|

|

|

|

|||||

|

|

|

Xylem trades at $140.11 and has moved in lockstep with the market. Its shares have returned 7% over the last six months while the S&P 500 has gained 11.3%.

Is XYL a buy right now? Find out in our full research report, it’s free.

Formed through a spinoff, Xylem (NYSE:XYL) manufactures and services engineered products across a wide variety of applications primarily in the water sector.

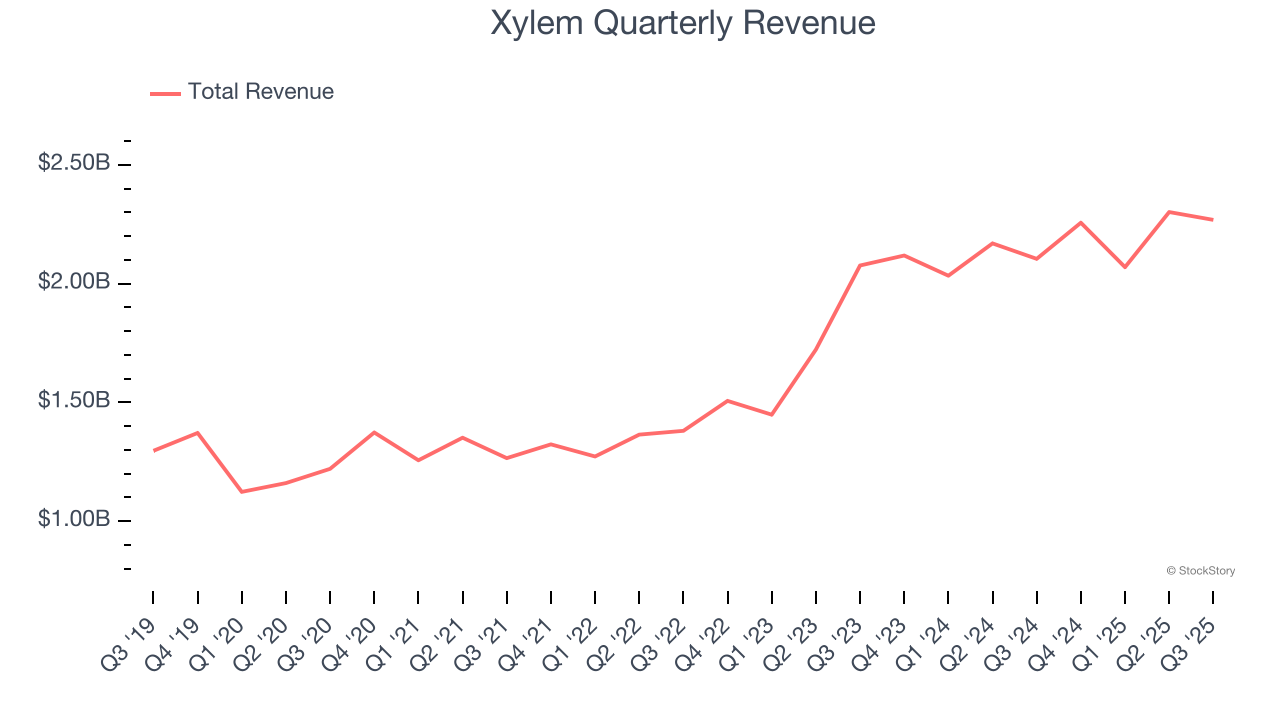

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Xylem grew its sales at an excellent 12.8% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

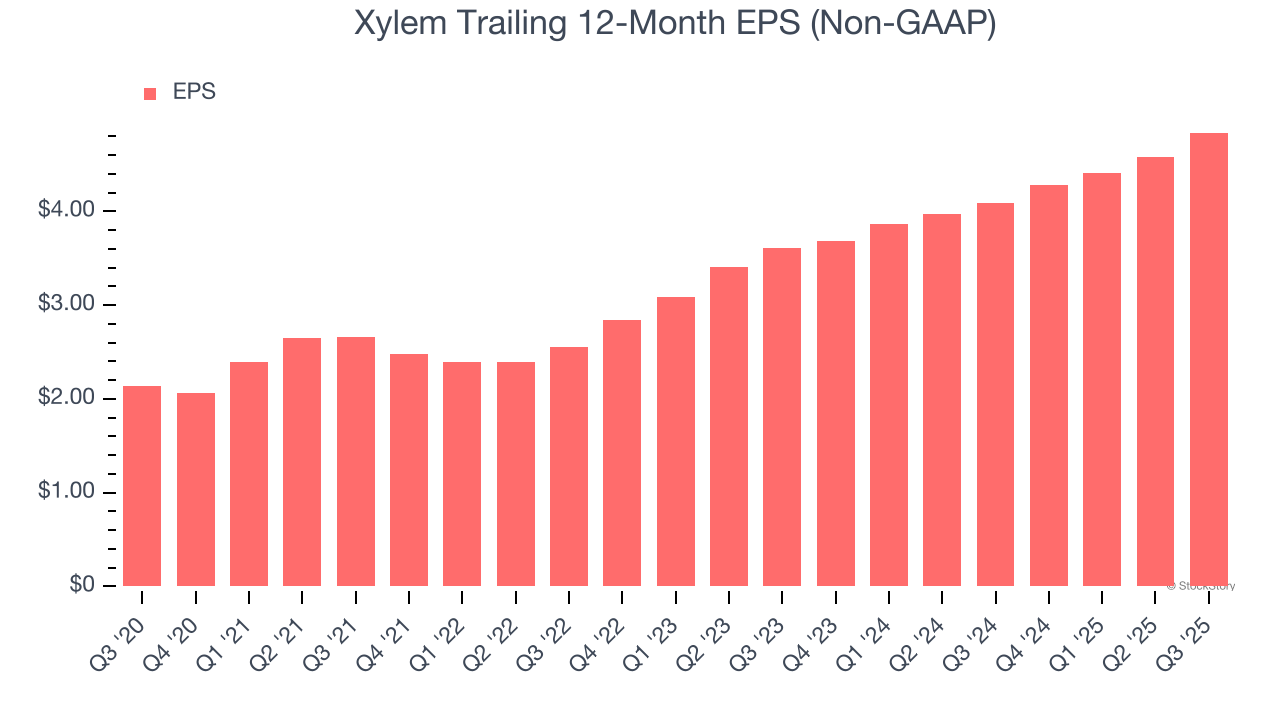

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Xylem’s EPS grew at an astounding 17.7% compounded annual growth rate over the last five years, higher than its 12.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

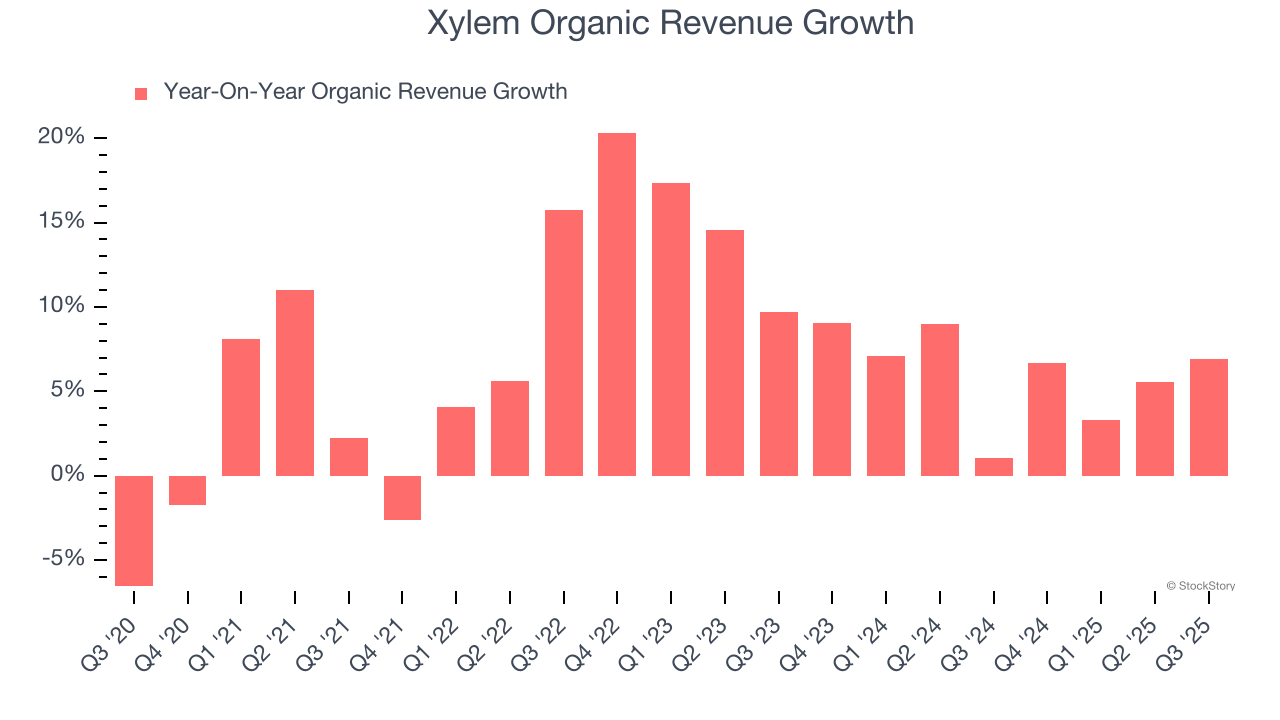

Investors interested in Water Infrastructure companies should track organic revenue in addition to reported revenue. This metric gives visibility into Xylem’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Xylem’s organic revenue averaged 6.1% year-on-year growth. This performance slightly lagged the sector and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Xylem’s positive characteristics outweigh the negatives, but at $140.11 per share (or 25.6× forward P/E), is now the time to initiate a position? See for yourself in our full research report, it’s free.

Check out the high-quality names we’ve flagged in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-15 | |

| Jul-02 | |

| Jun-30 | |

| May-26 | |

| May-15 | |

| May-12 | |

| Apr-29 | |

| Apr-28 | |

| Apr-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite