|

|

|

|

|||||

|

|

|

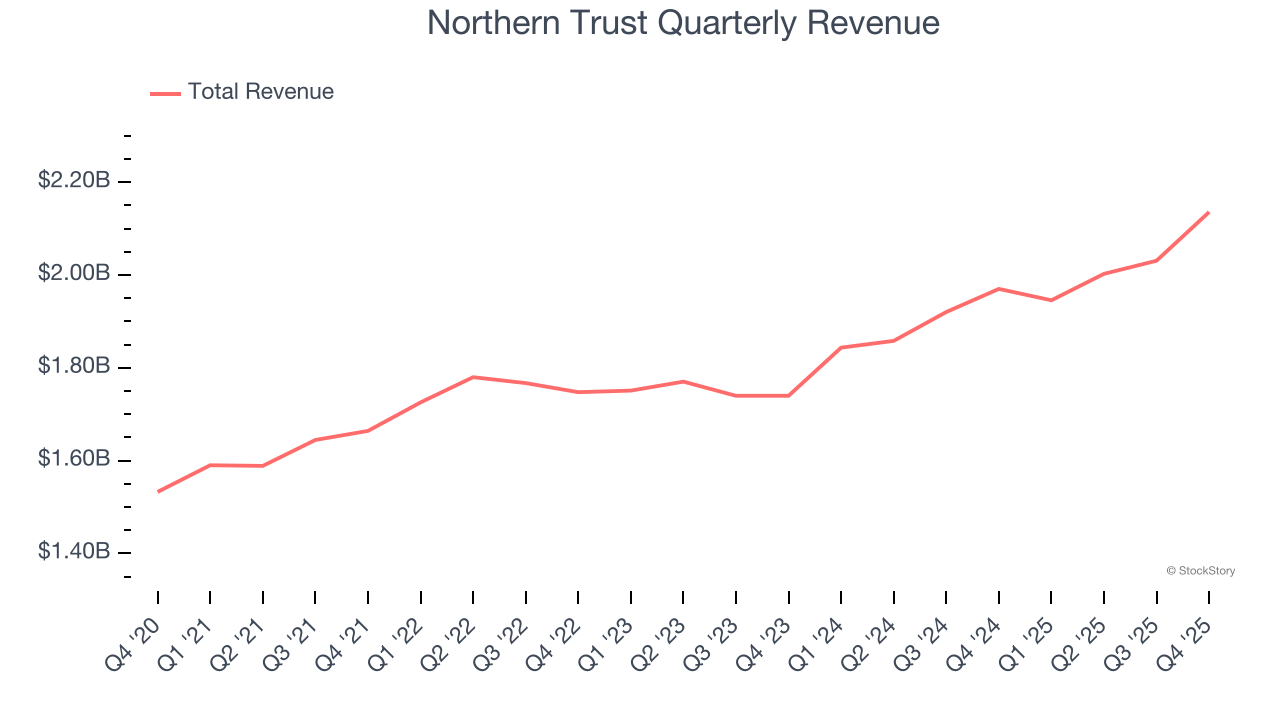

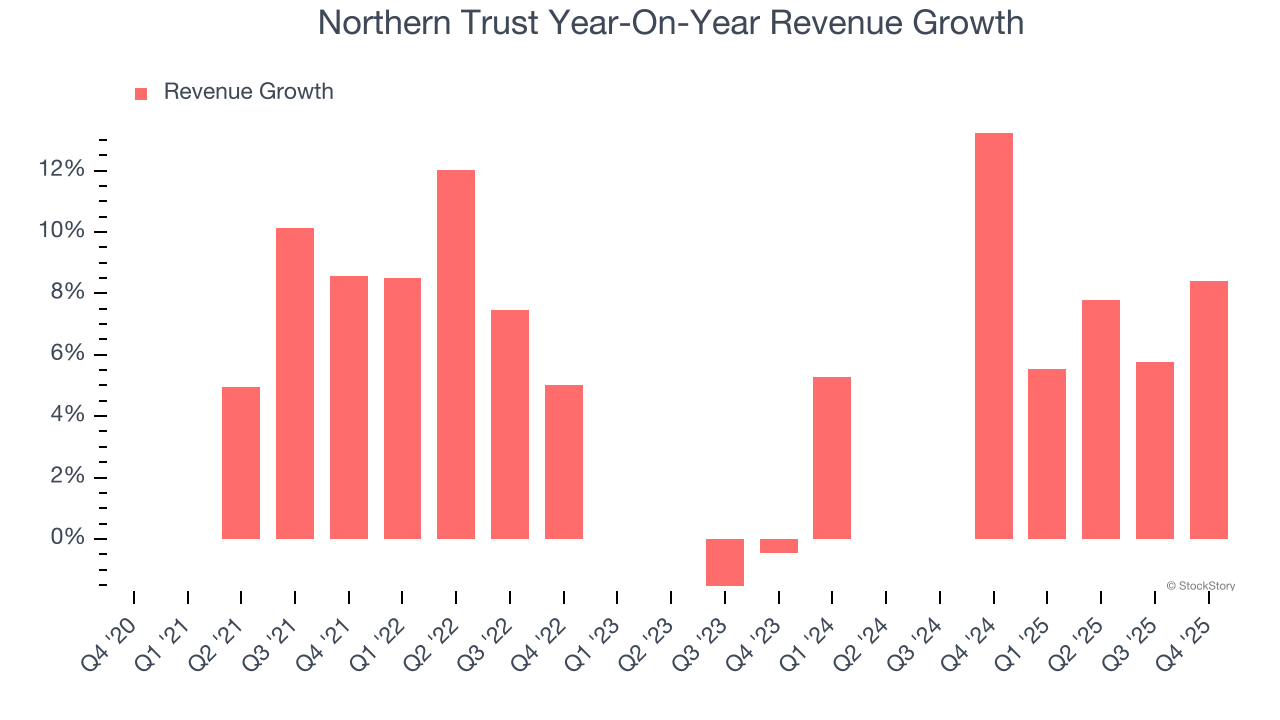

Financial services company Northern Trust (NASDAQ:NTRS) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 8.4% year on year to $2.14 billion. Its GAAP profit of $2.42 per share was 2.8% above analysts’ consensus estimates.

Is now the time to buy Northern Trust? Find out by accessing our full research report, it’s free.

Founded in 1889 during Chicago's post-Great Fire rebuilding boom, Northern Trust (NASDAQ:NTRS) provides wealth management, asset servicing, and banking solutions to corporations, institutions, families, and high-net-worth individuals globally.

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Northern Trust grew its revenue at a tepid 5.8% compounded annual growth rate. This was below our standard for the financials sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Northern Trust’s annualized revenue growth of 7.7% over the last two years is above its five-year trend, suggesting some bright spots.

This quarter, Northern Trust reported year-on-year revenue growth of 8.4%, and its $2.14 billion of revenue exceeded Wall Street’s estimates by 3.5%.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

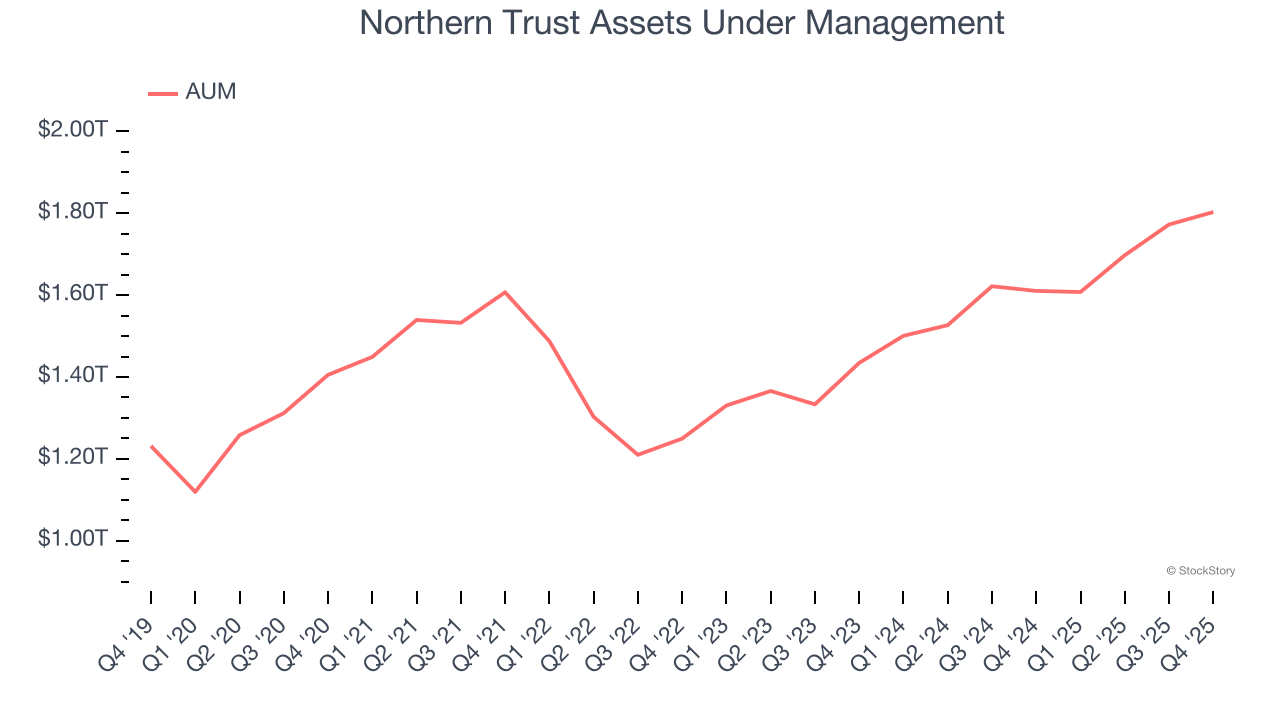

Assets Under Management (AUM) is the cornerstone of a financial firm's investment division, representing all client capital under its stewardship. Management fees on this AUM create reliable, recurring revenue that maintains stability even when investment performance struggles, though prolonged poor returns can eventually affect asset retention and growth.

Northern Trust’s AUM has grown at an annual rate of 6.2% over the last five years, slightly worse than the broader financials industry and mirrored its total revenue. When analyzing Northern Trust’s AUM over the last two years, we can see that growth accelerated to 12.2% annually. Fundraising or short-term investment performance were net contributors for the company over this shorter period since assets grew faster than total revenue. Keep in mind that asset growth can be erratic and seasonal, so we don't rely on it too heavily for our business quality analysis.

Northern Trust’s AUM punched in at $1.80 trillion this quarter, meeting analysts’ expectations. This print was 12% higher than the same quarter last year.

It was encouraging to see Northern Trust beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $144.09 immediately following the results.

So should you invest in Northern Trust right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-13 | |

| Jul-06 | |

| Jun-22 | |

| Jun-18 | |

| Jun-17 | |

| Jun-17 | |

| Jun-15 | |

| Jun-11 | |

| Jun-10 | |

| Jun-08 | |

| Jun-03 | |

| Jun-02 | |

| May-22 | |

| May-20 | |

| May-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite