|

|

|

|

|||||

|

|

|

Artificial intelligence stocks soared to start 2026, boosted by Taiwan Semiconductor’s impressive Q4 report and guidance that confirmed the AI spending boom is heating up.

Investors with long-term outlooks should consider buying best-in-class AI stocks now to make sure they are exposed to what could be another blockbuster year for Wall Street in 2026, driven by soaring earnings growth and lower interest rates.

Check out the Zacks Earnings Calendar to stay ahead of market-moving news.

Let’s dive into two of the best AI-boosted technology stocks to consider buying right now and holding for the long haul.

First up is soaring Zacks Rank #1 (Strong Buy) memory chip powerhouse Micron. After that, we look at AI data center networking standout Arista Networks, which works with Meta and others and earns a Zacks Rank #2 (Buy).

Wall Street was already expecting 2026 to be another blockbuster year for AI stocks, driven by the ongoing capex boom.

Taiwan Semi’s TSM blowout beat-and-raise Q4 report on January 15 cemented the bull case for buying AI stocks in 2026 even after a massive run over the last few years.

The semiconductor manufacturing powerhouse, which makes chips for Nvidia, Apple, and other Mag 7 technology companies, boosted its 2026 capex guidance to $52 billion to $56 billion, blowing away 2025's $40.9 billion.

The AI chip manufacturer also expects to expand its revenue by another 30% in 2026 as part of a projected CAGR of ~25% between 2024 and 2029.

AI hyperscalers are projected to spend roughly $530 billion in capex this year, up from around $400 billion in 2025 as they fight for their share of the growing AI pie. On top of that, global AI data center infrastructure spending is expected to reach ~$7 trillion by 2030.

The chart above highlights how much the Tech sector’s 2026 earnings outlook has improved from early July until now, as demonstrated by the Mag 7.

Wall Street is also increasingly upbeat about earnings expansion across the entire economy. All 16 Zacks sectors are projected to post positive earnings growth in 2026, which would mark the first time that’s happened since 2018.

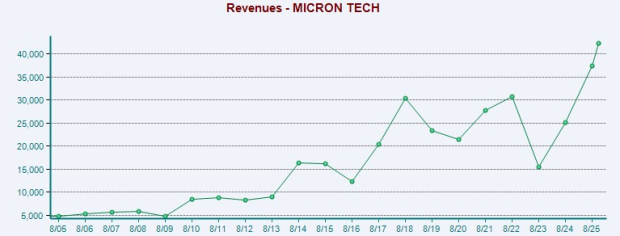

Micron Technology, Inc. MU is a semiconductor memory chip powerhouse that easily doubled its revenue between 2010 and 2020, well before the artificial intelligence age began. The AI boom is sending MU’s growth into hyperdrive (+95% revenue projected in FY26 alone) because it’s a leader in high-bandwidth memory (HBM) offerings that are increasingly critical for AI workloads.

Micron raised its outlook after reporting a strong first quarter of 2026 on December 17. The “essential AI enabler” said its Q2 outlook reflects “substantial records across revenue, gross margin, EPS and free cash flow.” The Boise, Idaho-headquartered company expects its “business performance to continue strengthening through fiscal 2026” as the AI spending spree ramps up.

MU works directly with AI chip powerhouse Nvidia NVDA and its closest rival, AMD. Micron’s CEO and industry analysts project that AI will continue driving record memory chip demand.

The company is projected to increase its revenue by 95% in FY26 and another 24% next year to climb from $37.38 billion in FY25 to $90 billion in FY27. This top-line expansion follows back-to-back years of at ~50% sales growth or higher.

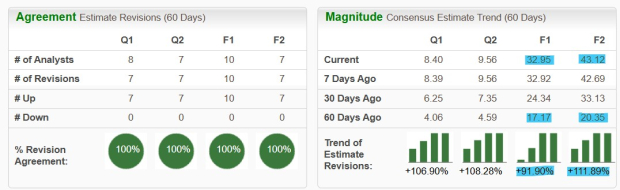

Micron grew its GAAP earnings per share (EPS) by 1,016% in FY25 and its adjusted EPS by 540%. The company’s beat-and-raise Q1 sent analysts racing to raise their 2026 and 2027 estimates yet again. MU’s FY26 Zacks consensus has soared 92% in the last 60 days, with its FY27 estimate 112% higher.

The AI chip stock’s stellar EPS revisions earn it a Zacks Rank #1 (Strong Buy). MU is projected to grow its EPS by a mind-boggling 298% in FY25 (from $8.29 to $32.95) and then 31% next year.

The rapid expansion of AI data centers and the growing AI arms race could see Micron become increasingly untethered from the historically boom-and-bust memory chip cycle. Its standing as the only U.S.-based memory manufacturer enhances its long-term bull case as the U.S. races to dominate AI and build the most cutting-edge chips domestically.

Micron is a vertically integrated semiconductor company, meaning it designs, manufactures, and tests most of its chips in-house, unlike fabless companies such as Nvidia, which outsource manufacturing to companies such as Taiwan Semi.

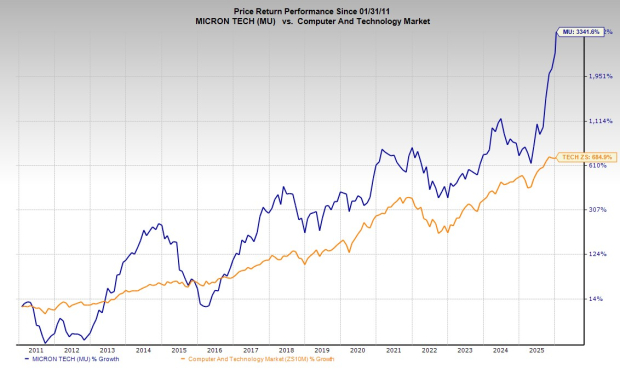

MU stock has soared 245% in the last 12 months to crush the Tech sector’s 26% and Nvidia’s 35%. Micron’s recent run, which is part of a 3,200% charge in the past 10 years, helped it break out meaningfully above its 2000 and pre-dot.com bubble peaks.

Micron is trading miles above its 21-day and 21-week moving averages and at some overheated RSI levels. This means that some investors might want to wait for a pullback to one of those levels before they dip their toes into the stock. But market timing is extremely difficult.

Plus, Micron’s stellar earnings growth outlook has it trading at a 65% discount to the Zacks Tech (27.4X) sector and in line with its own historic median at 10.0X forward 12-month earnings despite skyrocketing to fresh highs.

Interested investors might want to start an initial position in Micron sooner rather than later, and then buy more shares the next time MU and the broader AI-boosted tech sector experience a significant pullback. Wall Street analysts are convinced that Micron is a great stock to buy, with 27 of the 39 brokerage recommendations Zacks has at “Strong Buys,” alongside five “Buys” and five “Holds” (meaning zero Sells).

Arista Networks ANET has been a key behind-the-scenes player in cutting-edge technologies for a long time. ANET’s networking infrastructure expanded rapidly over the past decade-plus alongside the explosion of cloud computing, big data, and most recently and most critically, AI.

The company helps build and maintain some of the ‘plumbing’ that keeps large-scale technology operations such as AI running smoothly 24/7. Arista is a client-to-cloud networking powerhouse for large AI, data center, campus, and routing environments. ANET’s products help connect computers, servers, and beyond to ensure fast and reliable data transfer.

Arista is steadily expanding its portfolio and its reach in an economy that’s completely reliant on ultra-fast digital infrastructure running efficiently, nonstop. AI hyperscalers, Microsoft and Meta are two of Arista’s largest clients, highlighting to investors that ANET’s portfolio is full of some of the best-in-class offerings.

ANET grew its revenue from $361 million in 2013 to $7 billion in 2024, boosted by 32% average sales growth in the trailing four years. Arista is projected to grow its sales by 27% in FY25 and 21% in 2026 to reach $10.73 billion (more than doubling revenue between 2022 and 2026).

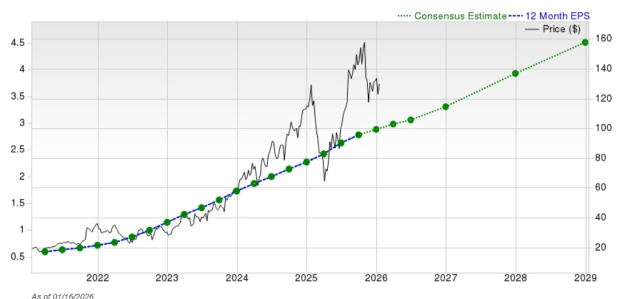

The networking infrastructure firm is projected to grow its adjusted earnings by 27% and 15%, respectively. Arista’s recent upward earnings revisions earn ANET a Zacks Rank #2 (Buy) and extend a steady run over the last several years. The chart below highlights that Arista is projected to expand its earnings to roughly $4.50 a share in 2028 (vs. $2.88 in 2025).

The stock skyrocketed 3,100% in the past 10 years to blow away Tech’s 460%. The AI infrastructure stock also doubled the Zacks Tech sector in the past three years and outpaced every Mag 7 stock outside of Nvidia.

Yet, investors can buy ANET stock down around 20% from its October 2025 peaks, even as many other AI-boosted tech stocks, including Micron, trade at all-time highs. ANET’s average price target also marks 28% upside from its current levels.

On the technical side, Arista stock found support at its 200-day moving average last week. The nearby chart shows that ANET could be ready to break out again once it overtakes its January 2025 levels.

Arista’s valuation levels might be holding back the stock a bit right now. But Wall Street has been willing to pay a premium for ANET for most of the past decade, given its consistent expansion in vital behind-the-scenes areas.

Image Source: Zacks Investment Research

Arista stands to be a winner in the AI age, no matter which hyperscalers grab more market share or how the technology evolves beyond the current large language models.

On top of that, ANET is a well-run company with a pristine balance sheet that includes $10.1 billion in cash and equivalents and zero debt. This backdrop could help ANET expand its reach within AI and beyond.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 min | |

| 18 min | |

| 26 min | |

| 38 min | |

| 40 min | |

| 58 min |

Markets may get 'increasingly nervous' if hyperscalers raise AI capex further

MU

Yahoo Finance Video

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite