|

|

|

|

|||||

|

|

|

Planet Labs PL is a leading provider of Earth-imaging data and geospatial analytics, operating the largest fleet of Earth-observation satellites globally. The company primarily generates revenues through fixed-price subscriptions and usage-based contracts, delivering imagery and analytics through its cloud-based platform to government and large commercial customers. Despite this, the company is facing a profitability issue.

Though the company experienced significant revenue growth in recent periods, its continuous investment in the development of platforms and satellites, as well as their replacement, weighs on profitability. Given the breadth of its portfolio, Planet Labs needs continuous investments in research and development. Also, higher sales and marketing expense, as well as general and administrative expense, weighs on profitability.

PL has increasingly prioritized securing large government and defense contracts, which provide long-term visibility and stability. At the same time, management views the commercial sector as a substantial growth opportunity as the company continues to enhance its product and solution offerings.

The development of AI-enabled analytics for government customers is expected to drive broader adoption across commercial markets as well, enabling actionable insights for a wide range of use cases, including supply chain monitoring, security, operational optimization, insurance risk assessment, financial analysis, energy management and agricultural productivity. Despite these, a rebound is not expected in the near term.

Just like Planet Labs, Rocket Lab RKLB and BlackSky Technology BKSY are facing a profitability issue and a rebound in the near term is unlikely.

Rocket Lab incurs high operating expenses, caused by investments in innovations like the Neutron launch vehicle, Electron’s first-stage recovery, advanced spacecraft capabilities and an expanded portfolio of components. These expenses often offset revenue gains, leading to losses at Rocket Lab.

Despite achieving strong revenue growth, BlackSky is unable to deliver strong bottom-line performance. BlackSky incurs huge operating expenses in the form of high research and development costs as well as professional and engineering services costs, in addition to high interest expenses due to its huge long-term debt load.

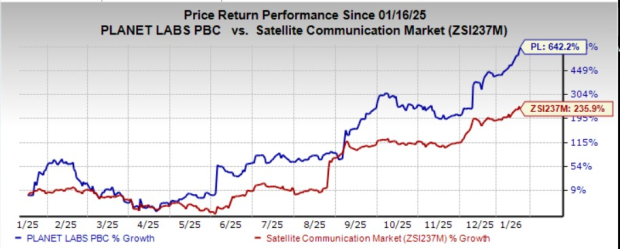

PL has gained 642.2% in a year, outperforming the industry.

The stock is overvalued compared with its industry. It is currently trading at a price-to-sales multiple of 23.83, higher than the industry average of 2.44.

The Zacks Consensus Estimate for PL’s fiscal fourth-quarter 2026 and fiscal first-quarter 2027 EPS witnessed no movement in the last 30 days. The same holds true for fiscal 2026 and 2027 estimates.

The consensus estimates for PL’s 2026 and 2027 revenues and EPS indicate year-over-year increases.

PL stock currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

SpaceX Stock Lands Upgrade, Rocket Lab Surges After Electron Mission

RKLB +9.46%

Investor's Business Daily

|

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite