|

|

|

|

|||||

|

|

|

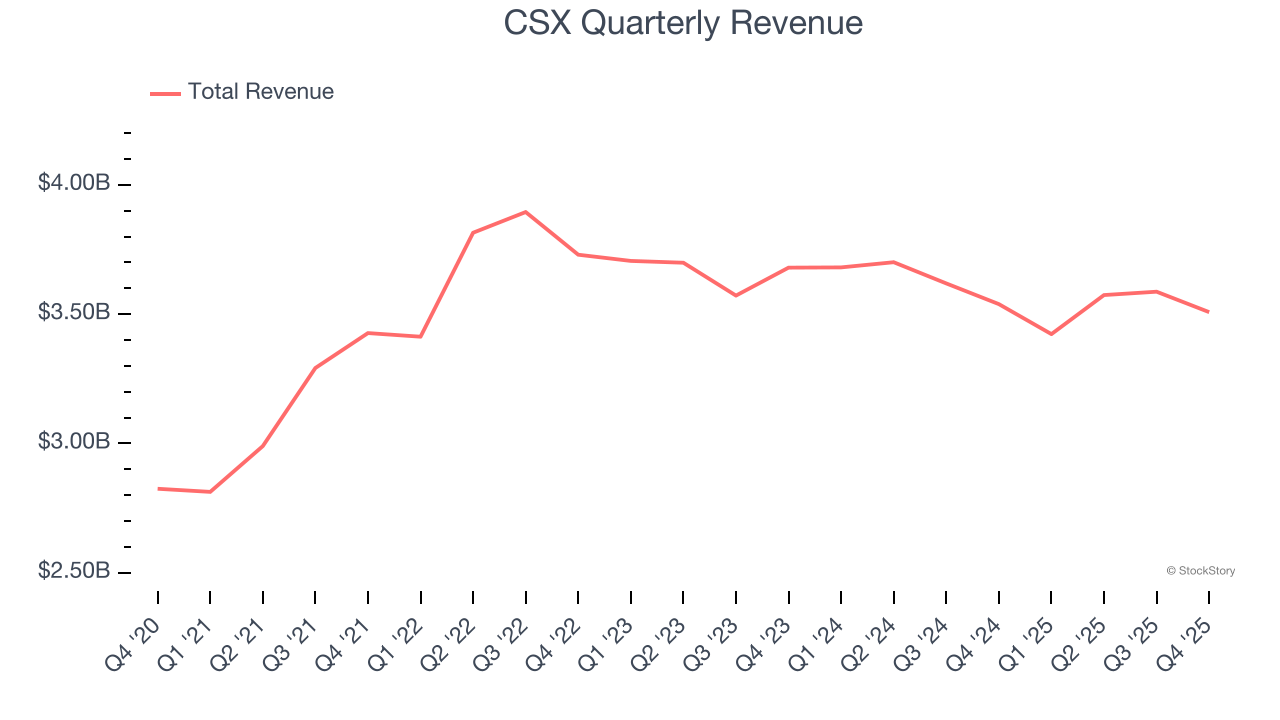

Freight rail services provider CSX (NASDAQ:CSX) fell short of the markets revenue expectations in Q4 CY2025, with sales flat year on year at $3.51 billion. Its non-GAAP profit of $0.39 per share was 5.3% below analysts’ consensus estimates.

Is now the time to buy CSX? Find out by accessing our full research report, it’s free.

Established as part of the Chessie System and Seaboard Coast Line Industries merger, CSX (NASDAQ:CSX) is a transportation company specializing in freight rail services.

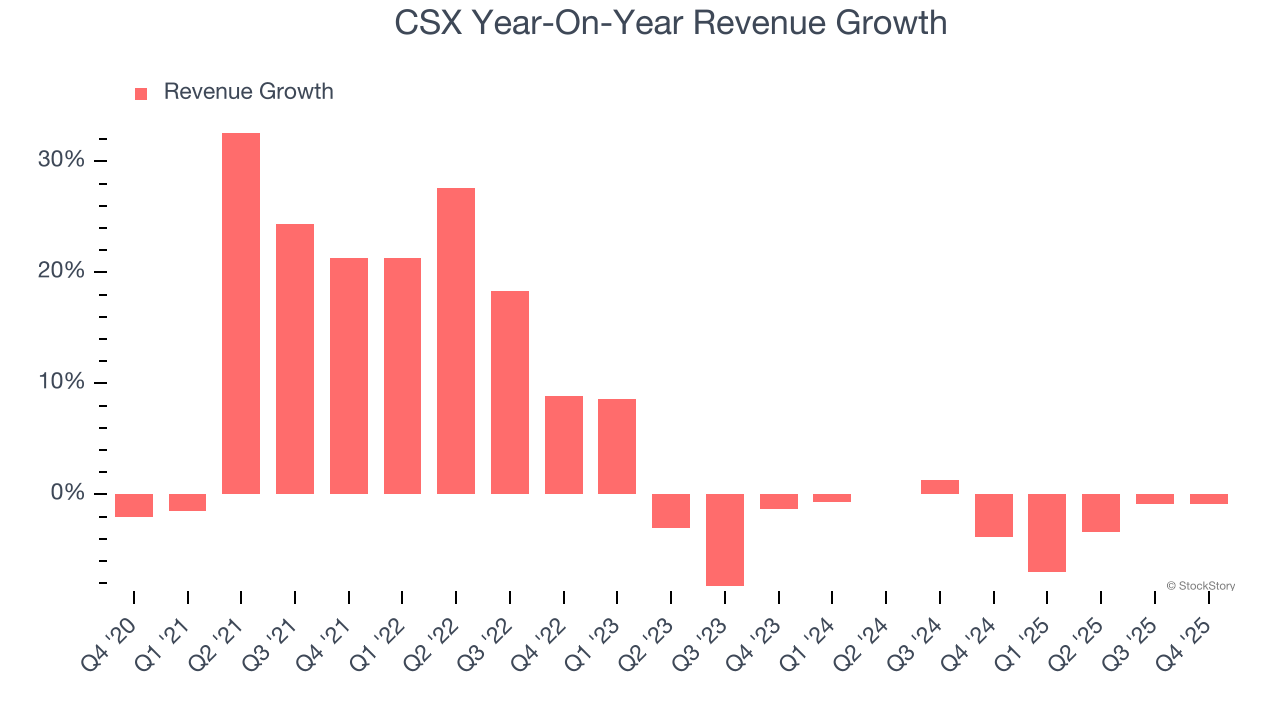

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, CSX grew its sales at a tepid 5.9% compounded annual growth rate. This was below our standard for the industrials sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. CSX’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.9% annually. CSX isn’t alone in its struggles as the Rail Transportation industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

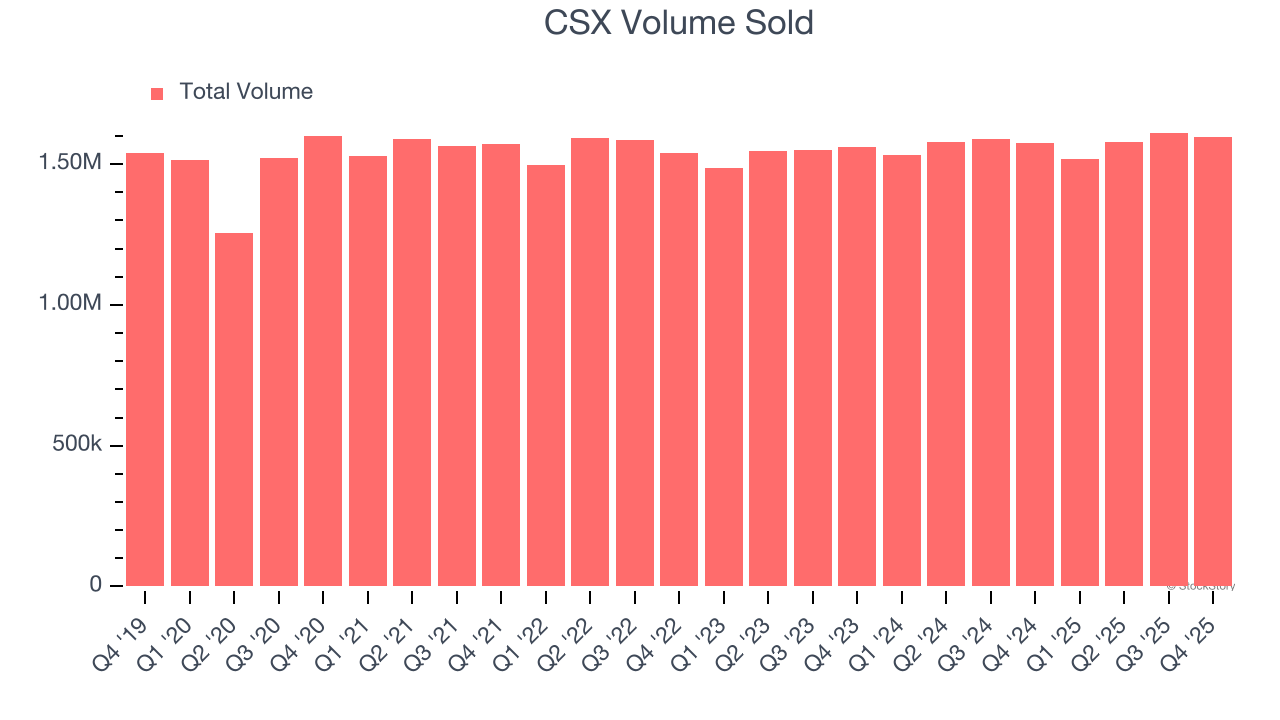

CSX also reports its number of units sold, which reached 1.6 million in the latest quarter. Over the last two years, CSX’s units sold averaged 1.3% year-on-year growth. Because this number is better than its revenue growth, we can see the company’s average selling price decreased.

This quarter, CSX missed Wall Street’s estimates and reported a rather uninspiring 0.9% year-on-year revenue decline, generating $3.51 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 4% over the next 12 months. Although this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

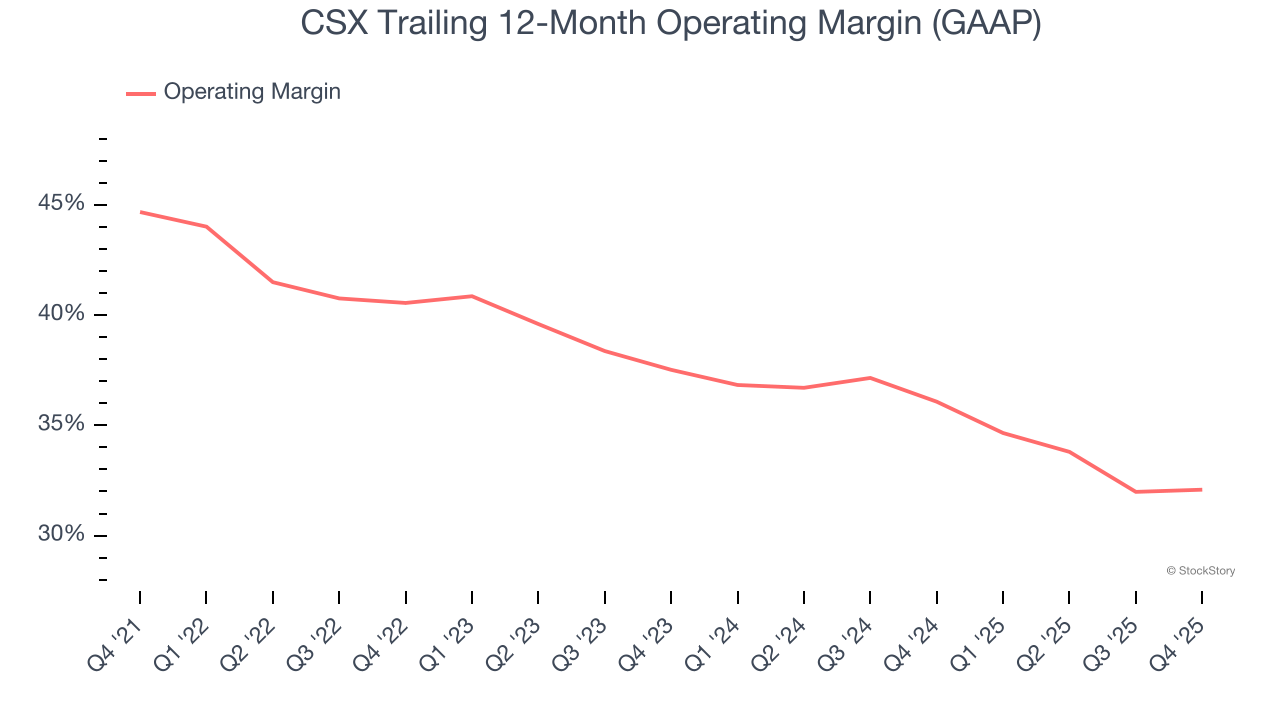

CSX has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 38%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, CSX’s operating margin decreased by 12.6 percentage points over the last five years. Many Rail Transportation companies also saw their margins fall (along with revenue, as mentioned above) because the cycle turned in the wrong direction. We hope CSX can emerge from this a stronger company, as the silver lining of a downturn is that market share can be won and efficiencies found.

In Q4, CSX generated an operating margin profit margin of 31.6%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

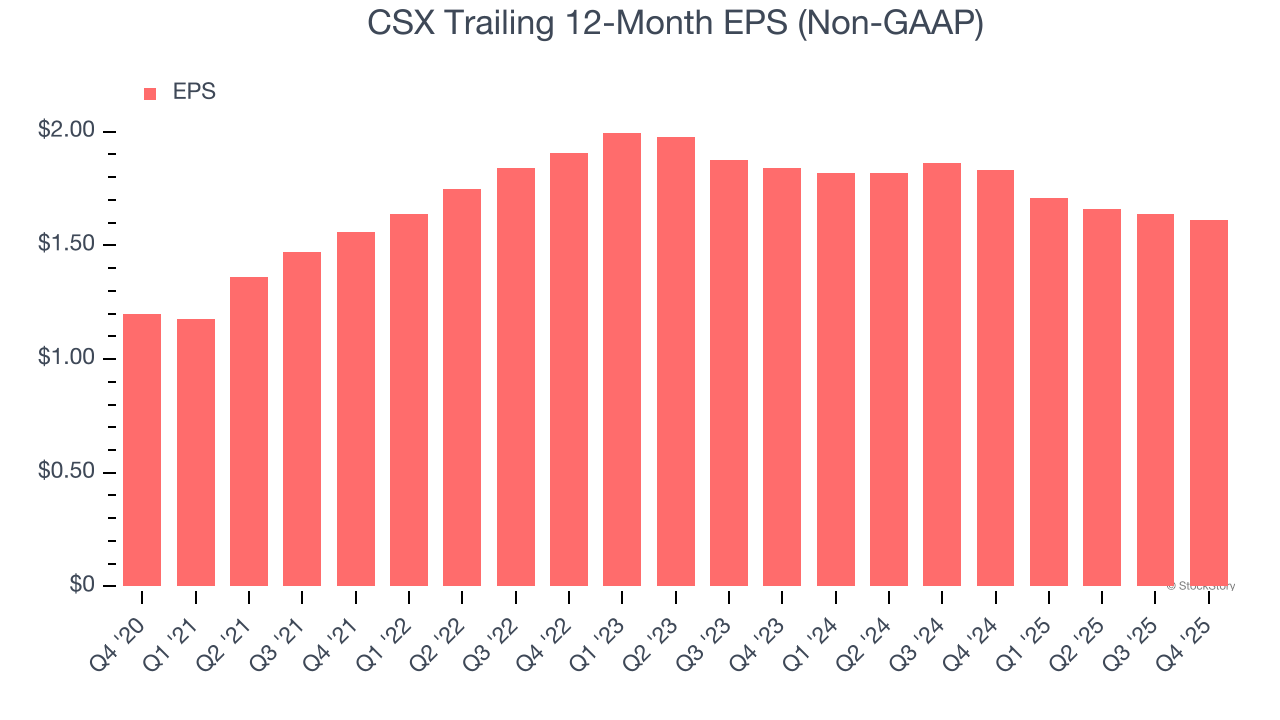

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

CSX’s unimpressive 6.1% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

CSX’s two-year annual EPS declines of 6.5% were bad and lower than its two-year revenue losses.

We can take a deeper look into CSX’s earnings to better understand the drivers of its performance. While we mentioned earlier that CSX’s operating margin was flat this quarter, a two-year view shows its margin has declined. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, CSX reported adjusted EPS of $0.39, down from $0.42 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects CSX’s full-year EPS of $1.61 to grow 16.2%.

We struggled to find many positives in these results. Its EBITDA missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded up 4.2% to $37.51 immediately following the results.

Big picture, is CSX a buy here and now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-13 | |

| Jul-09 | |

| Jul-01 | |

| Jun-22 | |

| Jun-18 | |

| Jun-08 | |

| May-28 | |

| May-12 | |

| May-06 | |

| May-06 | |

| May-05 | |

| May-04 | |

| May-04 | |

| Apr-24 | |

| Apr-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite