|

|

|

|

|||||

|

|

|

Western Digital Corporation’s WDC deepening collaborations with hyperscaler customers are becoming a strategic competitive moat as AI-driven data growth accelerates.

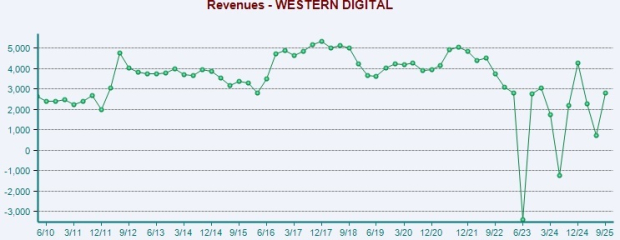

WDC is one of the leading providers of mass capacity storage solutions. As multimodal large language models and agentic AI scale across industries, hyperscalers are facing an unprecedented growth in data generated, resulting in strong demand for high-capacity, cost-efficient storage solutions.

A key indicator of this strengthening competitive moat is the growing visibility that Western Digital now has into customer demand. Customers are transitioning to higher-capacity drives, with shipments of its latest ePMR products offering up to 26TB CMR and 32TB UltraSMR, exceeding 2.2 million units in the September quarter. The reliability, scalability and TCO benefits of its ePMR and UltraSMR technologies remain key to success in the data center market.

Western Digital plans to build on this with its next-generation HAMR drives. All top seven customers have issued purchase orders through the first half of 2026, with five extending through all of 2026 and one major hyperscale customer securing supply for all of 2027.

It is making strong progress on HAMR development. It remains on track to begin qualification with one hyperscale customer in the first half of 2026, with the potential to expand to up to three customers by year-end. This progress positions the company for volume production ramp-up in the first half of 2027.

Meanwhile, WDC will start qualification for its next-gen ePMR drives by early 2026. For the second quarter of fiscal 2026, management anticipates ongoing revenue growth, supported by strong data center demand. WDC is set to report second-quarter fiscal 2026 results on Jan. 29, 2026. Non-GAAP revenues are expected to be $2.9 billion (+/- $100 million), up 20% year over year.

However, the company faces intense competition from the likes of Seagate Technology Holdings Plc STX and other flash-based alternatives.

Seagate, one of Western Digital’s closest rivals in the HDD space, is gaining from strong industry tailwinds. The company shipped more than 1 million Mozaic drives during the September quarter. Since its HAMR-based Mozaic drives are the industry’s only products offering 3 terabytes per disk, cloud customers are lining up for them. Seagate now has five global CSPs qualified on its Mozaic 3+ terabyte-per-disk products, offering up to 36TB per drive, and remains on track to qualify the remaining three CSPs by the first half of 2026.

The Mozaic products are performing strongly in production, with Seagate on track to reach 50% exabyte crossover on nearline HAMR drives in the second half of 2026. The company has also begun qualifying with a second major CSP on the Mozaic 4+ terabyte-per-disk platform, offering up to 44TB per drive, with volume ramp expected in early 2026. Moreover, management is steadily advancing 5TB per disk technology, aiming for market launch in early 2028. Lab demonstrations of 10TB per disk are also expected around that time. Ongoing innovation in media and photonics is key to this progress.

Among flash-based alternatives, Pure Storage PSTG is one of the prominent players in the data storage space. Increasing adoption of flash storage, advantages of all-flash arrays in data centers, strong partner base and growth prospects in emerging data-driven markets are key positives.

Hyperscaler partnerships are becoming an increasingly important component of PSTG’s growth strategy. Pure Storage noted that year-to-date hyperscale shipments through the third quarter of fiscal 2026 already exceeded its original fiscal year target of 1-2 exabytes, with additional shipments expected in the fiscal fourth quarter. Pure Storage noted that hyperscaler shipments are supporting higher product gross margins and were a factor in the upward revision to fiscal 2026 operating income guidance.

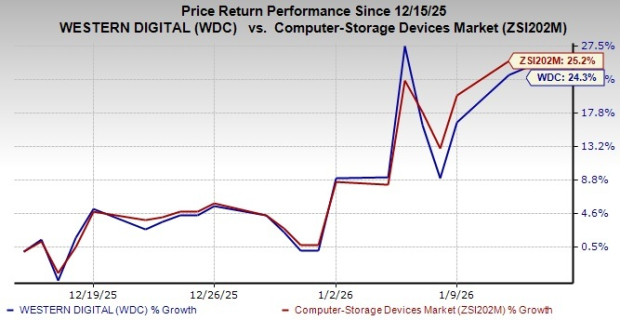

In the past month, shares of WDC have increased 24.3% compared with the Zacks Computer-Storage Devices industry’s growth of 25.2%.

In terms of forward price/earnings, WDC’s shares are trading at 23.25X, higher than the industry’s 21.7X.

The Zacks Consensus Estimate for WDC’s earnings for fiscal 2026 has been marginally revised upwards over the past 60 days.

Currently, Western Digital sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 9 hours | |

| Aug-10 | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite