|

|

|

|

|||||

|

|

|

Carter’s, Inc.’s CRI overall growth continues to be constrained by weakness in U.S. Wholesale, where declines, particularly related to Amazon’s Simple Joys brand, have largely offset gains achieved in U.S. Retail and International markets. The company’s net sales declined marginally by 0.1% to $757.8 million in the third quarter of 2025 compared with the prior-year quarter. While U.S. Retail and International delivered growth, U.S. Wholesale fell by a similar dollar amount, resulting in a net neutral impact at the consolidated level.

Performance in the third quarter reflected divergent trends across operating segments. Approximately $15 million in incremental sales from U.S. Retail and International operations was offset by a comparable year-over-year decline in U.S. Wholesale revenue. Consequently, adjusted operating income declined $40 million year over year. The reduction in profitability was driven almost equally by weaker results in both U.S. Retail and U.S. Wholesale, underscoring balanced pressure across these segments despite strength elsewhere.

U.S. Wholesale sales declined compared with last year, primarily due to softer performance from the Simple Joys brand within the exclusive brands portfolio. Demand for Simple Joys on Amazon has moderated throughout the course of the year. While the brand experienced rapid growth following its launch in 2017, supported by Amazon’s positioning of Simple Joys as a private-label offering in children’s apparel, recent shifts in Amazon’s brand management strategy have intensified pressure on this business.

The company is actively developing the framework needed to better align with Amazon’s operating model across its entire brand portfolio. This approach is expected to create a more durable and meaningful long-term business on Amazon beyond the Simple Joys brand, leveraging the broader Carter’s brands. Looking ahead, management expects U.S. Wholesale sales to decline in the low-single-digits in the fourth quarter, largely reflecting continued near-term softness in demand for Simple Joys. In the same quarter, sales across the remainder of the U.S. Wholesale portfolio are expected to increase, helping to partially mitigate the overall decline.

Carter’s shares have gained 20.8% in the past six months against the industry’s decline of 8.7%. CRI presently carries a Zacks Rank #3 (Hold).

From a valuation standpoint, CRI trades at a forward price-to-earnings ratio of 17.04X, lower than the industry’s average 28.16X.

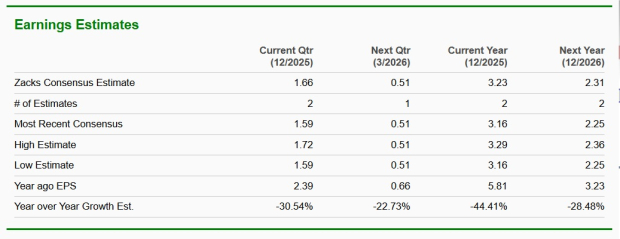

The Zacks Consensus Estimate for CRI’s current and next year earnings implies a year-over-year decline of 44.4% and 28.5%.

Some better-ranked stocks have been discussed below:

Vince Holding Corp. VNCE provides luxury apparel and accessories in the United States and internationally. It operates through Vince Wholesale and Vince Direct-to-Consumer segments. At present, the company sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for VNCE’s current fiscal-year sales and earnings implies growth of 2% and 26.3%, respectively, from the year-ago figures. VNCE has delivered a trailing four-quarter earnings surprise of 229.6%, on average.

Advantage Solutions, Inc. ADV, provides business solutions to the consumer-packaged goods companies and retailers in North America, Asia Pacific, and Europe. At present, Advantage Solutions carries a Zacks Rank of 2 (Buy).

The Zacks Consensus Estimate for Advantage Solutions’ current fiscal-year sales implies a decline of 2.2%, and the same for earnings implies growth of 107.1% from the year-ago figures. ADV has delivered a trailing four-quarter negative earnings surprise of 128.1%, on average.

Guess?, Inc. GES designs, markets, distributes, and licenses lifestyle collections of apparel and accessories for men, women, and children. At present, the company holds a Zacks Rank of 2.

The Zacks Consensus Estimate for GES’s current fiscal-year sales implies growth of 8%, and the same for current fiscal-year earnings implies a decline of 13.8% from the year-ago figures. GES has delivered a trailing four-quarter earnings surprise of 45%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-29 | |

| Jul-27 | |

| Jul-22 | |

| Jul-08 | |

| Jun-26 | |

| Jun-25 | |

| Jun-17 | |

| Jun-17 | |

| Jun-17 | |

| Jun-17 | |

| Jun-16 | |

| Jun-16 | |

| Jun-16 | |

| Jun-16 | |

| Jun-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite