|

|

|

|

|||||

|

|

|

Bristol Myers Squibb BMY and GSK PLC GSK are among the largest global biopharma companies with broad and diverse portfolios.

Bristol Myers Squibb focuses on the discovery, development and commercialization of transformational therapies across oncology, hematology, immunology, cardiovascular disease, neuroscience and other serious conditions.

GSK offers one of the most diversified portfolios in the global pharma and biotech industry, with strong positions in HIV, oncology and respiratory diseases, complemented by a robust vaccine business.

Both companies have established solid competitive positions in their core markets and have consistently delivered returns to shareholders.

Against this backdrop, selecting one stock over the other is not easy. A closer examination of their fundamentals, growth prospects, risks and valuation metrics is necessary to determine the more attractive investment opportunity.

BMY’s Growth Portfolio comprises drugs like Opdivo, Opdivo Qvantig, Orencia, Yervoy, Reblozyl, Camzyos, Breyanzi, Opdualag, Zeposia, Abecma, Sotyku, Krazati and Cobenfy.

The recent performance of this portfolio has been strong, maintaining top-line growth for BMY.

Opdivo sales in the United States are being driven by a strong launch in MSI-high colorectal cancer and continued growth in first-line non-small cell lung cancer, while international sales are supported by label expansion of the drug across multiple markets.

The approval of Opdivo Qvantig (nivolumab and hyaluronidase-nvhy) injection for subcutaneous use has boosted BMY’s immuno-oncology portfolio. The initial uptake has been strong and the launch is going well in the United States across all indicated tumor types.

Bristol Myers now expects global Opdivo sales, together with Qvantig, to increase in the high single-digit to low double-digit range in 2025 (previous guidance: mid to high single-digit range in 2025), driven by strong performance year to date.

The stellar performance of the thalassemia drug Reblozyl, for which BMY has a collaboration agreement with Merck (MRK), has significantly boosted BMY’s top line. BMY is now annualizing over $2 billion in Reblozyl sales. Revenue growth continues to be strong, primarily due to demand in first-line RS-positive and RS-negative settings as well as improved duration of therapy.

Breyanzi sales are now annualizing over $1 billion, reflecting strong growth in large B-cell lymphoma and expansion in new indications approved last year.

Cardiovascular drug Camzyos sales continue to increase on robust demand.

The FDA approval for xanomeline and trospium chloride (formerly KarXT), an oral medication for the treatment of schizophrenia, in adults (under the brand name Cobenfy), is a significant boost for the company.

The initial uptake is encouraging, with sales of $105 million year to date. Cobenfy is expected to contribute meaningfully to BMY’s top line in the coming years as the company looks to expand the drug’s label into other indications.

However, while BMY is progressing with its growth portfolio, its legacy portfolio is being adversely impacted due to continued generic impact on Revlimid, Pomalyst, Sprycel and Abraxane.

The decline in sales of legacy drugs has adversely impacted the top line. BMY continues to expect the legacy portfolio to decline approximately 15-17% in 2025.

The legacy portfolio also comprises blood thinner medicine Eliquis, for which BMY has a worldwide co-development and co-commercialization agreement with pharma giant Pfizer PFE. Eliquis is the biggest contributor to the top line.

Meanwhile, BMY is on the lookout for acquisitions/collaborations to broaden its portfolio and drive top-line growth.

The recent acquisition of privately held biotechnology company Orbital Therapeutics will add OTX-201, Orbital’s lead RNA immunotherapy preclinical candidate currently in IND-enabling studies, to BMY’s pipeline. OTX-201, a next-generation CAR T-cell therapy, is designed to reprogram cells in vivo with a potential best-in-class profile for autoimmune disease. BMY will also add Orbital’s proprietary RNA platform to its pipeline.

The company had earlier collaborated with BioNTech BNTX for the global co-development and co-commercialization of BioNTech’s investigational bispecific antibody BNT327 across numerous solid tumor types.

Nonetheless, BMY is looking to boost its bottom line through cost-cutting initiatives.

While BMY’s strategy of acquiring companies with promising drugs/candidates is encouraging, this has resulted in colossal debt to finance these acquisitions. As of Sept. 30, 2025, Bristol Myers’ total debt-to-total capital was a whopping 72.5%. The company had cash and equivalents of $15.7 billion and a long-term debt of $44.5 billion as of the same date.

Strong sales growth in GSK’s Specialty Medicines unit (HIV, Oncology, Immunology/Respiratory, and Other), fueled by successful new launches in oncology and long-acting HIV medicines, is driving top-line growth.

Top drugs like Nucala and Dovato continue to be key revenue growth drivers in this segment. New long-acting HIV medicine, Cabenuva, along with oncology drugs Jemperli and Ojjaara, has boosted the top line, driven by strong patient demand.

GSK is also developing innovative ultra-long-acting HIV regimens for treatment and prevention, which can extend the dosing intervals of the injections.

In addition, label expansion of key drugs like Nucala (for COPD) and approval of new drugs such as Ojjaara for myelofibrosis with anemia, Blujepa/gepotidacin for treating uncomplicated urinary tract infection, Apretude, a long-acting injectable form of cabotegravir drug for the prevention of HIV infection, and Exdensur (depemokimab) for severe asthma should further propel growth.

Although GSK’s Vaccines portfolio is also diversified, this franchise is under pressure due to lower sales of some products like the RSV vaccine, Arexvy. Nonetheless, approval of new products like Penmenvy, GSK’s pentavalent MenABCWY meningococcal vaccine should help revive growth..

While GSK is working to further expand the label of drugs like Nucala and Blenrep, it also has a deep pipeline. Promising candidates in late-stage development include bepirovirsen (chronic hepatitis B), tebipenem pivoxil (complicated UTIs), linerixibat (cholestatic pruritus in primary biliary cholangitis), camlipixant (refractory chronic cough) and GSK5764227 (antibody drug conjugate for second-line extensive stage small cell lung cancer), among others.

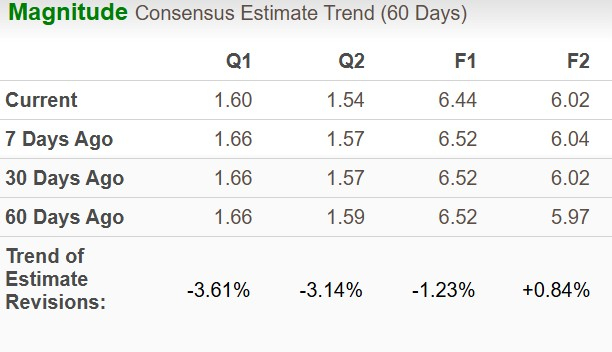

The Zacks Consensus Estimate for BMY’s 2025 sales implies a year-over-year decrease of 0.80%, while that for EPS suggests an increase of 460%. The extraordinary EPS growth rate can be attributed to an extremely low EPS figure in 2024 due to acquisition expenses.

While EPS estimates for 2025 have moved down to $6.44 in the past 60 days, the same for 2026 has inched up to $6.02.

The Zacks Consensus Estimate for GSK’s 2025 sales implies a year-over-year increase of 6.92% and that for EPS suggests growth of 12.10%. EPS estimates for both 2025 and 2026 have moved north in the past 60 days.

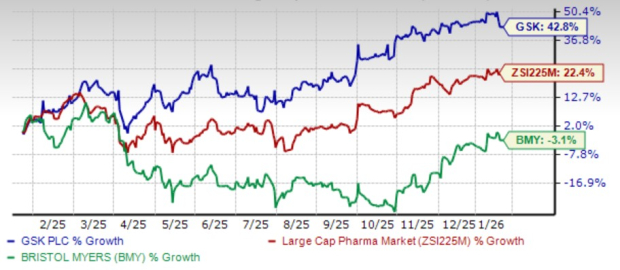

From a price-performance perspective, GSK has fetched better returns than BMY in the past year. Shares of GSK have gained 42.8%, while those of BMY have lost 3.1%. The large-cap pharma industry has gained 22.4% in the said period.

From a valuation standpoint, we use the P/E ratio of the large-cap pharma industry to compare these companies. Going by the same, GSK is slightly more expensive than BMY. GSK’s shares currently trade at 9.85X forward earnings, higher than 9.19X for BMY. The large-cap pharma industry currently trades at 17.72X forward earnings.

Both GSK and BMY have an attractive dividend yield. This is a strong positive for investors. However, BMY's dividend yield of 4.56% is higher than GSK’s 3.53%.

Large pharma/biotech companies are generally considered safe havens for investors interested in this sector. However, with both BMY and GSK stocks currently carrying a Zacks Rank #3 (Hold), choosing one over the other could be tricky. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

BMY’s efforts to revive the top line in the face of generic challenges for key drugs are commendable. Approval of new drugs and label expansion of key drugs should generate incremental revenues for the company. However, we believe there is still time before the efforts reap a harvest for the company.

GSK’s diversified revenue base with a broad global footprint has enabled it to maintain top-line momentum. The company’s strong HIV portfolio and approval of newer treatments should propel growth. Label expansion of key drugs like Nucala and approval of new drugs should generate incremental sales growth. However, the Vaccines portfolio is under pressure.

We believe GSK is a better pick at present, primarily due to the diversity and strength of its portfolio and its stronger returns over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours |

Schrödinger and BMS expand partnership to deploy AI for drug discovery

BMY

Pharmaceutical Technology

|

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 |

Novo Nordisk CEO Remains Open to Bolt-On Acquisitions, But Rules out Transformative Deals

BMY

The Wall Street Journal

|

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite