|

|

|

|

|||||

|

|

|

Shares of Apellis Pharmaceuticals APLS have crashed 22.6% in the past week. The massive stock price decline was observed after the company reported preliminary fourth-quarter U.S. net product revenues earlier this week at the J.P. Morgan Healthcare Conference, which likely failed to impress investors.

Apellis reported preliminary U.S. net product revenues of $190 million in the fourth quarter of 2025. The company’s product revenues comprise sales of its two marketed drugs — Empaveli (pegcetacoplan) and Syfovre.

Syfovre was approved for treating geographic atrophy (GA) secondary to age-related macular degeneration by the FDA in 2023. The drug’s sales generated preliminary U.S. net product revenues of approximately $155 million in the fourth quarter of 2025, down 8% year over year. The figure marginally beat the Zacks Consensus Estimate of $154 million and matched our model estimate.

Apellis delivered more than 89,000 commercial vials and nearly 13,000 samples of Syfovre to doctors in the fourth quarter. Despite being a market leader in GA, enjoying more than 60% share of the overall market, revenues generated from Syfovre sales declined year over year, which disappointed the investors.

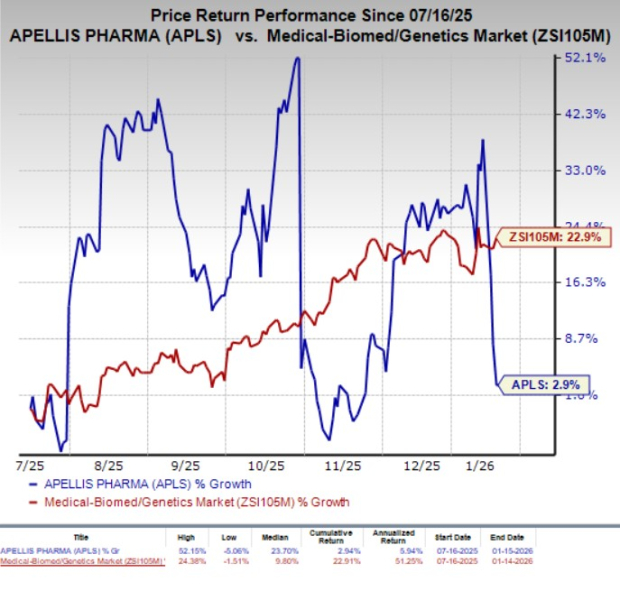

In the past six months, shares of Apellis have gained 2.9% compared with the industry’s 22.9% growth.

Empaveli is approved in the United States for the treatment of paroxysmal nocturnal hemoglobinuria. The drug’s sales generated preliminary U.S. net product revenues of approximately $35 million in the fourth quarter of 2025, up 50% year over year. The figure beat the Zacks Consensus Estimate of $28 million as well as our model estimate of $32 million.

Please note that Apellis and Sobi’s regulatory filing seeking the label expansion of Empaveli to treat C3 glomerulopathy and primary immune complex glomerulonephritis (C3G and IC-MPGN) was approved by the FDA as the first treatment for this indication in patients aged 12 years and older in July 2025.

Apellis reported that 267 cumulative patient start forms have been received as of Dec. 31, 2025, which represents more than 5% penetration into the U.S. patient market in five months post-launch. The fourth quarter of 2025 represents the first full quarter of sales following the drug’s launch in the United States for this new indication. The investors were likely expecting higher sales of the drug, which also contributed to the stock price decline.

For full-year 2025, Apellis announced preliminary U.S. net product revenues of approximately $689 million, down 3% year over year.

At the J.P. Morgan Healthcare Conference, Apellis also provided updates regarding its pipeline. A regulatory filing seeking the label expansion of Empaveli (marketed as Aspaveli in the EU) to treat C3G and IC-MPGN is also currently under review in the EU.

Apellis also stated that it has initiated two pivotal phase III studies of Empaveli in focal segmental glomerulosclerosis (FSGS) and delayed graft function (DGF) in the fourth quarter of 2025. Both FSGS and DGF are rare kidney diseases in which the complement pathway plays a significant role, and there are no approved therapies.

The company’s mid-stage multi-dose study of siRNA candidate APL-3007 in combination with Syfovre is currently ongoing, aimed at comprehensively blocking complement activity in the retina and choroid. Top-line data from this study is expected in 2027.

As of Dec. 31, 2025, Apellis had cash, cash equivalents and marketable securities worth $466 million compared with $479.2 million as of Sept. 30, 2025. APLS expects its cash balance, combined with cash anticipated from sales of marketed products, to be enough to fund its operations to profitability.

Apellis Pharmaceuticals, Inc. price-consensus-chart | Apellis Pharmaceuticals, Inc. Quote

Apellis currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the biotech sector are Amicus Therapeutics FOLD, Alkermes ALKS and Krystal Biotech KRYS, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Over the past 60 days, estimates for Amicus Therapeutics’ 2026 EPS have decreased from 67 cents to 65 cents. Shares of FOLD have surged 136.9% over the past six months.

Amicus Therapeutics’ earnings beat estimates in one of the trailing four quarters, missing the mark on the other three occasions, delivering an average negative surprise of 20.21%.

Over the past 60 days, 2026 EPS estimates for Alkermes have increased from $1.54 to $1.80. Shares of ALKS have gained 4.9% over the past six months.

Alkermes’ earnings beat estimates in three of the trailing four quarters, missing on the remaining occasion, with the average surprise being 4.58%.

Over the past 60 days, estimates for Krystal Biotech’s EPS for 2026 have risen to $8.49 from $8.34. KRYS stock has rallied 94.4% over the past six months.

Krystal Biotech’s earnings beat estimates in three of the trailing four quarters and missed in the remaining quarter, with the average surprise being 40.43%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-20 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 | |

| Jun-29 | |

| Jun-29 | |

| Jun-26 | |

| Jun-17 | |

| Jun-15 | |

| Jun-13 |

Viking, Bloom Energy Lead Five Stocks Making Bullish Moves As Market Rebounds

KRYS

Investor's Business Daily

|

| Jun-12 |

Dow Jones Futures Rise, Oil Skids On Iran Deal Hopes; SpaceX IPO Indicated Higher

KRYS

Investor's Business Daily

|

| Jun-12 | |

| Jun-04 | |

| Jun-03 | |

| May-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite