|

|

|

|

|||||

|

|

|

Shareholders of Stride would probably like to forget the past six months even happened. The stock dropped 50.2% and now trades at $68.80. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Following the pullback, is this a buying opportunity for LRN? Find out in our full research report, it’s free for active Edge members.

Formerly known as K12, Stride (NYSE:LRN) is an education technology company providing education solutions through digital platforms.

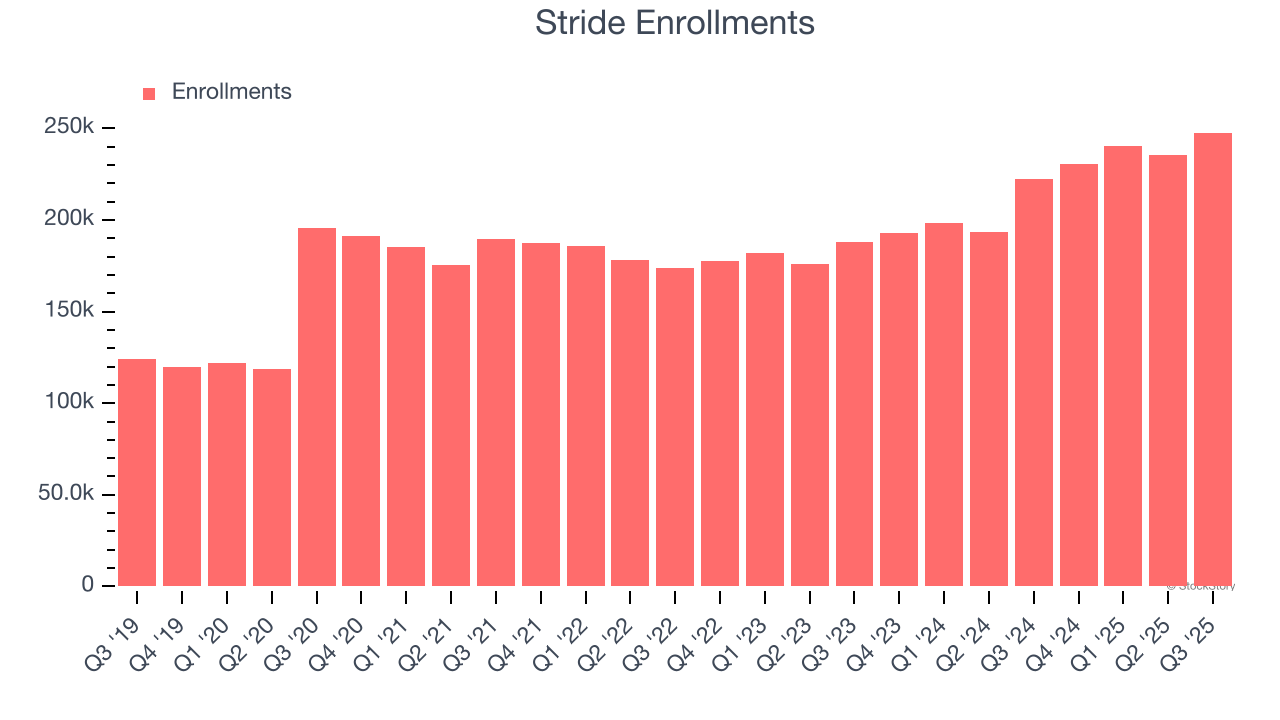

Revenue growth can be broken down into changes in price and volume (for companies like Stride, our preferred volume metric is enrollments). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Stride’s enrollments punched in at 247,700 in the latest quarter, and over the last two years, averaged 15% year-on-year growth. This performance was fantastic and shows its services have a unique value proposition.

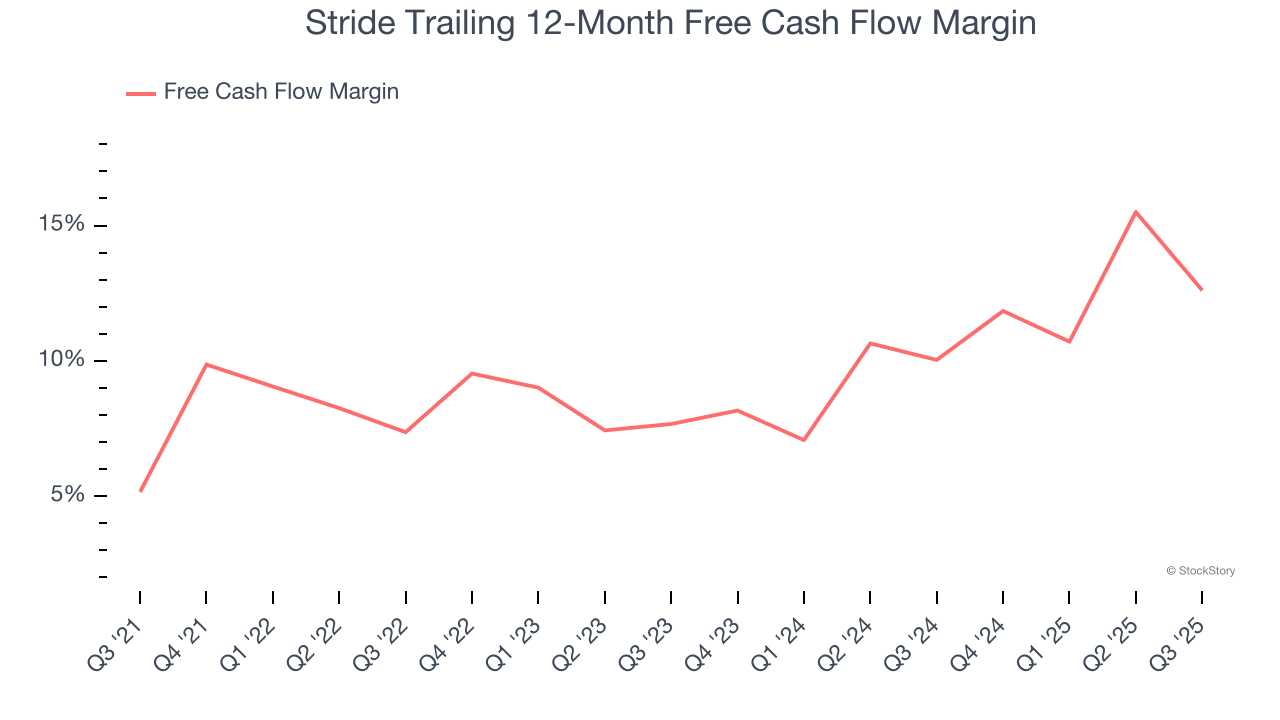

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Stride’s margin expanded by 7.4 percentage points over the last five years. This is encouraging because it gives the company more optionality. Stride’s free cash flow margin for the trailing 12 months was 12.6%.

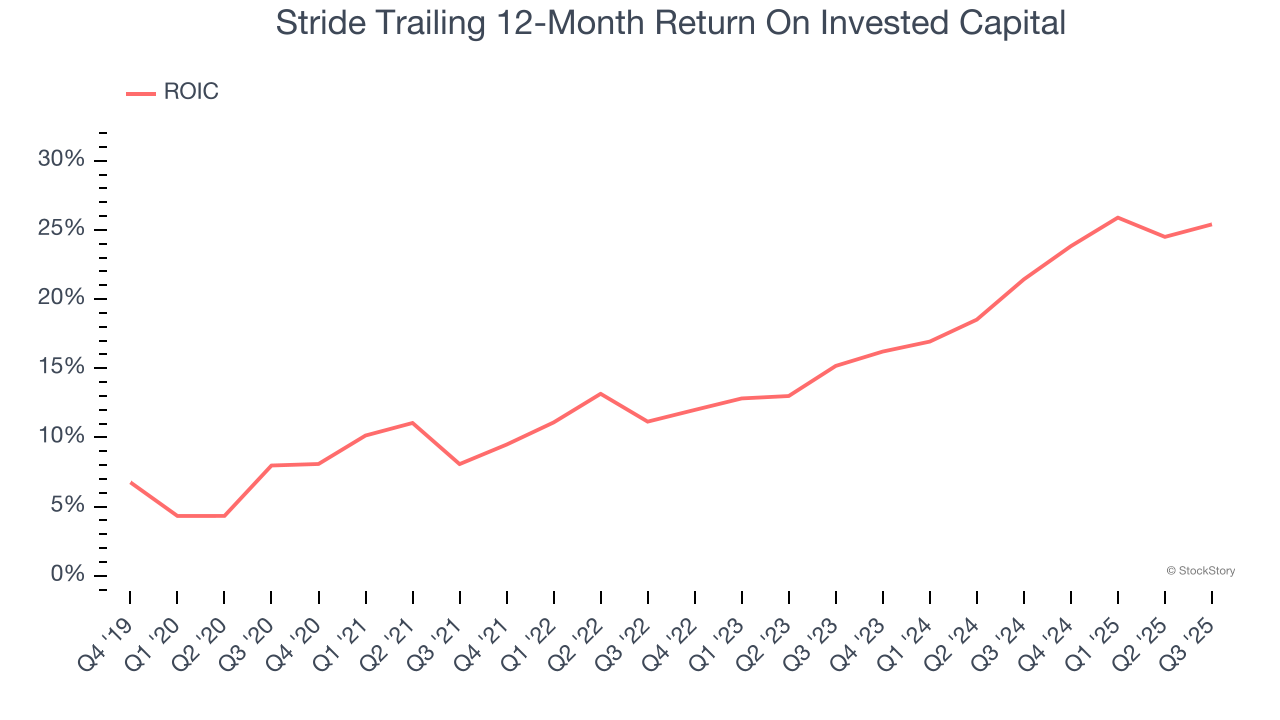

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Stride’s ROIC has increased significantly over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

These are just a few reasons why we think Stride is an elite business services company. After the recent drawdown, the stock trades at 8.2× forward P/E (or $68.80 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free for active Edge members .

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Jul-30 | |

| Jul-29 | |

| Jul-21 | |

| Jul-14 | |

| Jun-05 | |

| May-02 | |

| Apr-29 | |

| Apr-29 | |

| Apr-28 | |

| Apr-14 | |

| Apr-01 | |

| Mar-12 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite