|

|

|

|

|||||

|

|

|

Navitas Semiconductor NVTS and Analog Devices ADI are two key players operating in the semiconductor industry. They benefit from the growing demand for data centers, artificial intelligence (AI) infrastructure, and energy-efficient technologies.

Navitas Semiconductor focuses on Gallium nitride (GaN) and Silicon carbide (SiC) chips used in next-generation AI data centers and energy systems. Analog Devices manufactures semiconductor devices, specifically, analog, mixed signal and digital signal processing integrated circuits.

Both NVTS and ADI are positioned to benefit from long-term growth in data centers and advanced technology infrastructure. However, from an investment point of view, one stock offers a more favorable outlook than the other right now. Let’s break down their fundamentals, growth prospects, market challenges and valuation to determine which stock offers a more compelling investment case.

Navitas Semiconductor is trying to reposition itself around high-power markets, and its inclusion in NVIDIA’s new 800-volt AI factory ecosystem is an important step. The new architecture shifts data center power distribution from traditional AC/DC stages to a high-voltage DC approach that requires faster, more efficient power electronics. This creates an opening for Navitas Semiconductor’s GaN and high-voltage SiC technologies, both of which are now part of the NVIDIA-led ecosystem.

In the third quarter of 2025, Navitas Semiconductor highlighted that it is one of the few companies offering both GaN and SiC solutions, all the way from the grid to graphics processor units. The company has begun sampling mid-voltage GaN devices at 100 volts, which target the last stage of power conversion inside AI servers. NVTS is also sampling 2.3 kV and 3.3 kV SiC modules for grid and energy storage applications that support these new data center designs.

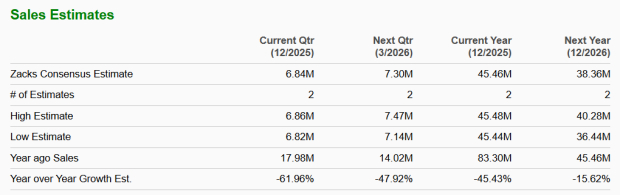

However, the company’s decision to deprioritize its lower-margin China mobile business weighs on its near-term prospects. The company is walking away from low-margin mobile products to focus its resources on high-power business. In the third quarter of 2025, revenues were about $10.1 million, down more than 50% from last year due to weak demand and strong pricing pressure in the mobile business, especially in China.

For the fourth quarter of 2025, management projects revenues to be around $7 million, which represents another sequential decline. The company is reducing exposure to low-margin mobile and consumer customers, cutting channel inventory, and consolidating distributors, all of which reduce near-term revenues. The Zacks Consensus Estimate for Navitas Semiconductor’s 2026 revenues is pegged at $38.36 million, indicating a year-over-year decline of 15.6%.

Analog Devices is seeing strong demand from AI-related data center spending, and this is becoming an important part of its growth story. In the fourth quarter of fiscal 2025, revenues from ADI's data center segment crossed a $1 billion annual run-rate. This represents a year-over-year increase of more than 50% for the third straight quarter.

Management linked this momentum directly to continued strength in the AI infrastructure market. AI servers require more power and higher-speed data movement compared to traditional computing systems. This is fueling higher investment in AI infrastructure, which helped drive a record year for ADI's data center segment.

ADI is seeing strong demand for high-throughput connectivity and power delivery solutions. These products are important inside AI data centers because higher compute workloads create more stress on networking and power systems. As more AI systems are deployed, these needs continue to rise. This data center strength bodes well for ADI’s Communications end market as well. Communications was its fastest-growing market, increasing 26% on a year-over-year basis in fiscal 2025, where the growth was driven by the strong performance in ADI's data center segment.

Looking ahead, ADI expects this momentum to continue. Management said that it is confident about continued data center growth through fiscal 2026, where it pointed out hyperscaler capital spending plans have continued moving higher, with several large hyperscalers increasing their original CapEx plans. Overall, the above-mentioned factors suggest that AI demand is not just a short-term boost. With a growing data center business, strong customer demand for power and connectivity products, ADI remains well-positioned to ride the AI-driven data center growth.

Analog Devices expects revenues of $3.1 billion (+/- $100 million) for the first quarter of fiscal 2026. The Zacks Consensus Estimate for Analog Devices’ fiscal 2026 revenues is pegged at $12.89 billion, indicating year-over-year growth of 16.9%.

Analog Devices has a steady earnings growth outlook compared with Navitas Semiconductor.

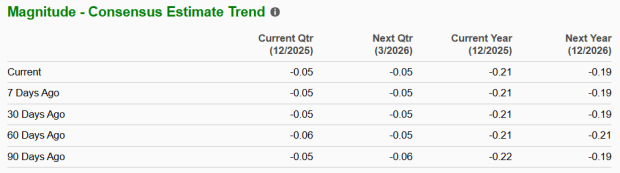

The Zacks Consensus Estimate for Navitas Semiconductor’s 2026 bottom line is pegged at a loss of 19 cents per share, unchanged over the past 30 days.

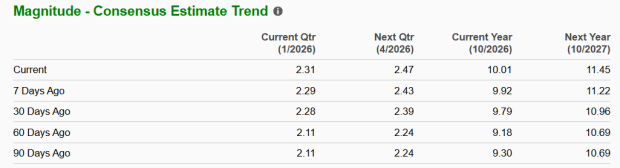

The Zacks Consensus Estimate for Analog Devices’ fiscal 2026 earnings is pegged at $10.01 per share, revised up by 9 cents over the past seven days. This indicates a 28.5% increase year over year.

In the past three months, Analog Devices shares have surged 23.1%, while shares of Navitas Semiconductor have lost 27.1%.

Currently, Analog Devices is trading at a forward sales multiple of 11.28X, lower than Navitas Semiconductor’s forward sales multiple of 63.2X. Analog Devices’ reasonable valuation makes it more attractive for investors looking for value and stability.

Navitas Semiconductor and Analog Devices are both set to ride the long-term growth in AI and data center markets, but their current positions are very different. Currently, Navitas Semiconductor is facing risks of lower revenues and near-term uncertainty as it shifts away from the lower-margin mobile business.

In contrast, Analog Devices stands out with clear momentum in its data center business, strong AI-driven demand for power and connectivity solutions, and a healthier revenue growth outlook for fiscal 2026. ADI’s reasonable valuation offers downside protection as well, making it a better choice for investors looking for stability and steady upside.

Currently, Analog Devices sports a Zacks Rank #1 (Strong Buy), making the stock a clear winner over Navitas Semiconductor, which carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-13 | |

| Jul-10 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 | |

| Jul-06 | |

| Jul-06 | |

| Jun-26 | |

| Jun-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite