|

|

|

|

|||||

|

|

|

Since July 2025, Hewlett Packard Enterprise has been in a holding pattern, posting a small return of 3.8% while floating around $21.45. The stock also fell short of the S&P 500’s 10% gain during that period.

Is there a buying opportunity in Hewlett Packard Enterprise, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We're swiping left on Hewlett Packard Enterprise for now. Here are three reasons why HPE doesn't excite us and a stock we'd rather own.

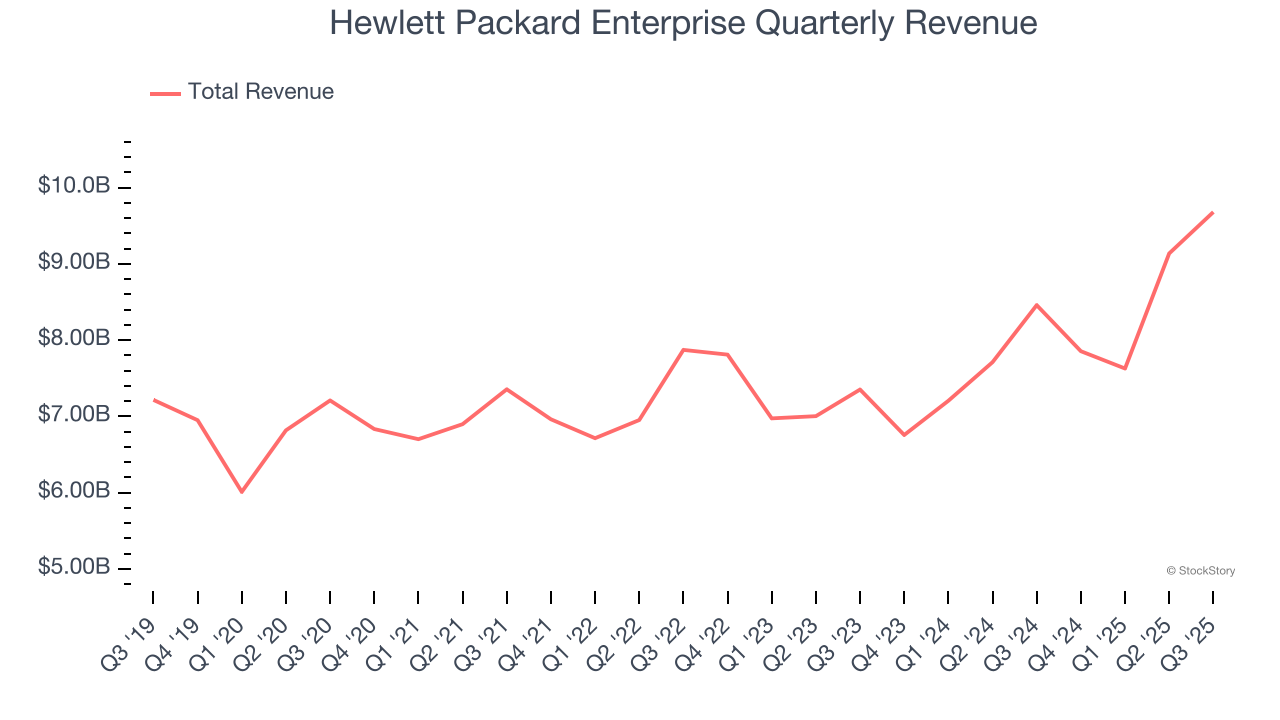

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Hewlett Packard Enterprise grew its sales at a mediocre 4.9% compounded annual growth rate. This was below our standard for the business services sector.

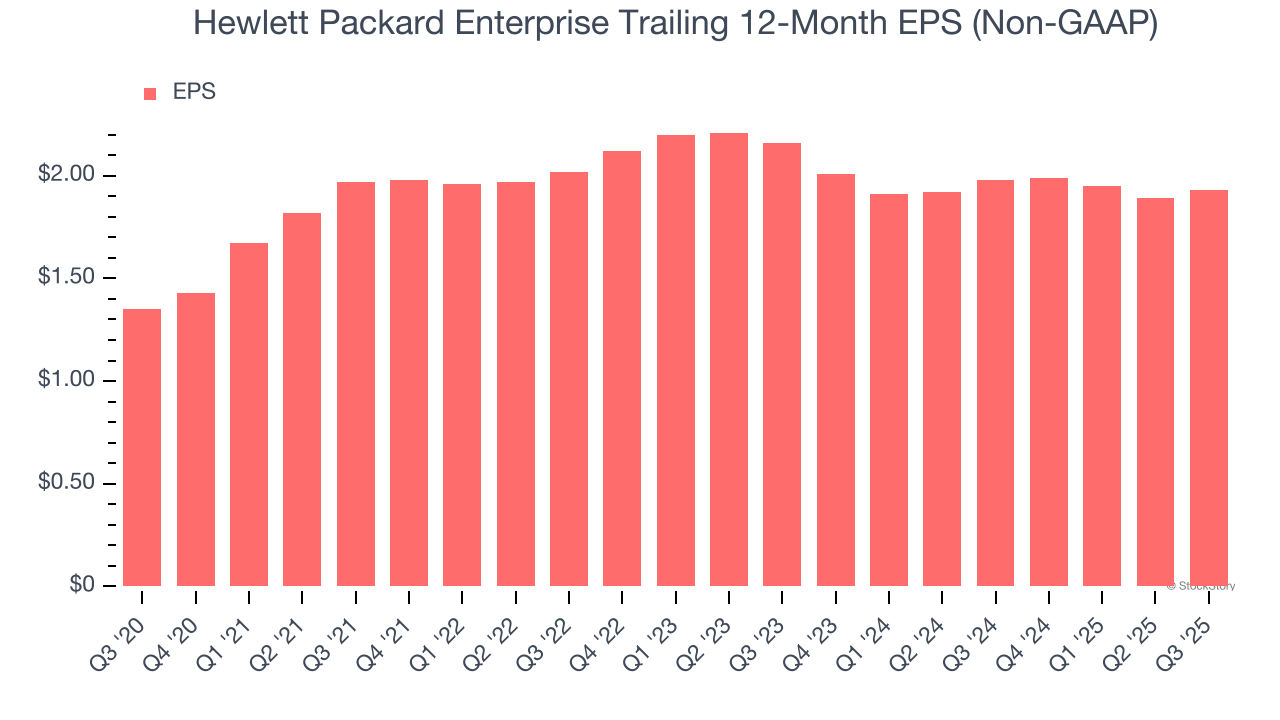

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Hewlett Packard Enterprise’s EPS grew at an unimpressive 7.4% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 4.9% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

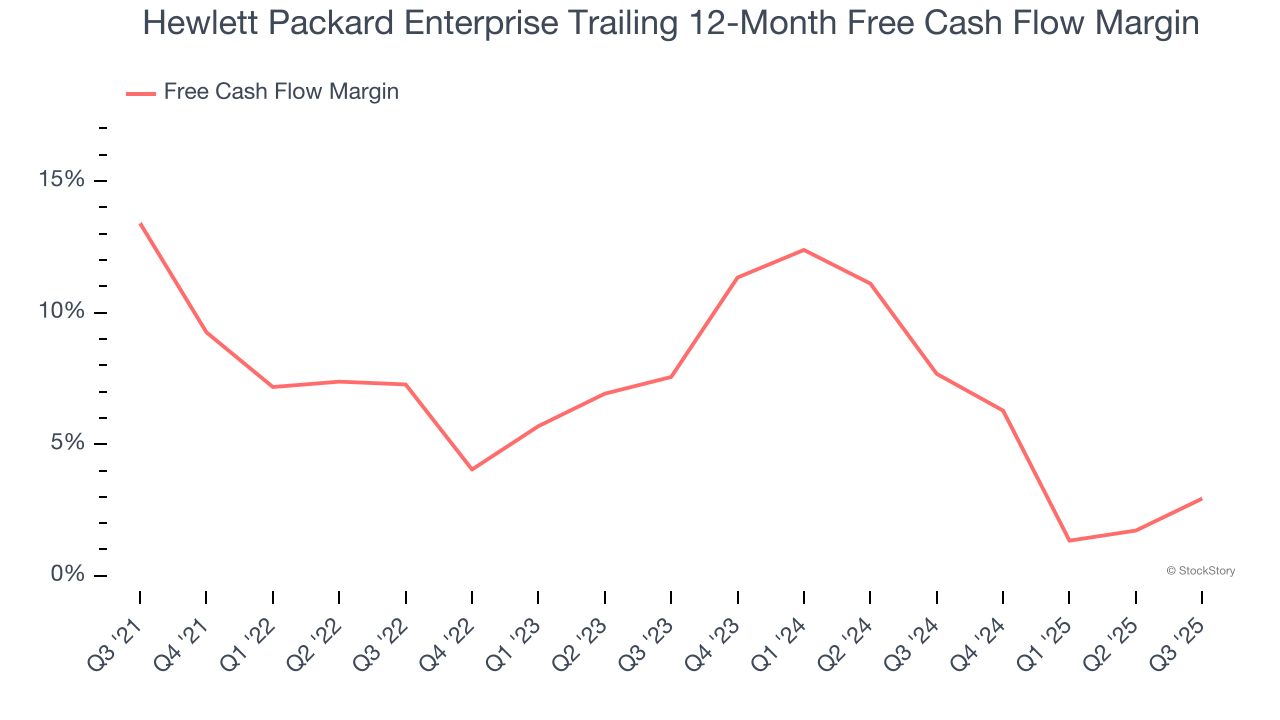

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Hewlett Packard Enterprise’s margin dropped by 10.5 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Hewlett Packard Enterprise’s free cash flow margin for the trailing 12 months was 2.9%.

Hewlett Packard Enterprise isn’t a terrible business, but it doesn’t pass our quality test. With its shares lagging the market recently, the stock trades at 9.1× forward P/E (or $21.45 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere. We’d suggest looking at our favorite semiconductor picks and shovels play.

Check out the high-quality names we’ve flagged in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Jun-26 | |

| Jun-25 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-23 | |

| Jun-22 | |

| Jun-22 | |

| Jun-22 | |

| Jun-21 | |

| Jun-19 | |

| Jun-18 | |

| Jun-17 | |

| Jun-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite