|

|

|

|

|||||

|

|

|

Hollister has become a meaningful earnings driver for Abercrombie & Fitch Co. ANF rather than a volatility risk. In third-quarter fiscal 2025, Hollister delivered 16% net sales growth, with 15% comparable sales growth, extending its streak to the tenth consecutive quarter of growth. This performance materially outpaced the Abercrombie brand and provided critical top-line support to the consolidated business.

The quality of Hollister’s growth is essential for fundamentals. Management emphasized that gains were balanced across men’s and women’s and spread across categories, suggesting broad-based demand rather than reliance on a single trend. Growth was supported by rising traffic, expanding customer files and improved cross-channel engagement, reinforcing the sustainability of revenue momentum. At the same time, disciplined inventory management under the Read & React model enabled Hollister to improve average unit retail through lower promotions, supporting gross margin resilience in an otherwise promotional apparel environment.

Strategic investments further strengthen Hollister’s fundamental outlook. Marketing collaborations tied to collegiate sports and pop-culture brands have enhanced customer acquisition and brand relevance, while physical retail expansion, 25 new stores and more than 35 refreshes planned, signal management’s confidence in long-term demand. These initiatives are being funded from a position of balance-sheet strength, as Abercrombie maintains ample liquidity and continues aggressive share repurchases.

Risks remain, including tougher year-over-year comparisons and fashion sensitivity inherent in teen apparel. However, given Hollister’s consistent revenue growth, margin-supportive execution and growing strategic weight within the portfolio, the brand currently represents a fundamental catalyst to earnings stability and cash flow generation, rather than a drag on Abercrombie’s results.

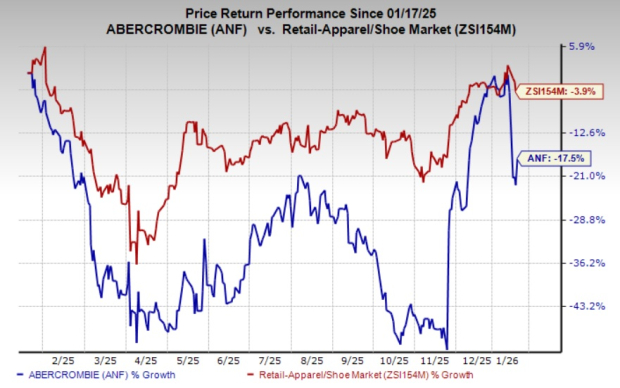

Abercrombie’s shares have lost 17.5% in the past year compared with the industry’s 3.9% decline.

From a valuation standpoint, ANF trades at a forward price-to-earnings ratio of 10.88X compared with the industry’s average of 16.32X.

The Zacks Consensus Estimate for ANF’s fiscal 2025 EPS indicates a year-over-year decline of 8.4%, while that for fiscal 2026 EPS suggests growth of 4.3%. The company’s EPS estimates for fiscal 2025 and 2026 have been northbound in the past seven days. Abercrombie currently carries a Zacks Rank #3 (Hold).

We have highlighted three better-ranked stocks from the Retail-Wholesale industry, namely American Eagle Outfitters Inc. AEO, Boot Barn Holdings Inc. BOOT and The Gap Inc. GAP.

American Eagle is a specialty retailer of casual apparel, accessories and footwear for men and women. AEO sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for American Eagle’s fiscal 2025 sales indicates growth of 2.7%, while the estimate for EPS suggests a decline of 21.3% from the year-ago period’s reported figures. AEO has a trailing four-quarter earnings surprise of 35.1%, on average.

Boot Barn operates as a lifestyle retail chain devoted to western and work-related footwear, apparel and accessories. BOOT flaunts a Zacks Rank #1 at present.

The Zacks Consensus Estimate for Boot Barn’s fiscal 2025 sales and earnings indicates growth of 16.6% and 23.7%, respectively, from the year-ago period’s reported figures. BOOT has a trailing four-quarter earnings surprise of 5.4%, on average.

Gap is a premier international specialty retailer offering a diverse range of clothing, accessories and personal care products. GAP currently sports a Zacks Rank #1.

The Zacks Consensus Estimate for Gap’s fiscal 2025 sales indicates growth of 1.8% from the year-ago period’s reported figures, while the EPS estimate suggests a decline of 2.7%. GAP has a trailing four-quarter earnings surprise of 19.1%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-24 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite