|

|

|

|

|||||

|

|

|

Alibaba BABA is promoting quick commerce as a key growth driver, with revenues surging 60% year over year in the second quarter of fiscal 2026, driven by strong order momentum and expansion of Taobao Instant Commerce. This growth is boosting user engagement, increasing monthly active users on the Taobao app and supporting customer management revenues through higher traffic and monetization, though its rising costs are becoming a growing challenge to margins.

Alibaba has acknowledged that heavy spending on subsidies, logistics and user experience is weighing on profitability, particularly within the China e-commerce segment, which plunged 76% year over year in the second quarter of fiscal 2026. Excluding quick commerce losses, core China e-commerce EBITA would have posted mid-single-digit growth — underscoring that quick commerce is currently the dominant drag on profitability and affecting near-term margins.

Cost trends reinforce this pressure. Sales and marketing expenses jumped sharply to nearly 27% of revenues, reflecting intense competition in China’s instant delivery and local commerce markets. At the same time, cash flow has deteriorated meaningfully. Cash generation has softened, largely due to continued investments in quick commerce and supporting infrastructure.

Management has been transparent that adjusted EBITA may fluctuate in the coming quarters as competition remains intense and investment levels stay high. With costs likely to increase, EBITA volatility is likely to continue, suggesting that margin pressure is not only mounting but may persist longer than expected.

JD.com JD poses stiff competition to Alibaba by focusing on a self-operated, price-competitive and supply-chain-driven model. JD.com benefits from strong quality control, faster delivery and high customer trust, especially in electronics and home appliances. In the third quarter of 2025, JD.com posted revenue growth of 14.9% to RMB299.1 billion, supported by retail expansion and price competitiveness, even as higher logistics costs pressure margins — highlighting Alibaba’s intensifying competitive landscape.

PDD Holdings PDD intensifies competition with Alibaba through its low-cost, social commerce model. PDD Holdings emphasizes price efficiency, strong user engagement and a capital-light structure that supports high profitability. In the third quarter of 2025, PDD Holdings delivered solid revenue growth and strong net income gains, pressuring Alibaba’s core platforms. Its ability to scale quickly, monetize merchants and maintain healthy margins highlights growing competitive pressure.

BABA shares have gained 37.5% in the past six-month period, outperforming the Zacks Internet – Commerce industry and the Zacks Retail-Wholesale sector’s growth of 3.1% and 6.4%, respectively.

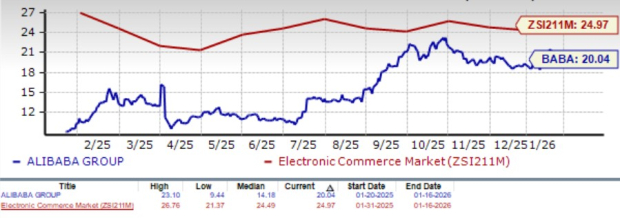

From a valuation standpoint, BABA stock is currently trading at a forward 12-month Price/Earnings ratio of 20.04X compared with the industry’s 24.97X. BABA has a Value Score of F.

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $6.10 per share, down by 5% over the past 30 days and indicating a 32.3% year-over-year decline.

Alibaba currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 6 hours | |

| 8 hours | |

| 9 hours | |

| 11 hours | |

| 14 hours | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite