|

|

|

|

|||||

|

|

|

The past six months have been a windfall for Dycom’s shareholders. The company’s stock price has jumped 42.7%, hitting $366.38 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Following the strength, is DY a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Working alongside some of the most popular mobile carriers in the world, Dycom (NYSE:DY) builds and maintains telecommunications infrastructure.

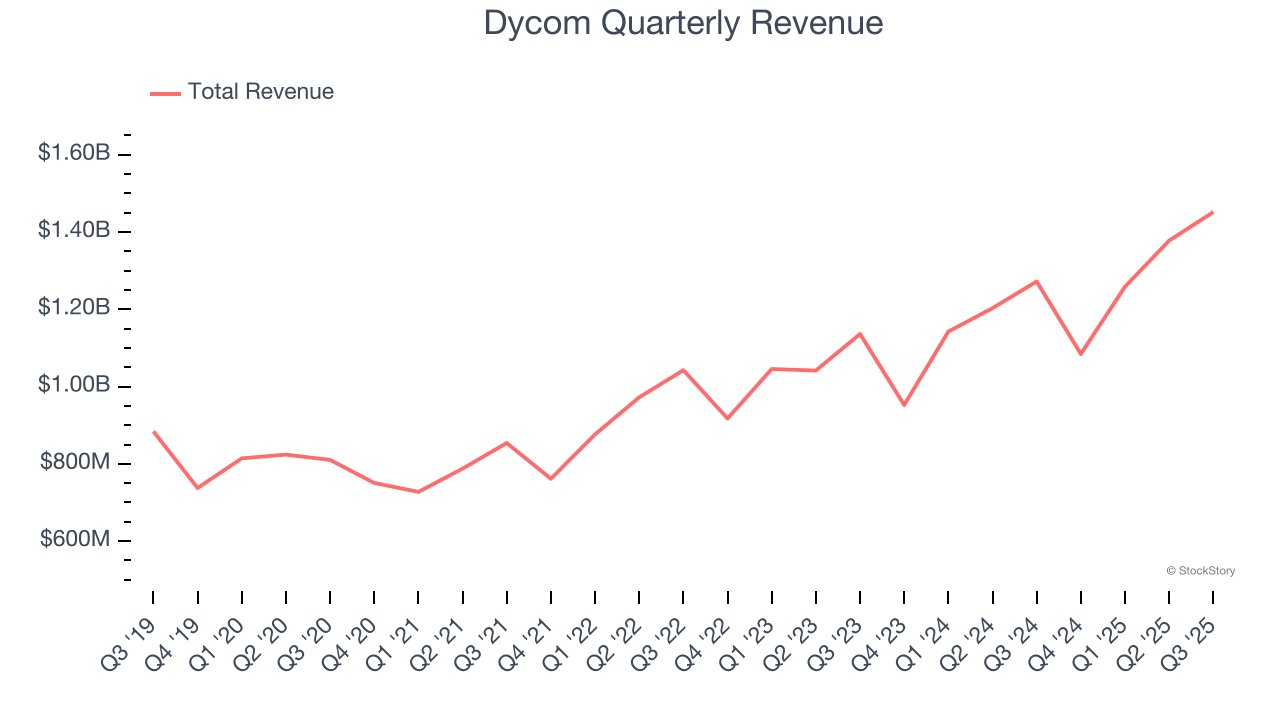

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Dycom’s sales grew at a solid 10.2% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers.

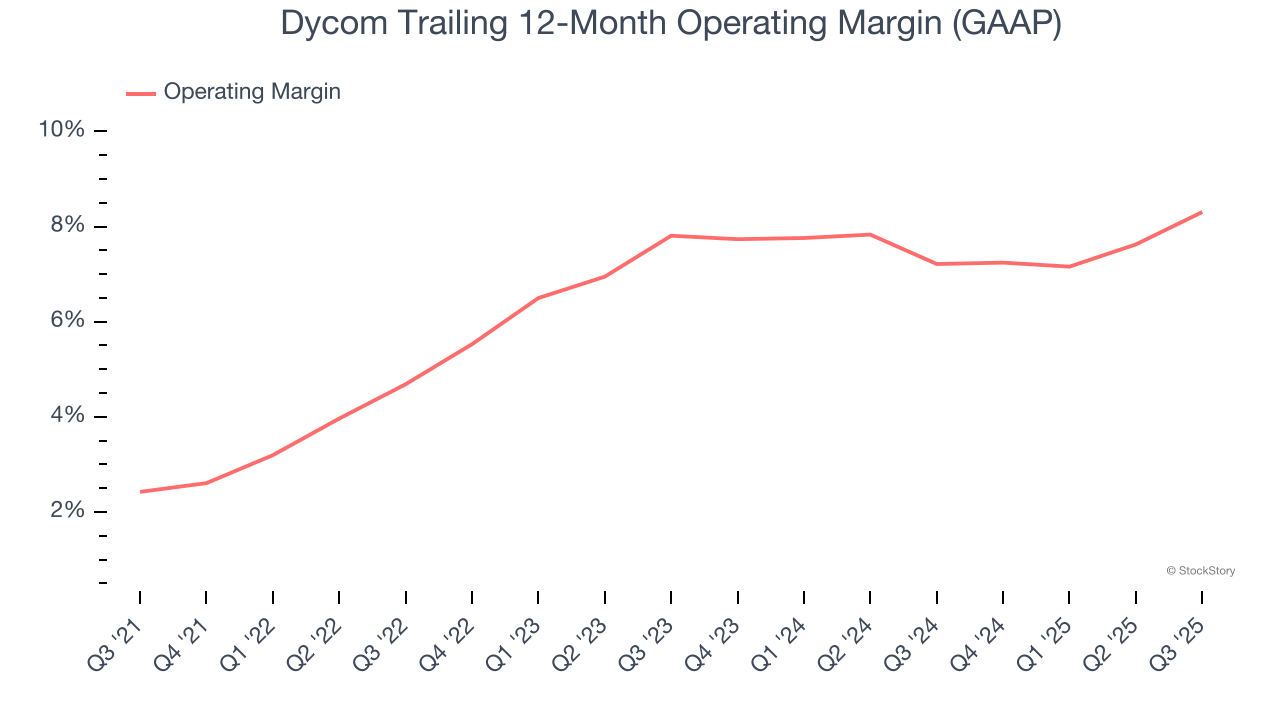

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Dycom’s operating margin rose by 5.9 percentage points over the last five years, as its sales growth gave it immense operating leverage. Its operating margin for the trailing 12 months was 8.3%.

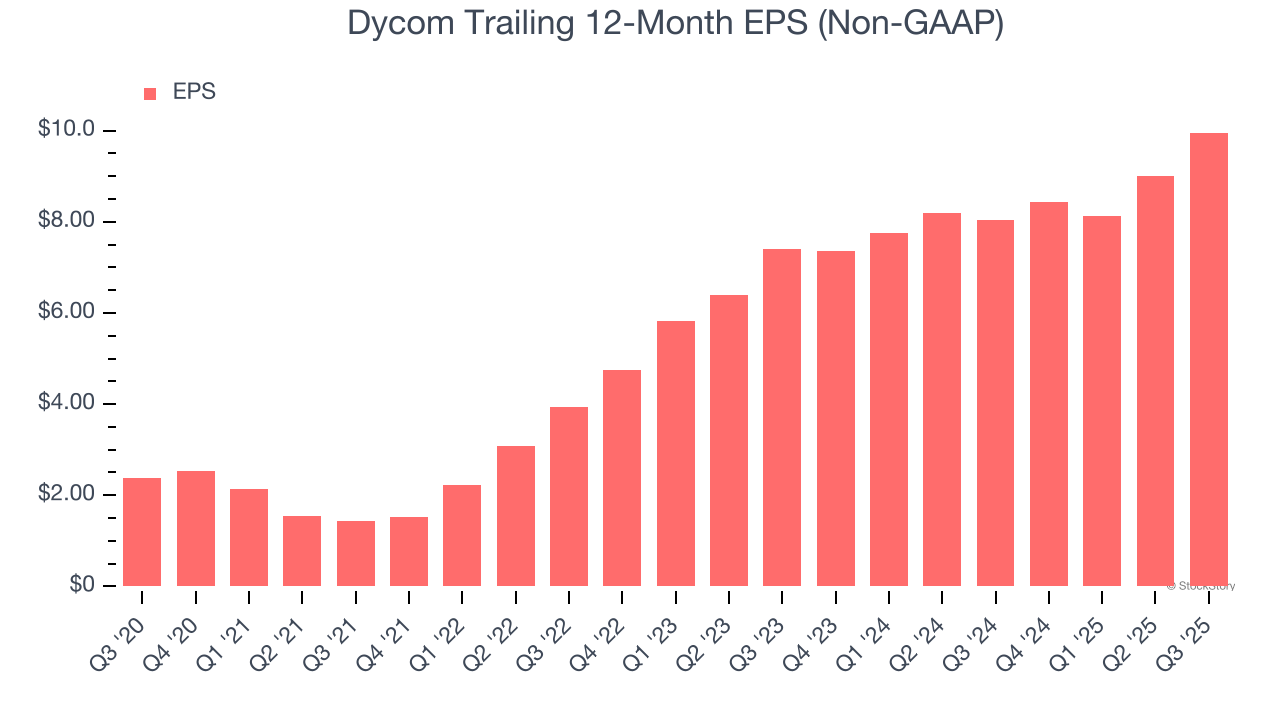

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Dycom’s EPS grew at an astounding 33.3% compounded annual growth rate over the last five years, higher than its 10.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

These are just a few reasons Dycom is a high-quality business worth owning, and with the recent surge, the stock trades at 29× forward P/E (or $366.38 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Aug-04 | |

| Jun-02 | |

| May-29 |

Stock Market Hits Highs On Iran Deal Hopes; Dell, NetApp, Okta Lead Earnings Winners: Weekly Review

DY

Investor's Business Daily

|

| May-27 | |

| May-27 | |

| May-27 | |

| May-27 |

Dycom Soars As Earnings, Revenue Growth Accelerate Amid Data Center Acquisitions

DY +25.84%

Investor's Business Daily

|

| May-27 | |

| May-27 | |

| May-27 | |

| May-27 | |

| May-15 | |

| May-03 | |

| May-02 |

Broadcom, Viking, Rio Tinto Lead Five Stocks Near Buy Points In Strong Market

DY

Investor's Business Daily

|

| Apr-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite