|

|

|

|

|||||

|

|

|

C3.ai has gotten torched over the last six months - since July 2025, its stock price has dropped 53.8% to $13.09 per share. This may have investors wondering how to approach the situation.

Is there a buying opportunity in C3.ai, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Even with the cheaper entry price, we're swiping left on C3.ai for now. Here are three reasons why AI doesn't excite us and a stock we'd rather own.

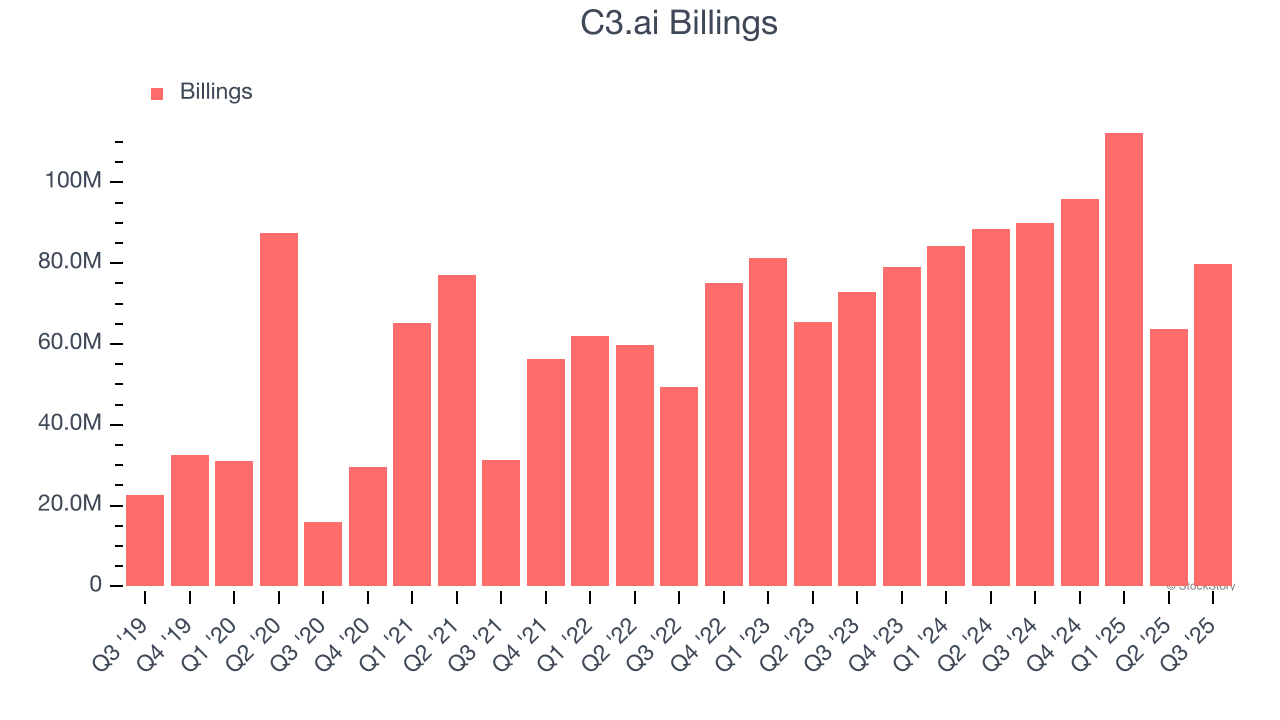

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

C3.ai’s billings came in at $79.9 million in Q3, and over the last four quarters, its year-on-year growth averaged 3.8%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

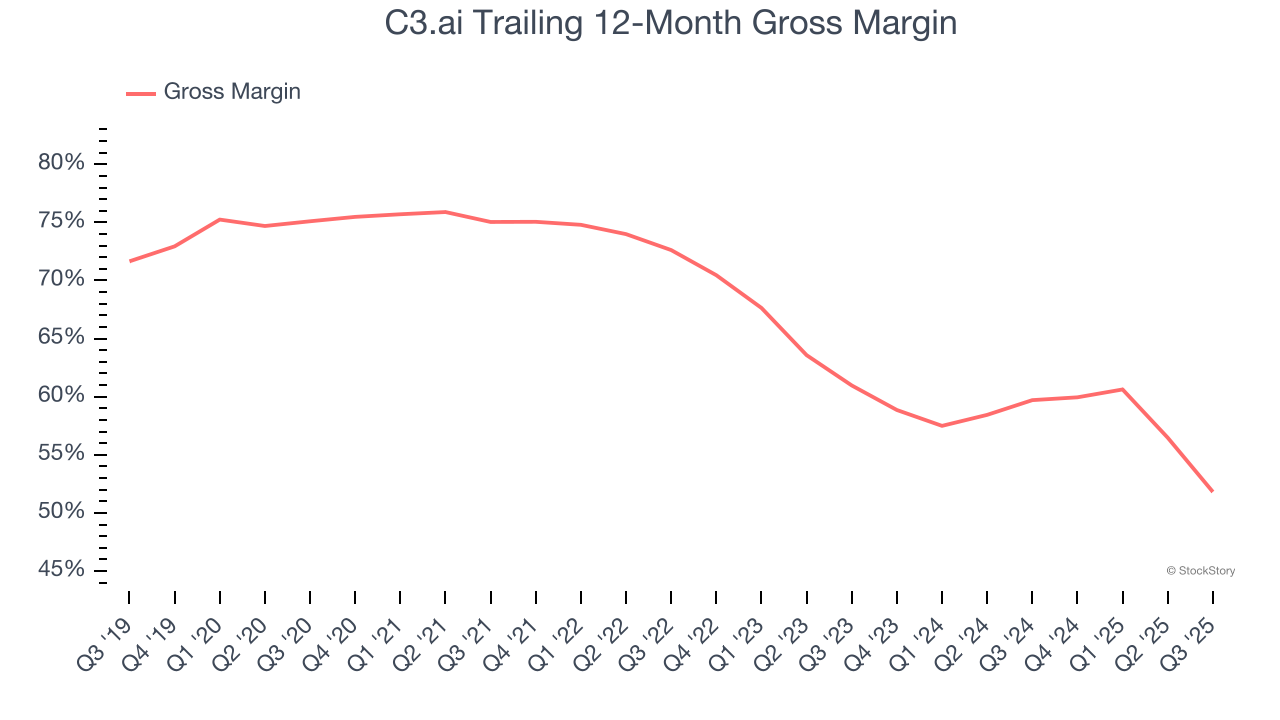

For software companies like C3.ai, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

C3.ai’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 51.8% gross margin over the last year. Said differently, C3.ai had to pay a chunky $48.19 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. C3.ai has seen gross margins decline by 9.2 percentage points over the last 2 year, which is among the worst in the software space.

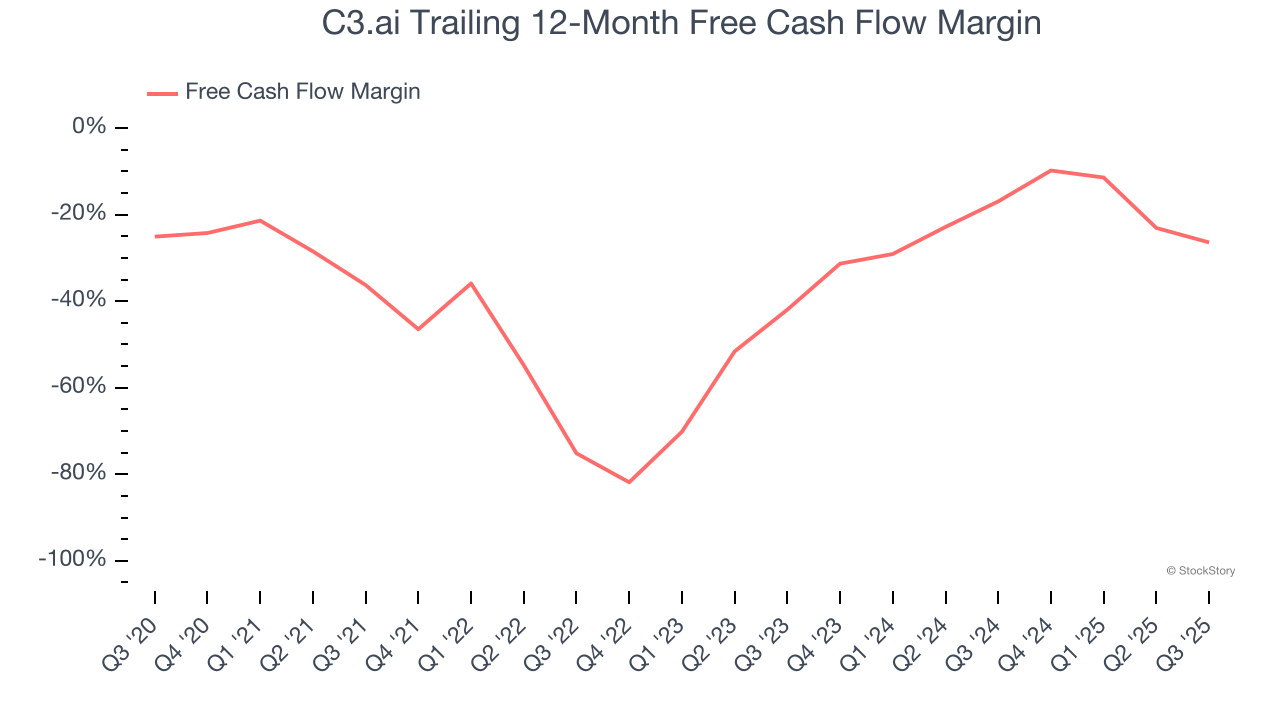

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

C3.ai’s demanding reinvestments have drained its resources over the last year, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 26.4%, meaning it lit $26.42 of cash on fire for every $100 in revenue.

We see the value of companies addressing major business pain points, but in the case of C3.ai, we’re out. Following the recent decline, the stock trades at 5.9× forward price-to-sales (or $13.09 per share). At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere. We’d suggest looking at our favorite semiconductor picks and shovels play.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-07 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 | |

| Mar-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite