|

|

|

|

|||||

|

|

|

Since July 2025, Jacobs Solutions has been in a holding pattern, posting a small return of 3.4% while floating around $138.76. The stock also fell short of the S&P 500’s 10.5% gain during that period.

Is now the time to buy Jacobs Solutions, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

We're swiping left on Jacobs Solutions for now. Here are three reasons there are better opportunities than J and a stock we'd rather own.

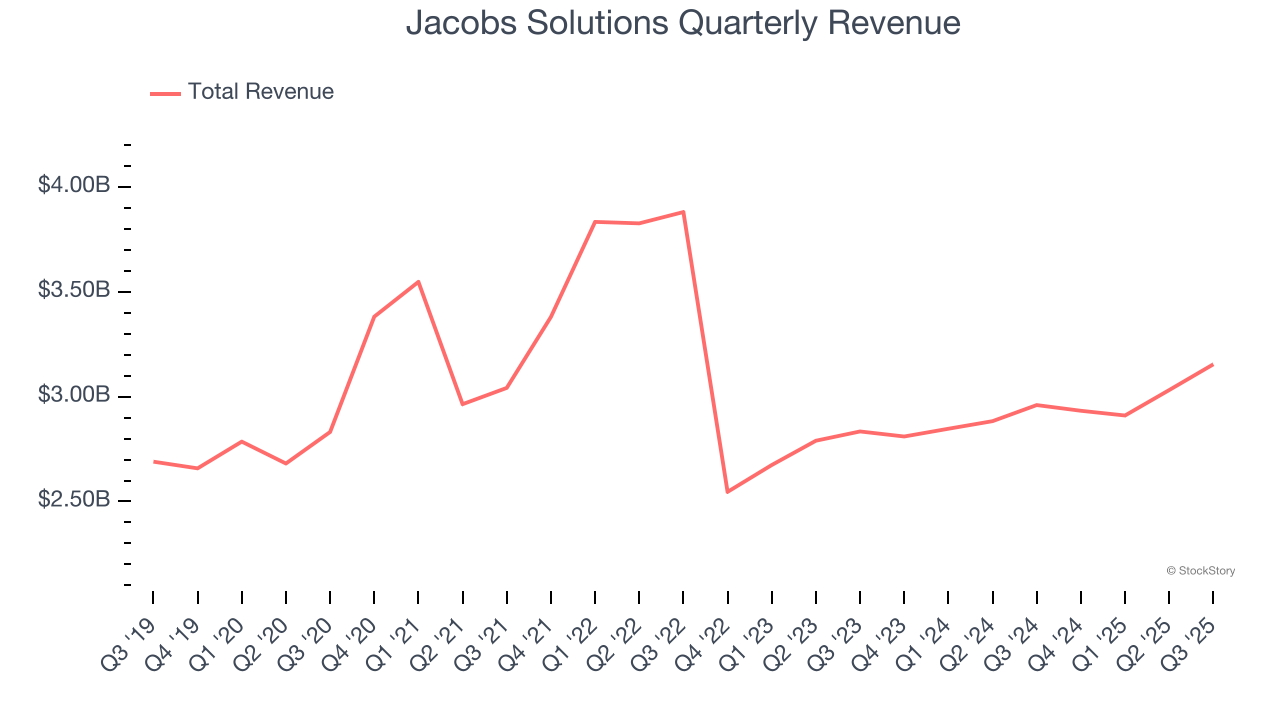

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Jacobs Solutions’s sales grew at a sluggish 1.9% compounded annual growth rate over the last five years. This was below our standards.

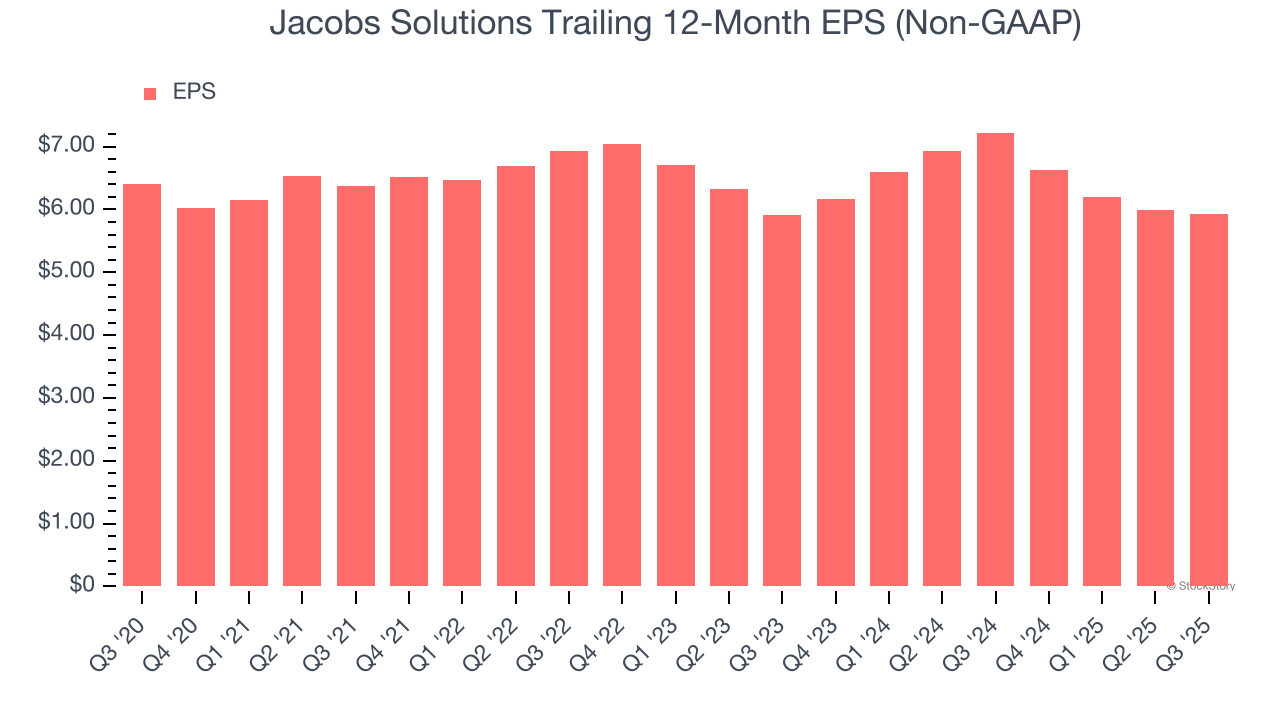

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Jacobs Solutions, its EPS declined by 1.5% annually over the last five years while its revenue grew by 1.9%. This tells us the company became less profitable on a per-share basis as it expanded.

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Jacobs Solutions historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8.1%, somewhat low compared to the best business services companies that consistently pump out 25%+.

Jacobs Solutions isn’t a terrible business, but it doesn’t pass our bar. With its shares trailing the market in recent months, the stock trades at 19.3× forward P/E (or $138.76 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-07 | |

| Jul-02 | |

| Jun-30 | |

| Jun-22 | |

| Jun-20 | |

| Jun-15 | |

| Jun-09 | |

| Jun-04 | |

| Jun-03 | |

| May-26 | |

| May-18 | |

| May-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite