|

|

|

|

|||||

|

|

|

Great Lakes Dredge & Dock trades at $12.94 per share and has stayed right on track with the overall market, gaining 14.8% over the last six months. At the same time, the S&P 500 has returned 11.5%.

Is there a buying opportunity in Great Lakes Dredge & Dock, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

We're swiping left on Great Lakes Dredge & Dock for now. Here are three reasons why GLDD doesn't excite us and a stock we'd rather own.

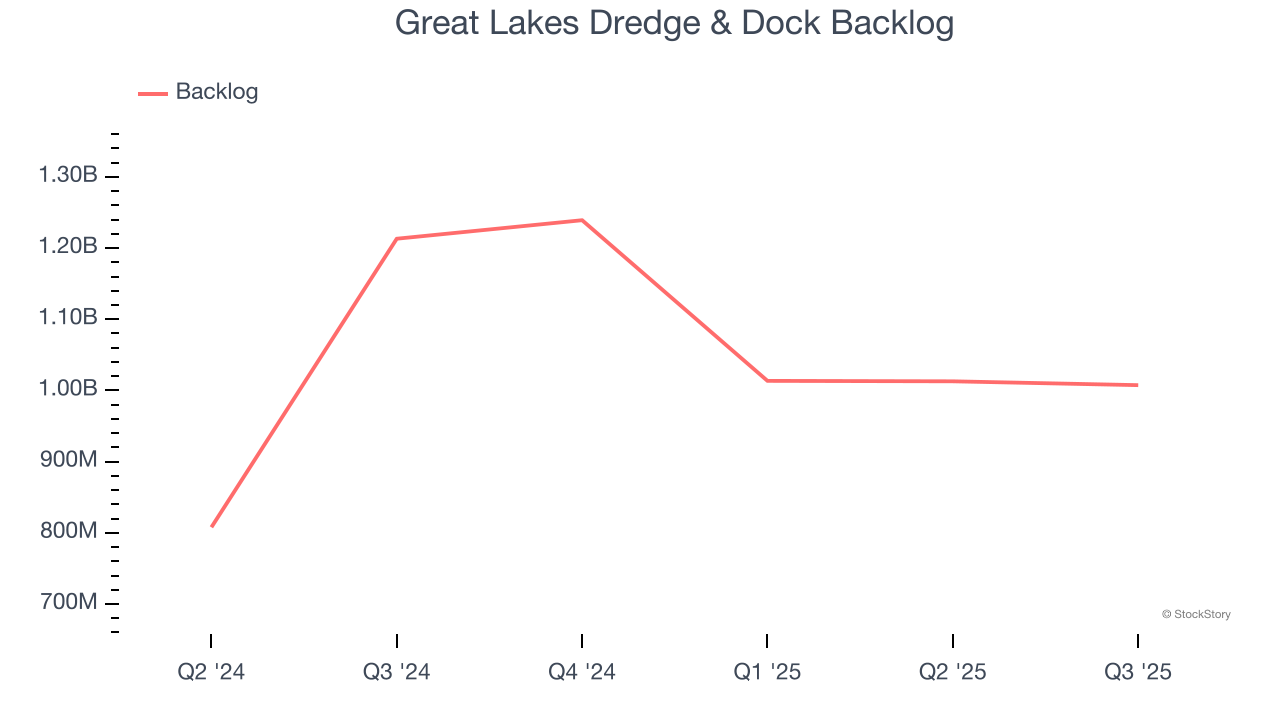

In addition to reported revenue, backlog is a useful data point for analyzing Construction and Maintenance Services companies. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into Great Lakes Dredge & Dock’s future revenue streams.

Great Lakes Dredge & Dock’s backlog came in at $1.01 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 4.2%. This performance was underwhelming and suggests that increasing competition is causing challenges in winning new orders.

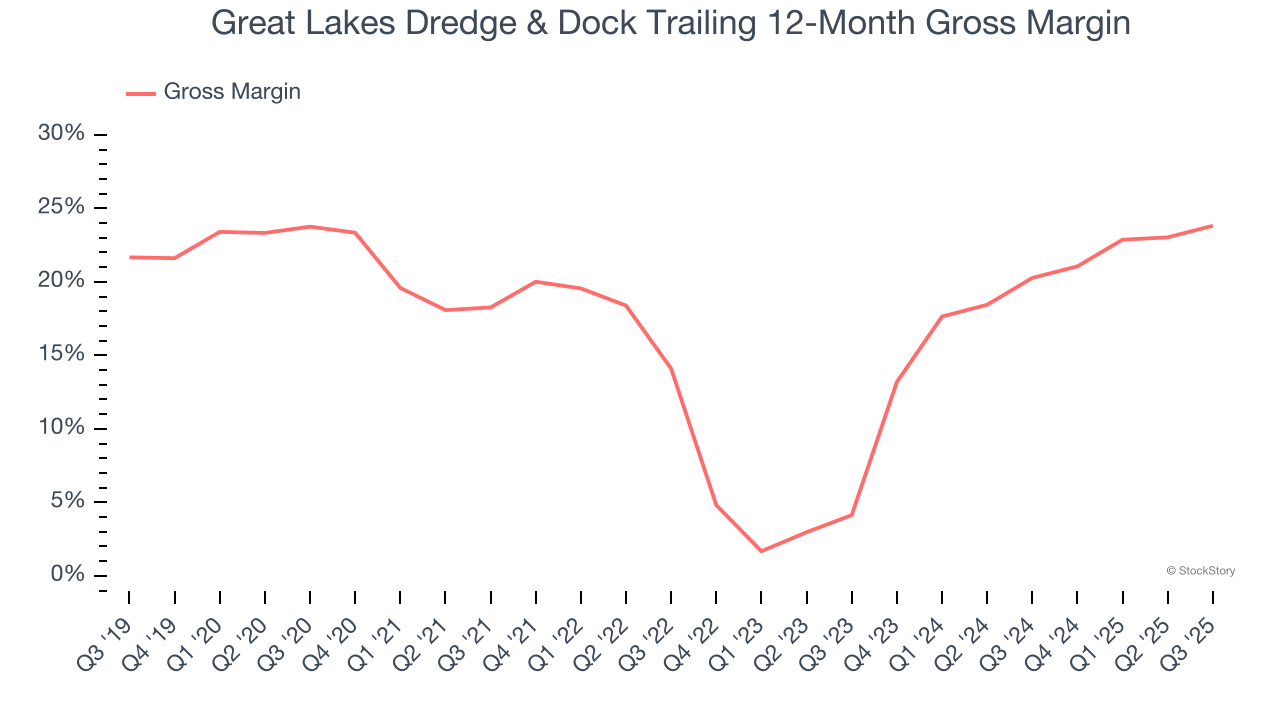

Cost of sales for an industrials business is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics.

Great Lakes Dredge & Dock has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 16.9% gross margin over the last five years. Said differently, Great Lakes Dredge & Dock had to pay a chunky $83.07 to its suppliers for every $100 in revenue.

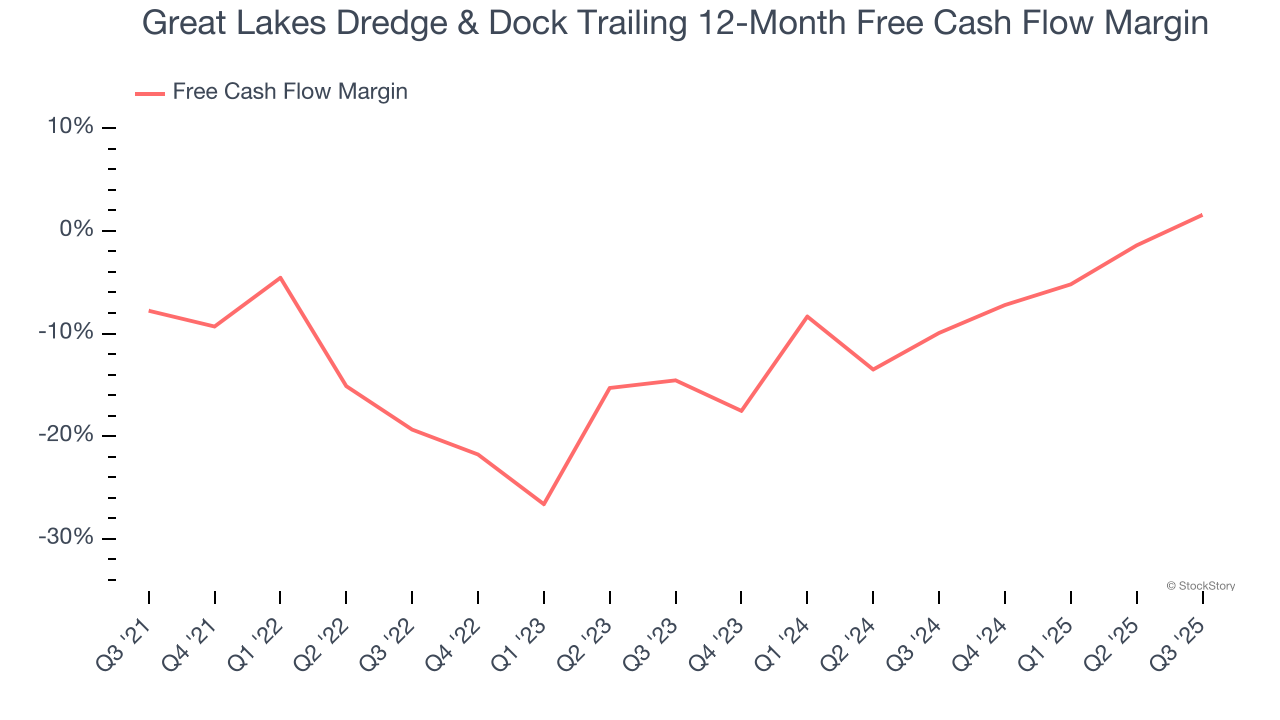

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While Great Lakes Dredge & Dock posted positive free cash flow this quarter, the broader story hasn’t been so clean. Great Lakes Dredge & Dock’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 9.4%, meaning it lit $9.43 of cash on fire for every $100 in revenue.

Great Lakes Dredge & Dock isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 14.2× forward P/E (or $12.94 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at one of our top digital advertising picks.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Apr-01 | |

| Apr-01 | |

| Mar-19 | |

| Mar-18 | |

| Mar-16 | |

| Mar-10 | |

| Mar-10 | |

| Mar-05 | |

| Mar-04 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite