|

|

|

|

|||||

|

|

|

Sprouts has gotten torched over the last six months - since July 2025, its stock price has dropped 56.1% to $73 per share. This might have investors contemplating their next move.

Given the weaker price action, is now a good time to buy SFM? Find out in our full research report, it’s free.

Playing on the secular trend of healthier living, Sprouts Farmers Market (NASDAQ:SFM) is a grocery store chain emphasizing natural and organic products.

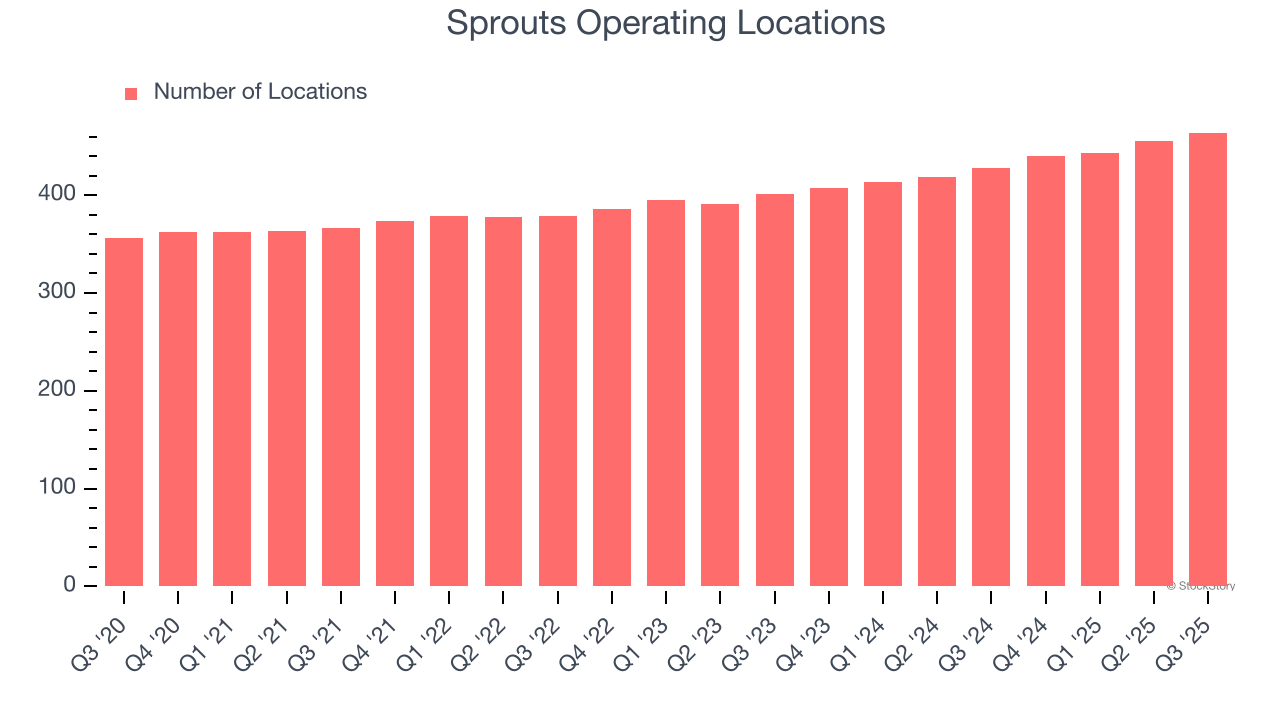

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Sprouts sported 464 locations in the latest quarter. Over the last two years, it has opened new stores at a rapid clip by averaging 7% annual growth, among the fastest in the consumer retail sector. This gives it a chance to become a large, scaled business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

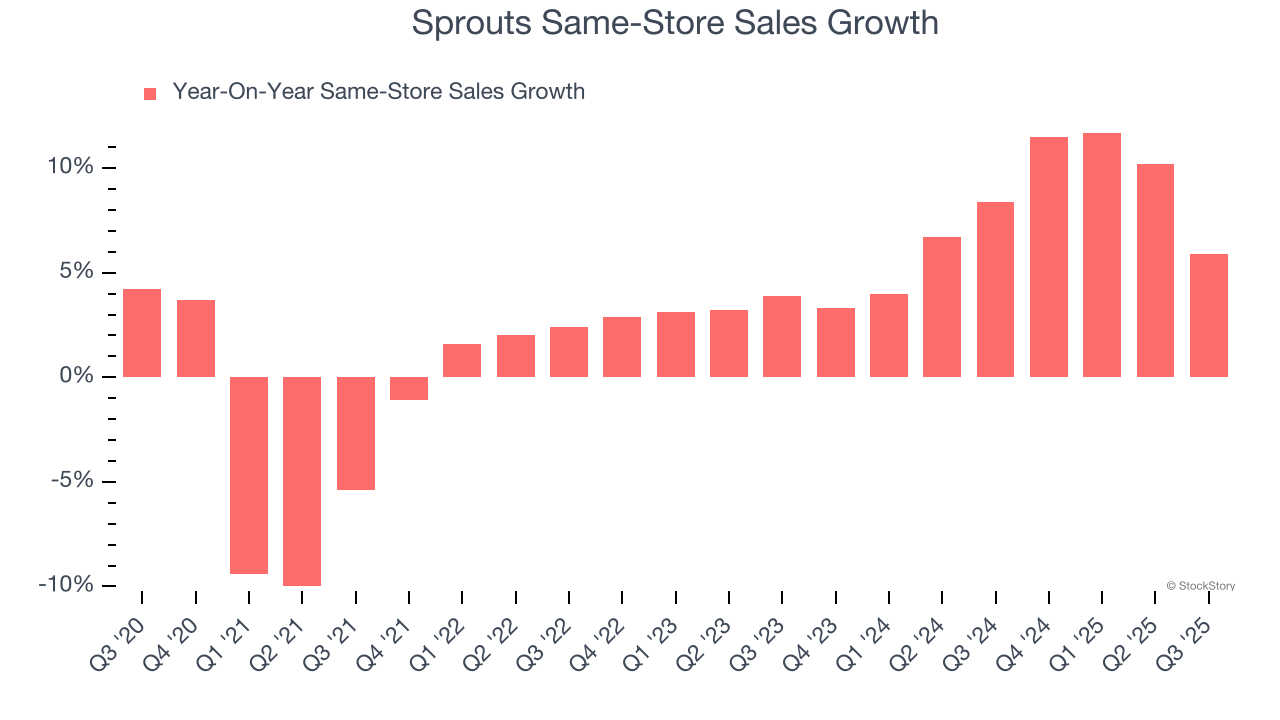

Same-store sales is a key performance indicator used to measure organic growth at brick-and-mortar shops for at least a year.

Sprouts has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing locations. On average, the company has posted exceptional year-on-year same-store sales growth of 7.7%.

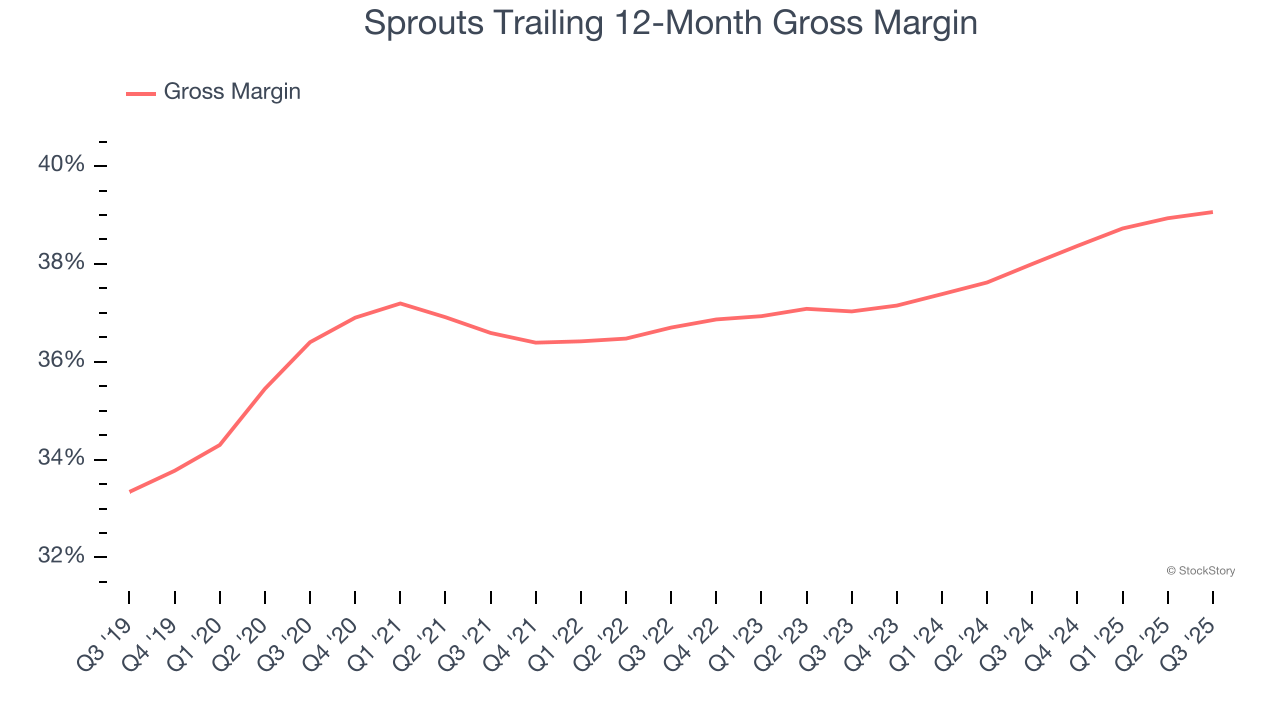

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

Sprouts’s gross margin is slightly below the average retailer, giving it less room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged a 38.6% gross margin over the last two years. That means Sprouts paid its suppliers a lot of money ($61.43 for every $100 in revenue) to run its business.

Sprouts has huge potential even though it has some open questions. With the recent decline, the stock trades at 14.2× forward P/E (or $73 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-21 | |

| Jul-17 | |

| Jul-02 | |

| Jun-30 | |

| Jun-07 | |

| May-19 | |

| May-18 | |

| May-08 | |

| Apr-30 | |

| Apr-30 | |

| Apr-30 | |

| Apr-29 | |

| Apr-29 | |

| Apr-06 | |

| Mar-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite