|

|

|

|

|||||

|

|

|

AI is a fast-growing market whose outlook has yet to be fully reflected in its stock prices. While it's hard to say for certain which AI infrastructure, model builder, or application will stand the test of time, it is certain that AI and the cloud are here to stay.

Many organizations use multiple cloud platforms (like AWS, Microsoft Azure, or Google Cloud), which can add complexity because each has different tools and management systems. Cross-cloud operators help bridge these environments so data, applications, and workflows operate more like a single, unified system. As multi-cloud adoption expands, these companies can be attractive long-term investments.

Let's take a look at five leading cross-cloud operators and where their stock prices may be headed in 2026.

Most cloud hyperscalers operate as cross-cloud providers to some degree. However, none provides the depth of cross-cloud coverage that Oracle (NYSE: ORCL) does.

Its data, database, and AI-enabled services are embedded throughout the hyperscale environment, including most private clouds, and expanding in reach quarterly.

Among the critical highlights from late 2025 results are quadruple-digit gains in hyperscaler-drien business, which attest to that. Looking forward, client wins and a swelling RPO point to a high-teens revenue growth this year and acceleration over the subsequent two to three years.

Oracle’s analyst trends are bullish, pointing to a robust 55% upside in 2026.

Not only has coverage increased, but the sentiment rating strengthened, and the price target revisions led to the high end of the range.

The consensus forecasts 55% upside, but the high-end adds to it, bringing the potential stock price gain in 2026 to approximately 100% relative to the critical support target. It aligns with prior highs and provides support in early January.

Salesforce (NYSE: CRM) is a cross-cloud operator because its system unifies sales, marketing, and service in a cloud-based, AI-enabled platform.

Highlights from 2025 include traction in growth drivers such as Agentforce, the application-end of its AI offerings, and a forecast for growth to begin accelerating into the double-digit range.

Agentforce enables businesses to monetize their data by developing AI agents for specific needs.

Analyst trends shifted significantly in 2025 and are tracking bullish as 2026 gets underway.

The shift is from negative to positive revisions, affirming the Moderate Buy rating and consensus forecast for 25% upside.

Assuming this trend continues. Salesforce will likely move into the high-end of its analysts' target range before year’s end.

Snowflake (NYSE: SNOW) is a cross-cloud operator because its cloud-agnostic position enables seamless integration of data and workloads across cloud environments and regions.

Among its strengths is the cloud-native architecture of its database, which effectively decouples storage from compute, enabling independent scaling. Highlights from 2025 include a successful CEO transition, reinvigorated growth, and accelerating RPO, pointing to strength in 2026.

Analyst trends are bullish for Snowflake. The 2025 trends, continued in early January, include increased coverage, firming sentiment, and an uptrend in the consensus price target, pointing to a 25% to 50% upside by year’s end.

Institutional trends also align with a rising stock price, as institutions bought at an aggressive $3-to-$1 pace in 2025 and extended that trend into the first week of 2026.

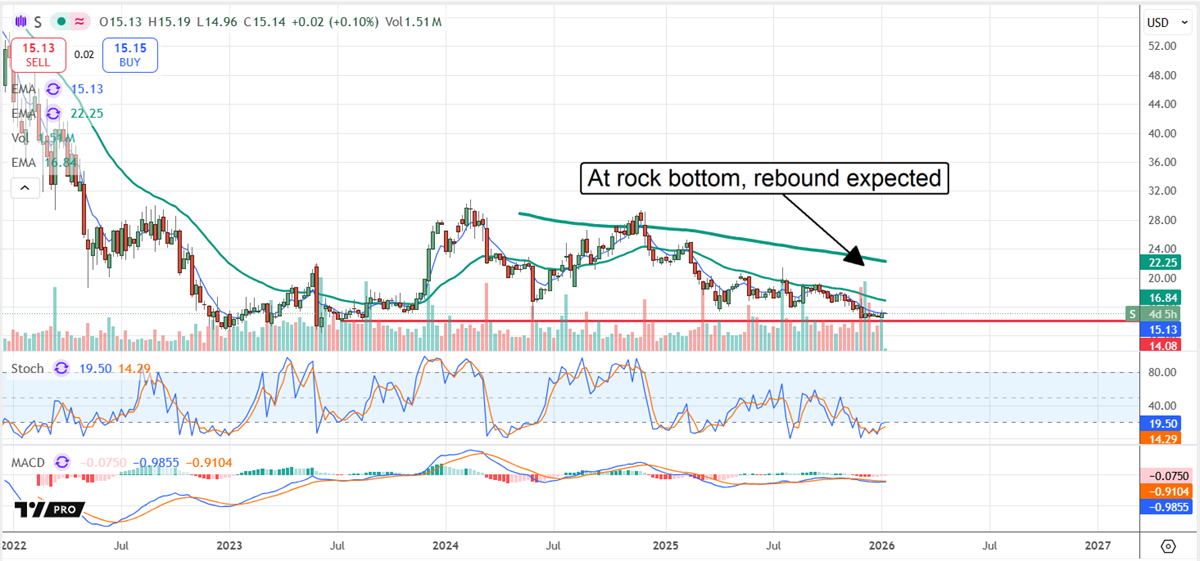

SentinelOne (NYSE: S) is a leading cybersecurity provider enabling seamless, cross-cloud security with a unified platform.

It secures public and private clouds, integrates with all major hyperscalers, including Oracle, covering endpoints and IDs while proactively seeking and mitigating threats.

Highlights from 2025 include sustained, high-level growth above 20%, outperformance, and solid guidance.

SentinelOne’s analyst trends align with those of its cross-cloud peers, including increased coverage, firm sentiment, a Moderate Buy rating, and an uptrend in the price target. The consensus for SentinelOne is a 50% upside this year, while trends suggest potential for as much as 85% by year’s end.

UiPath (NYSE: PATH) was ahead of its time with automated, agentic AI, but starting to gain traction today.

Its business-enhancing tools aid businesses from the loading dock to distribution, increasing efficiency and profitability.

Highlights from 2025 include accelerating growth, improving profitability, and strengthening forecasts underpinned by client growth and penetration gains.

Analysts are less bullish on this stock but are warming up in early 2026. The consensus rating is Hold, and the price target assumes fair value, but the company expects significant growth in the coming year and is likely to surprise investors.

UiPath is a critical cross-cloud operator because its platform enables complex workflows across business segments and cloud instances.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

The article "5 AI Stocks Positioned to Win, No Matter What" first appeared on MarketBeat.

| 1 hour | |

| 9 hours | |

| 11 hours | |

| 13 hours | |

| 14 hours | |

| 14 hours | |

| 14 hours | |

| 14 hours | |

| 15 hours | |

| 16 hours | |

| 21 hours | |

| 21 hours | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite