|

|

|

|

|||||

|

|

|

Carrier Global has gotten torched over the last six months - since July 2025, its stock price has dropped 28.6% to $57.21 per share. This might have investors contemplating their next move.

Is now the time to buy Carrier Global, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Even though the stock has become cheaper, we're cautious about Carrier Global. Here are three reasons we avoid CARR and a stock we'd rather own.

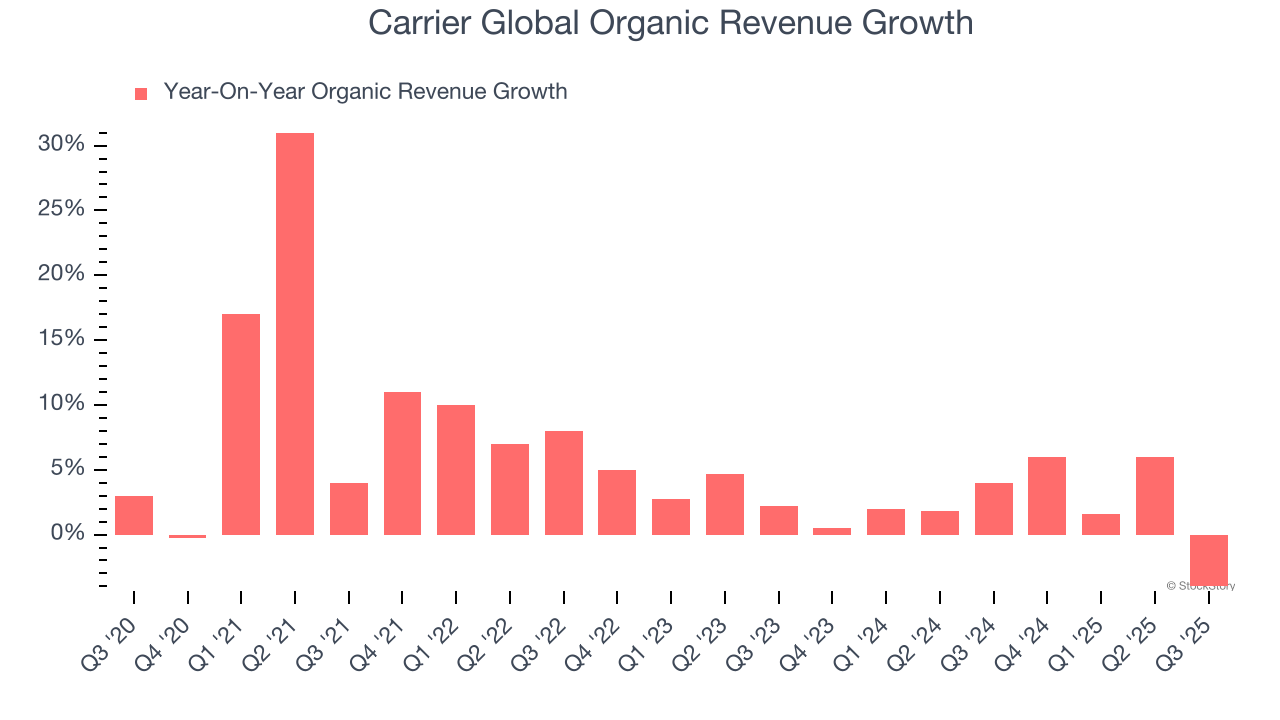

In addition to reported revenue, organic revenue is a useful data point for analyzing HVAC and Water Systems companies. This metric gives visibility into Carrier Global’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Carrier Global’s organic revenue averaged 2.2% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Carrier Global’s revenue to stall, a deceleration versus its 4.9% annualized growth for the past five years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Carrier Global’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Carrier Global falls short of our quality standards. After the recent drawdown, the stock trades at 21.3× forward P/E (or $57.21 per share). This valuation multiple is fair, but we don’t have much confidence in the company. There are more exciting stocks to buy at the moment. We’d suggest looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Aug-03 | |

| Aug-03 | |

| Jul-30 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-24 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite