|

|

|

|

|||||

|

|

|

The U.S. infrastructure and public-sector spending environment continues to support steady demand for engineering and technical consulting services, driven by grid modernization, energy transition initiatives and long-term government programs. Within this backdrop, Willdan Group, Inc. WLDN and Jacobs Solutions Inc. J have emerged as comparable engineering stocks benefiting from policy-backed investment trends and program-based work tied to public clients.

While both companies are exposed to long-duration infrastructure programs, the operating focus differs. Willdan is more concentrated on energy, utility and municipal consulting, with advisory work that supports recurring execution. Jacobs operates at a broader scale, with diversified exposure across transportation, water, energy and advanced facilities supported by multi-year government contracts. Furthermore, easing financial conditions following recent monetary policy shifts could provide an additional tailwind for infrastructure investment and project financing activity.

Let’s dive deep and closely compare the fundamentals of the two stocks to determine which one is a better investment now.

This California-based professional, technical and consulting service provider is seeing solid momentum as demand for energy transition and infrastructure modernization continues to rise. Willdan is benefiting from rising electricity load tied to data centers, electrification and grid upgrades. Activity across energy consulting, power engineering and program management remains healthy, supported by utilities, commercial customers and state and local governments. A growing pipeline and steady contract conversions are improving visibility as projects advance through planning and execution phases.

The company’s Energy segment, which represents the majority of revenues, continues to anchor performance. During the first nine months of 2025, contract revenues increased 20% year over year to $508 million, while net revenues rose 27% to $275 million. Growth was supported by strong execution across energy efficiency, power engineering and consulting programs. Long-term utility contracts, typically spanning three to five years, continue to provide recurring revenues and support workload stability as utilities respond to rising power demand.

However, a significant portion of activity is tied to public-sector budgets and regulated utility programs, where funding timing and regulatory processes can delay project starts. Rapid growth across data center and electrification-related work also increases execution complexity, requiring disciplined staffing and project selection to protect margins. Shifts in customer investment pacing could create short-term variability even with a solid pipeline in place.

Looking ahead, the company expects continued support from electricity load growth, infrastructure investment and expanding program scopes. The integration of recent power engineering capabilities and the steady conversion of consulting work into larger execution projects position Willdan for sustained growth. With improving visibility and exposure to long-duration energy programs, the company appears well-positioned as demand trends extend in 2026.

This Texas-based professional, technical and construction services provider is benefiting from steady demand across infrastructure, advanced facilities and public-sector programs. Jacobs continues to see support from transportation, water, energy and life sciences markets, where long-duration programs and complex project requirements favor experienced service providers. Broad exposure to government and regulated clients provides stability, while diversified end markets help balance project timing across regions and sectors.

At the end of the fourth quarter of fiscal 2025, consolidated backlog reached a record $23.1 billion, reflecting a 5.6% year-over-year increase. Strong booking activity supported a trailing 12-month book-to-bill ratio of 1.1x, while gross profit in backlog increased 13% year over year. This backlog mix provides improved visibility across multi-year programs and supports execution as large transportation, water and advanced facility projects move through development and delivery phases.

However, portions of the environmental business experienced softer demand, particularly in the United States, as regulatory uncertainty and funding transitions slowed customer decision-making. Project timing can also be affected by permitting processes and public-sector budget pacing, which may lead to variability in quarterly performance even as overall demand trends remain supportive.

Looking ahead, the company appears well-positioned for sustained growth in 2026. Continued public and private investment across infrastructure and advanced facilities supports backlog conversion, while strategic initiatives enhance long-term competitiveness. The company’s partnership with NVIDIA strengthens digital and AI-enabled delivery capabilities, and the full acquisition of PA Consulting expands exposure to higher-value advisory work. Combined with a record backlog and improving mix, these factors support a favorable long-term outlook.

As witnessed from the chart below, in the past six months, Willdan's share price performance stands above Jacobs.

Considering valuation, Willdan is currently trading at a premium compared with Jacobs on a forward 12-month price-to-earnings (P/E) ratio basis.

Willdan's earnings estimates for 2026 have remained unchanged in the past 60 days at $4.53 per share. This indicates expected earnings growth of 9.6% year over year on projected revenue growth of 4.8%.

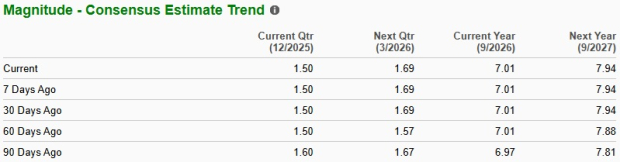

Jacobs' earnings estimates for fiscal 2026 have remained unchanged in the past 60 days at $7.01 per share. This indicates expected earnings growth of 14.5% year over year on projected revenue growth of 7.9%.

Willdan and Jacobs both benefit from sustained U.S. infrastructure and public-sector spending, but the near-term setups differ. WLDN is supported by rising electricity load, expanding energy and power engineering activity, and improving visibility tied to utility programs and data center-related work. Jacobs offers broader diversification across transportation, water, energy and advanced facilities, backed by a record backlog, but faces softer conditions in parts of the environmental business and greater variability tied to public-sector funding and project timing.

With Willdan carrying a Zacks Rank #3 (Hold) and Jacobs rated with a Zacks Rank #4 (Sell), the former’s steadier demand drivers and comparatively more favorable near-term outlook make it the more compelling engineering stock at this time.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-21 | |

| Jul-21 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-07 | |

| Jul-06 | |

| Jul-02 | |

| Jun-30 | |

| Jun-22 | |

| Jun-20 | |

| Jun-15 | |

| Jun-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite