|

|

|

|

|||||

|

|

|

Over the past six months, Armstrong World has been a great trade, beating the S&P 500 by 7.2%. Its stock price has climbed to $198.71, representing a healthy 18.3% increase. This performance may have investors wondering how to approach the situation.

Is now still a good time to buy AWI? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Started as a two-man shop dating back to the 1860s, Armstrong (NYSE:AWI) provides ceiling and wall products to commercial and residential spaces.

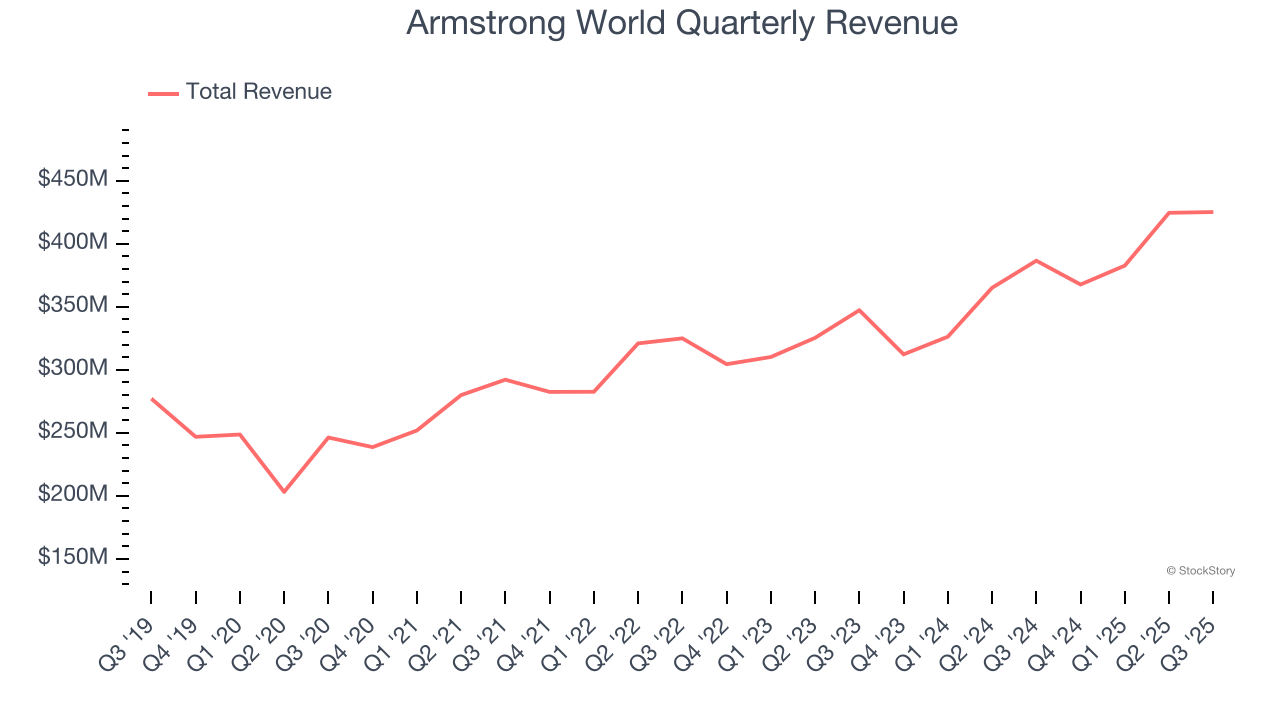

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Armstrong World’s 11.1% annualized revenue growth over the last five years was impressive. Its growth surpassed the average industrials company and shows its offerings resonate with customers.

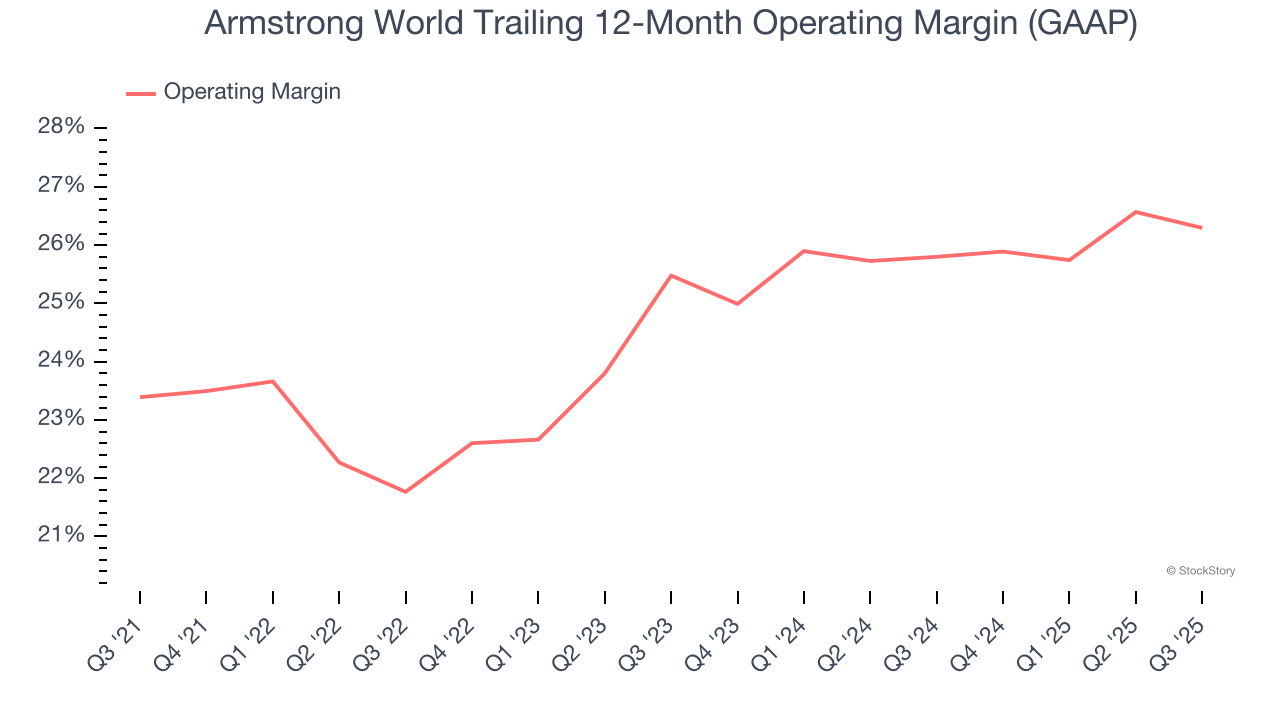

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Armstrong World has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 24.7%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

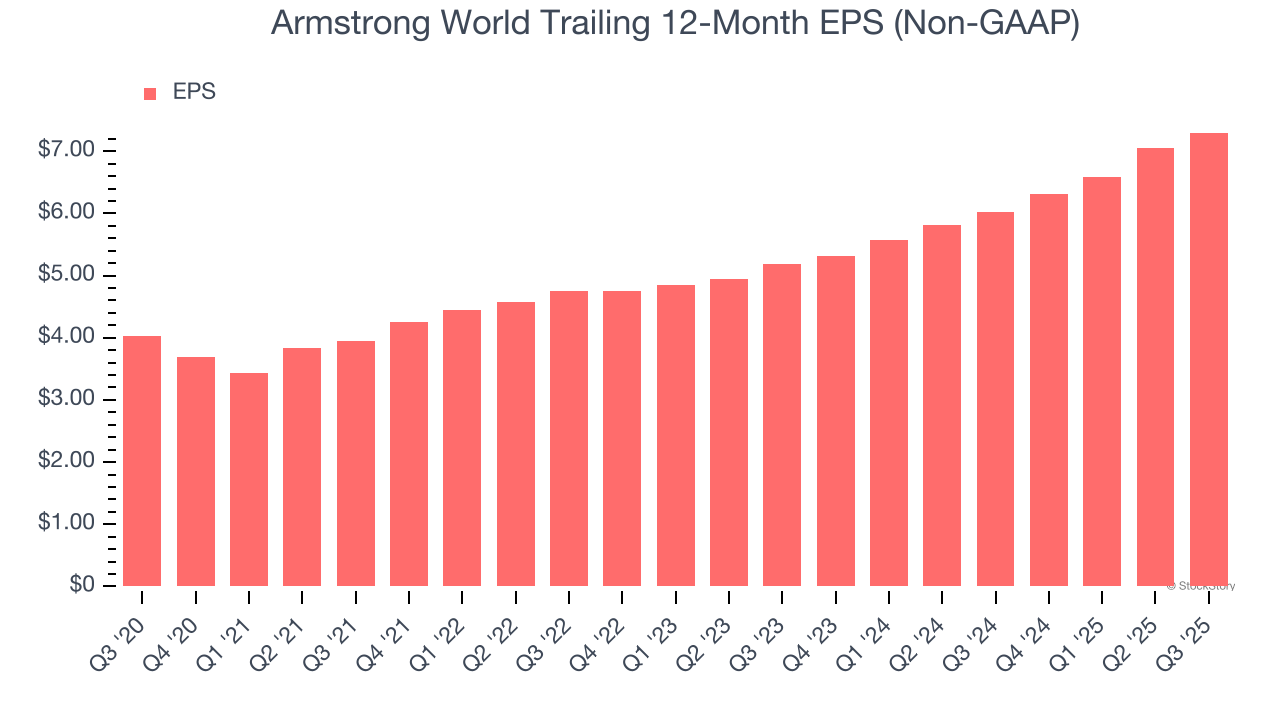

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Armstrong World’s remarkable 12.6% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

These are just a few reasons why we think Armstrong World is a high-quality business, and with its shares topping the market in recent months, the stock trades at 24.5× forward P/E (or $198.71 per share). Is now a good time to initiate a position? See for yourself in our full research report, it’s free.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-21 | |

| Jul-08 | |

| Jul-07 | |

| May-27 | |

| May-11 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-24 | |

| Apr-07 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite