|

|

|

|

|||||

|

|

|

Inspire Medical Systems INSP appears positioned for solid growth over the next few quarters as it navigates a significant product transition. Management highlighted strong clinical traction for Inspire V, clearer reimbursement pathways, and tight cost discipline, while also flagging short-term pressures from inventory conversion, evolving GLP-1 usage and heightened competitive and operational challenges.

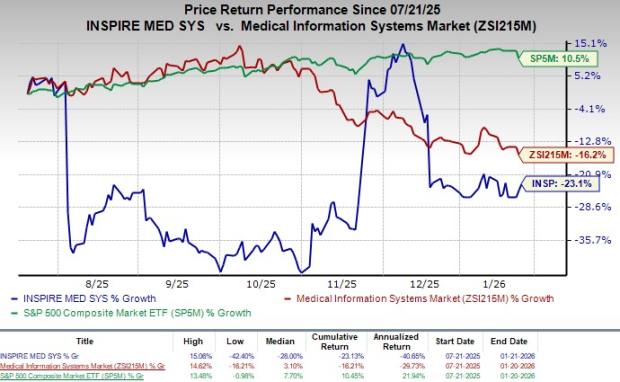

Shares of this Zacks Rank #3 (Hold) company have lost 23.1% over the past six months compared with the industry’s 16.2% decline. The S&P 500 Index has increased 10.5% in the same time frame.

Inspire Medical, a medical technology company focused on the development and commercialization of innovative, minimally invasive solutions for patients with obstructive sleep apnea, has a market capitalization of $2.74 billion. The company projects 39.1% earnings decline for the fourth quarter of 2025. However, earnings are expected to return to growth in 2026.

The company’s earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 164.19%.

Expanding Patient Funnel and Disciplined Execution: Management noted that rising GLP-1 adoption is driving more patients into sleep clinics, effectively broadening the funnel for Inspire Medical rather than cannibalizing demand. Sleep specialists are increasingly treating GLP-1 patients in parallel with CPAP, which can later translate into Inspire referrals as adherence issues arise or patients qualify under BMI criteria.

At the same time, Inspire Medical showed solid operational execution, posting earnings outperformance through margin improvement and disciplined expense management even with elevated marketing investment. Healthy cash flow, ongoing share buybacks, and more focused territory oversight further support the company’s ability to scale efficiently as procedure volumes rebound.

Strong Inspire V Clinical Performance and Adoption Momentum: The Inspire V launch is emerging as a structural growth driver. Management cited compelling clinical data, including reduced surgical times, high nightly usage and strong synchronization with patient breathing, reinforcing superior outcomes versus prior generations. With physician training nearing completion and contracting more than 90%, the adoption of Inspire V has accelerated, reaching more than 75% of implanting centers. Importantly, early evidence shows higher utilization and efficiency at converted centers, with surgeons able to perform more implants per day. This combination of better outcomes, easier implantation, and higher throughput underpins sustained volume growth.

Favorable Reimbursement Outlook Supports Economics: Reimbursement dynamics are turning increasingly favorable. CMS has finalized an 11% increase to the physician fee schedule for CPT 64568 starting January 2026, and proposed hikes to hospital outpatient and ASC reimbursement rates would further enhance site-of-care economics. Coverage already exceeds 90% of insured lives, including Medicare beneficiaries.

Collectively, these developments should help close longstanding reimbursement gaps around Inspire systems, easing adoption for hospitals. Greater reimbursement clarity enhances the value proposition of Inspire V, improves profitability at the center level, and is likely to support faster conversion and higher utilization over time.

GLP-1 Trialing and Timing Uncertainty: Although management views GLP-1 therapies as complementary over the long term, near-term trialing introduces uncertainty around procedure timing. Patients may delay surgical intervention while attempting pharmacologic weight loss, potentially dampening short-term volume growth. Management’s early-2026 growth outlook reflects prudence around this dynamic. While increased clinic visits and eventual CPAP noncompliance could ultimately benefit Inspire Medical, the pace at which GLP-1 patients convert to hypoglossal nerve stimulation remains difficult to predict, creating variability in near-term demand visibility.

Margin Pressure From Elevated OpEx and Competition: Despite robust gross margins, operating leverage is still limited by higher operating expenses, led by patient marketing and launch-related spending. Operating costs continue to grow faster than revenues on a year-over-year basis, and one-time items also pressured reported profitability. Management also pointed to early signs of competitive activity, though still modest, along with ongoing pricing and site-of-care dynamics at select centers.

Going forward, maintaining margin expansion will hinge on striking the right balance between continued investment in growth and incremental efficiency improvements, particularly as revenue growth settles into a low double-digit range.

Inspire Medical is witnessing a stable estimate revision trend for 2025. In the past 30 days, the Zacks Consensus Estimate for earnings is pegged at $1.60 per share.

The Zacks Consensus Estimate for fourth-quarter 2025 revenues and loss per share is pegged at $269 million and 70 cents, respectively.

Some better-ranked stocks in the broader medical space are IDEXX Laboratories IDXX, Boston Scientific BSX and STERIS STE. Each stock presently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Estimates for IDEXX’s 2025 earnings per share (EPS) have remained constant at $12.93 in the past 30 days. Shares of the company have risen 12.6% in the past year compared with the industry’s 11.1% growth. IDXX’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 7.1%. In the last reported quarter, it delivered an earnings surprise of 8.3%.

Boston Scientific shares have gained 2.9% in the past year. Estimates for the company’s 2025 EPS have remained constant at $3.04 in the past 30 days. BSX’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 7.4%. In the last reported quarter, it posted an earnings surprise of 5.6%.

STERIS shares have risen 9.1% in the past year. Estimates for the company’s 2025 EPS have increased by 2 cents to $10.23 in the past 30 days. STE’s earnings topped estimates in three of the trailing four quarters and matched on one occasion, delivering an average surprise of 2.6%. In the last reported quarter, it posted an earnings surprise of 2.6%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-21 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-15 | |

| Jul-09 | |

| Jul-09 | |

| Jul-07 | |

| Jul-06 | |

| Jul-06 | |

| Jul-06 | |

| Jul-02 | |

| Jul-01 | |

| Jun-29 | |

| Jun-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite