|

|

|

|

|||||

|

|

|

What a time it’s been for IQVIA. In the past six months alone, the company’s stock price has increased by a massive 51.4%, reaching $242.50 per share. This performance may have investors wondering how to approach the situation.

Is now the time to buy IQVIA, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Despite the momentum, we don't have much confidence in IQVIA. Here are three reasons why IQV doesn't excite us and a stock we'd rather own.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a stretched historical view may miss recent innovations or disruptive industry trends. IQVIA’s recent performance shows its demand has slowed as its annualized revenue growth of 3.5% over the last two years was below its five-year trend.

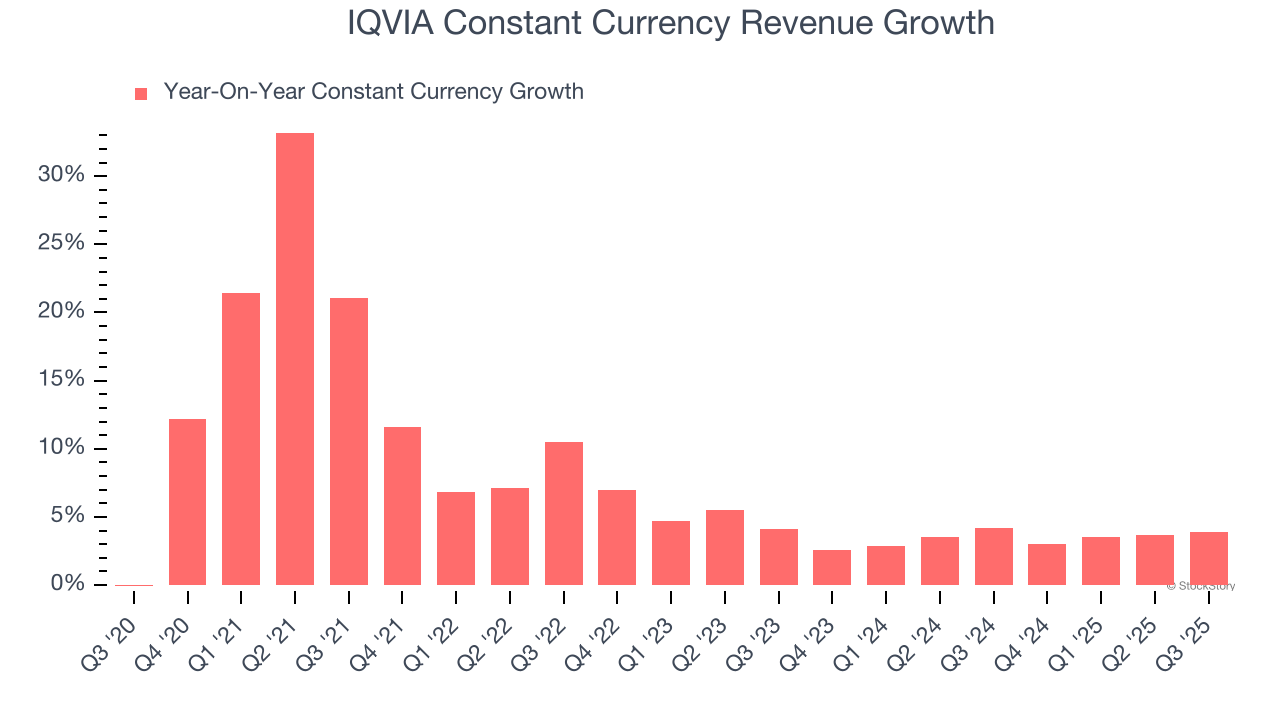

In addition to reported revenue, constant currency revenue is a useful data point for analyzing Drug Development Inputs & Services companies. This metric excludes currency movements, which are outside of IQVIA’s control and are not indicative of underlying demand.

Over the last two years, IQVIA’s constant currency revenue averaged 3.4% year-on-year growth. This performance slightly lagged the sector and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

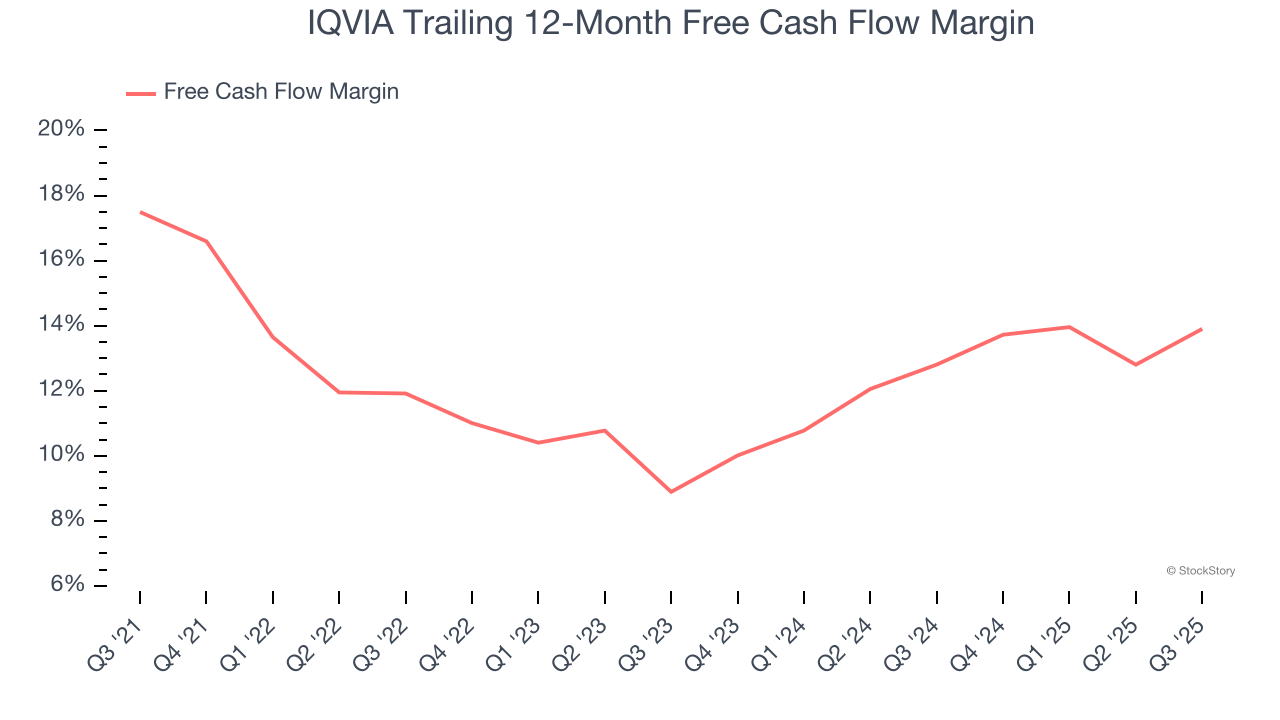

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, IQVIA’s margin dropped by 3.6 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. IQVIA’s free cash flow margin for the trailing 12 months was 13.9%.

IQVIA isn’t a terrible business, but it doesn’t pass our bar. After the recent rally, the stock trades at 19.3× forward P/E (or $242.50 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at the Amazon and PayPal of Latin America.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-16 | |

| Jul-08 | |

| Jun-24 | |

| Jun-17 | |

| Jun-17 | |

| Jun-15 | |

| Jun-04 | |

| Jun-04 | |

| Jun-03 | |

| May-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite