|

|

|

|

|||||

|

|

|

Sterling currently trades at $306.08 and has been a dream stock for shareholders. It’s returned 1,266% since January 2021, blowing past the S&P 500’s 82% gain. The company has also beaten the index over the past six months as its stock price is up 26.8% thanks to its solid quarterly results.

Is now still a good time to buy STRL? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Involved in the construction of a major highway, the Grand Parkway in Houston, TX, Sterling Infrastructure (NASDAQ:STRL) provides civil infrastructure construction.

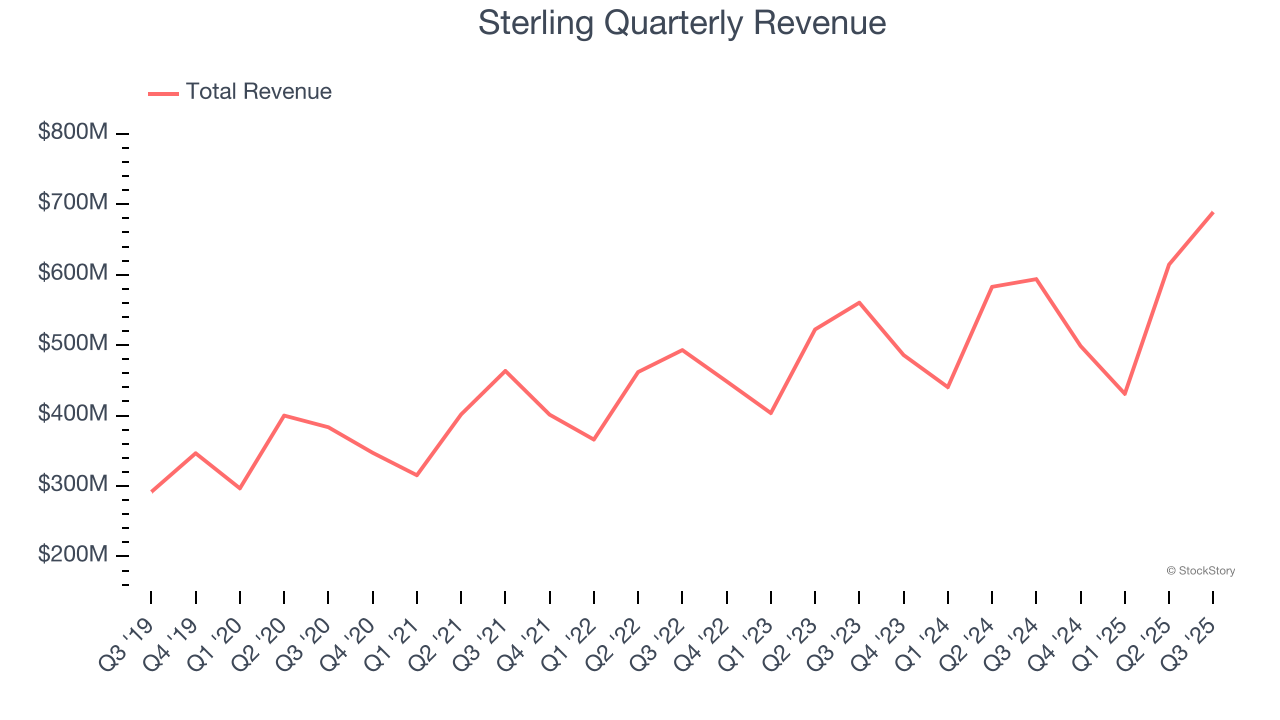

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Sterling’s sales grew at a solid 9.4% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

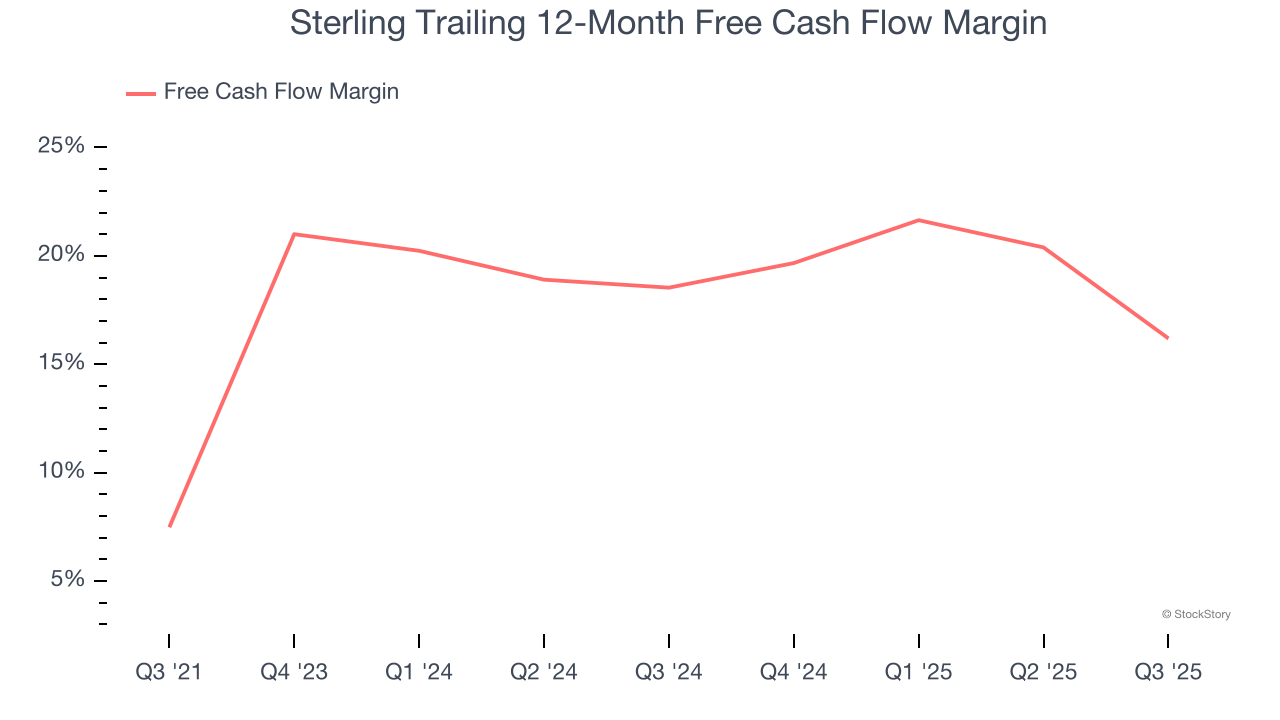

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Sterling’s margin expanded by 8.7 percentage points over the last five years. This is encouraging because it gives the company more optionality. Sterling’s free cash flow margin for the trailing 12 months was 16.2%.

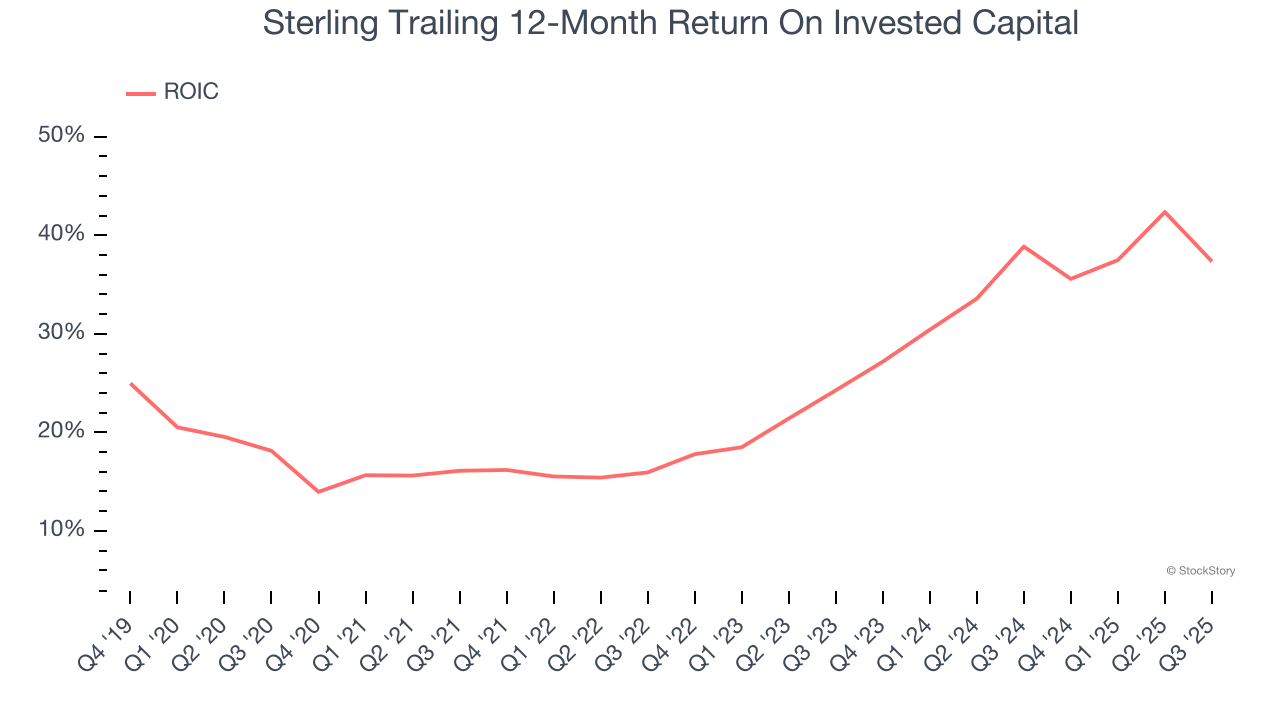

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Sterling’s ROIC has increased significantly over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

These are just a few reasons why we think Sterling is an elite industrials company, and with its shares outperforming the market lately, the stock trades at 26× forward P/E (or $306.08 per share). Is now a good time to buy? See for yourself in our in-depth research report, it’s free.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Apr-15 |

Sterling, IBD's Stock Of The Day, Soars 370% In One Year. It Could Climb Even More.

STRL

Investor's Business Daily

|

| Apr-14 |

Dow Jones Futures: What To Do As Nasdaq, Nvidia Win Streaks Hit 10 Days; ASML, Bank Of America On Tap

STRL

Investor's Business Daily

|

| Apr-08 | |

| Mar-25 | |

| Mar-23 |

Wall Street Raises Outlook For Three AI Names And This Medical Stock

STRL +5.21%

Investor's Business Daily

|

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite