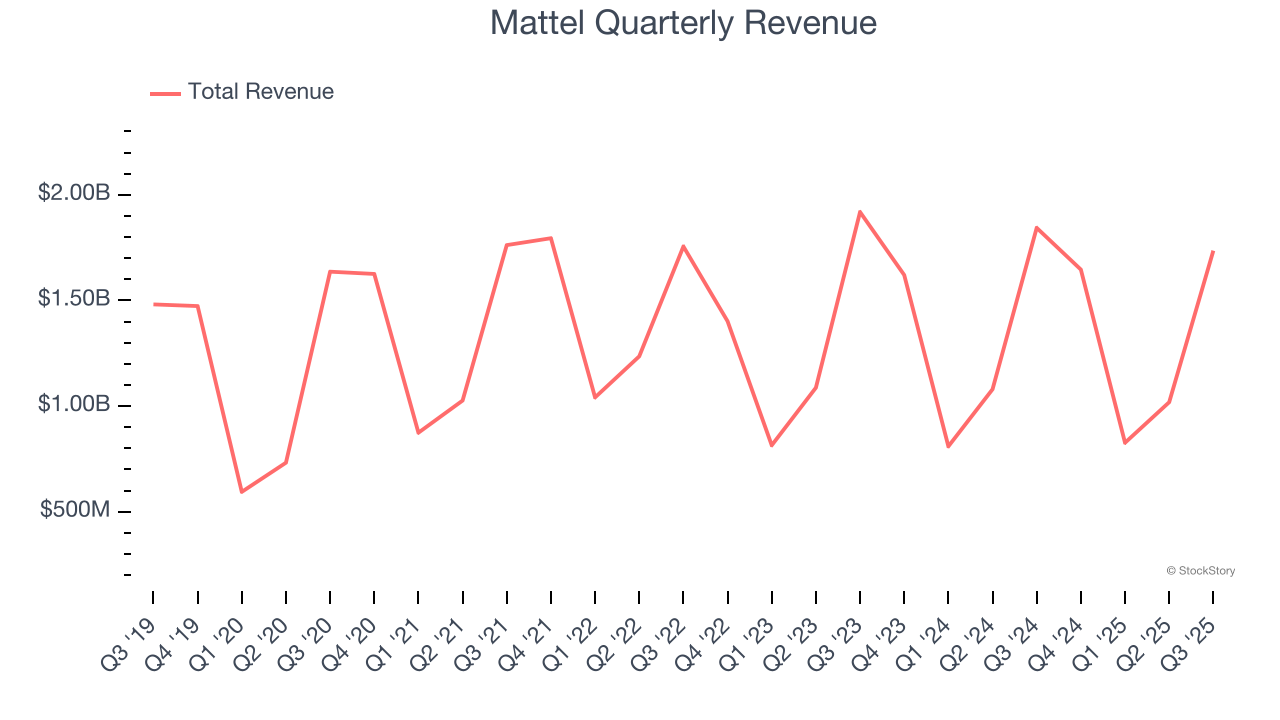

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Mattel’s sales grew at a weak 3.3% compounded annual growth rate over the last five years. This was below our standard for the consumer discretionary sector.

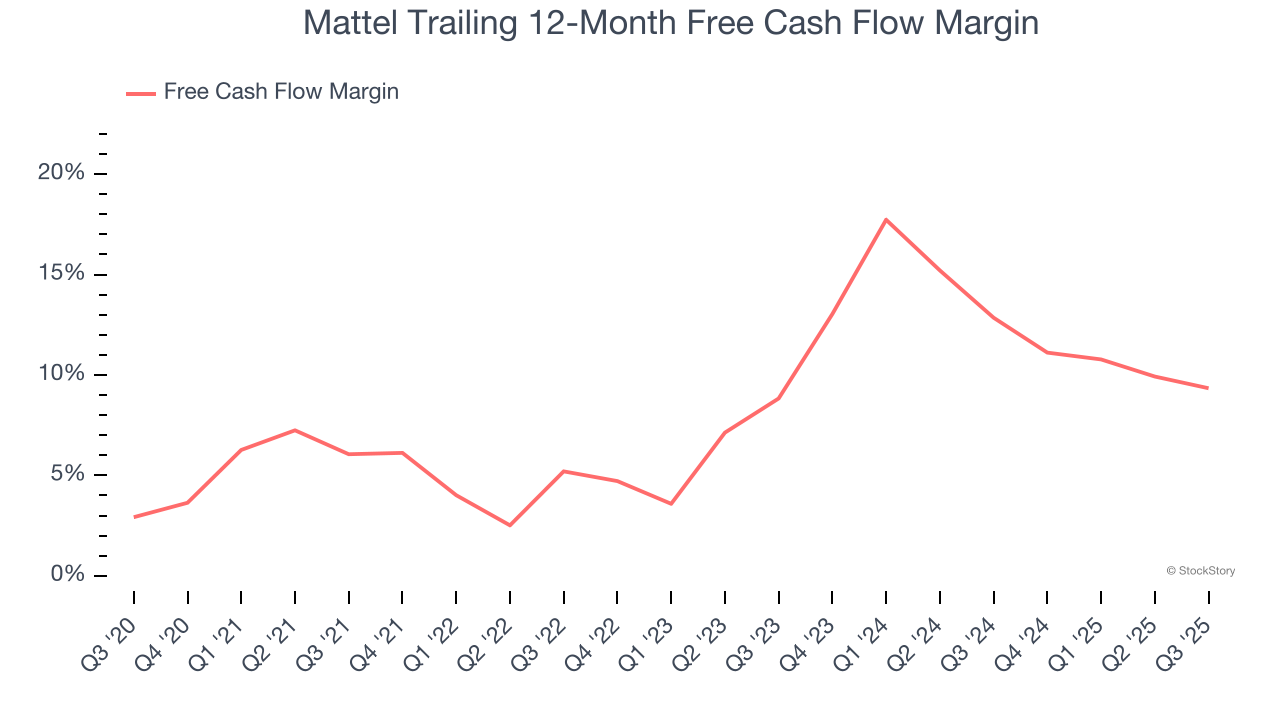

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Mattel has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 11.1%, lousy for a consumer discretionary business.

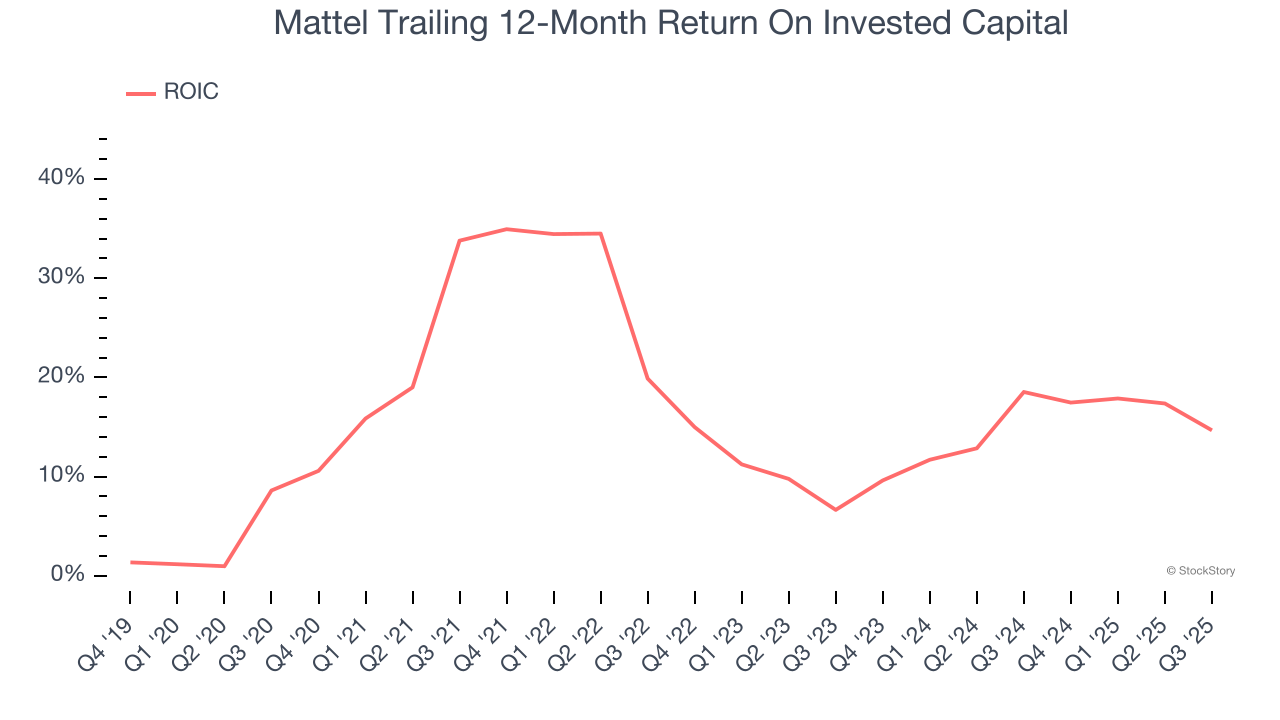

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Mattel’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

We see the value of companies helping consumers, but in the case of Mattel, we’re out. That said, the stock currently trades at 12× forward P/E (or $21.31 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better investments elsewhere. We’d suggest looking at an all-weather company that owns household favorite Taco Bell.

Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Apr-09 | |

| Apr-08 | |

| Apr-07 | |

| Mar-30 | |

| Mar-24 | |

| Mar-13 | |

| Mar-12 | |

| Mar-05 | |

| Mar-04 | |

| Mar-02 | |

| Mar-02 | |

| Feb-23 | |

| Feb-20 | |

| Feb-19 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite