|

|

|

|

|||||

|

|

|

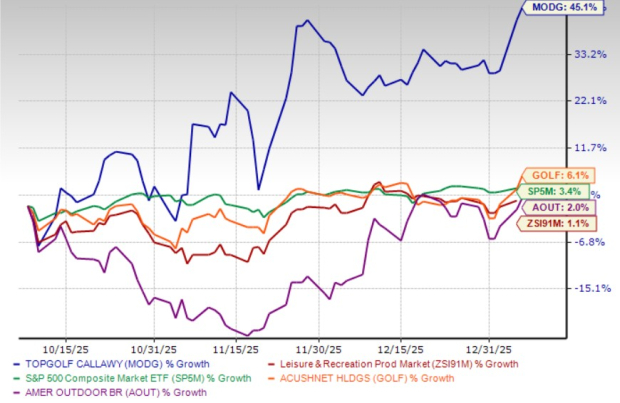

Shares of the company Topgolf Callaway Brands Corp. MODG have surged 45.1% compared with the industry and the S&P 500’s growth of 1.1% and 3.4%, respectively.

Shares of Topgolf Callaway have rallied as investors reacted to a clear operational turnaround highlighted in third-quarter 2025. The company posted better-than-expected results, led by a sharp rebound in Topgolf traffic following new value-driven initiatives that lifted same-venue sales back into positive territory, particularly in the core 1-2 bay segment. Continued strength in the Golf Equipment business, steady market share gains, improved balance sheet metrics and raised full-year revenue and EBITDA guidance further supported confidence in the company’s improving execution, helping drive the recent surge in the share price.

In the same time frame, shares of other companies like Acushnet Holdings Corp. GOLF and American Outdoor Brands, Inc. AOUT have gained 6.1% and 2%, respectively.

Shares of Topgolf Callaway were buoyed by a clear operational inflection at Topgolf during the third quarter. Management highlighted a return to positive same-venue sales, driven largely by a sharp rebound in traffic from the core 1-2 bay customer segment, which represents most of the revenues. Value-focused initiatives such as weekday discounts and promotional offerings resonated quickly with consumers, leading to high-teens traffic growth and renewed momentum after several softer quarters. This turnaround signaled improving demand elasticity and restored confidence in Topgolf’s growth engine.

Another tailwind came from strong execution in the Golf Equipment segment, where revenues grew despite fewer major product launches. Market conditions remained supportive, with rising rounds played and healthy sell-through trends across key regions. Topgolf Callaway continued to gain share in golf balls and reinforced its brand leadership through top rankings in independent product testing. These results underscored the durability of the equipment business and reassured investors that innovation-led differentiation remains intact even in a competitive launch environment.

Investors also responded positively to improving profitability trends and disciplined cost management. While tariffs weighed on reported earnings, management emphasized ongoing gross margin expansion excluding tariffs, supported by efficiency initiatives and vendor negotiations. Importantly, Topgolf venue-level EBITDA margins held firm even after introducing more aggressive value offerings, suggesting it can stimulate demand without materially eroding unit economics. This balance between growth and margins likely helped reinforce the stock’s recent strength.

Finally, upward revisions to full-year guidance and a stronger balance sheet provided additional support to MODG’s shares. The company raised both revenue and EBITDA outlooks, indicating confidence in sustained traffic trends and cost controls. Liquidity improved meaningfully, net leverage declined and free cash flow generation strengthened following asset divestitures. Combined with management’s reiterated commitment to unlocking shareholder value through a potential Topgolf separation, these factors likely contributed to the market’s willingness to re-rate the stock higher in recent months.

MODG is currently trading at a discount compared with the industry, with a forward 12-month price-to-sales (P/S) ratio of 0.62. Conversely, industry players, such as Acushnet Holdings and American Outdoor, are trading at a P/S ratio of 1.96 and 0.52, respectively.

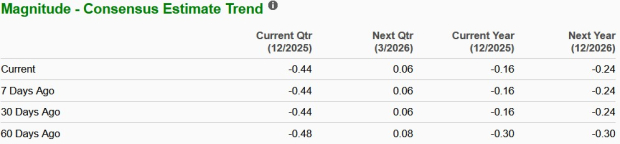

The Zacks Consensus Estimate for MODG’s 2026 loss estimate has narrowed in the past 60 days.

Topgolf Callaway looks attractive for investors as its core Topgolf business is showing a clear demand recovery, with traffic improving on the back of value-focused initiatives that have not pressured profitability. The Golf Equipment segment remains steady, supported by strong brands and ongoing share gains, while cost discipline and a healthier balance sheet are strengthening overall execution. With management signaling confidence in sustained momentum and the stock still trading at a relative discount, MODG offers an appealing risk-reward for investors seeking exposure to a turnaround with improving fundamentals.

MODG currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Jul-23 | |

| Jul-13 | |

| Jun-26 | |

| Jun-25 | |

| Jun-25 | |

| Jun-24 | |

| May-31 | |

| May-07 | |

| May-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite