|

|

|

|

|||||

|

|

|

Valero Energy Corporation VLO is set to report fourth-quarter 2025 results on Jan. 29, before the opening bell.

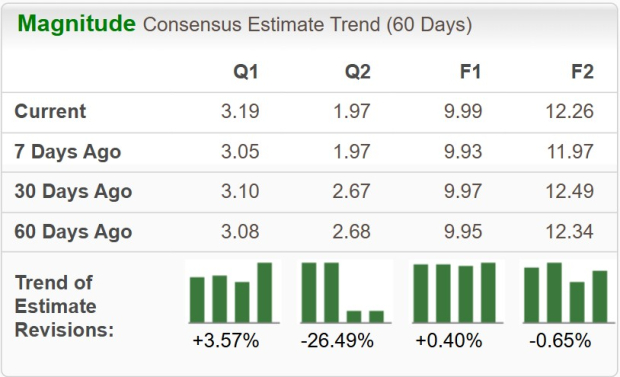

The Zacks Consensus Estimate for fourth-quarter earnings is pegged at $3.19 per share, implying an improvement of 398.4% from the year-ago reported number. VLO has witnessed four upward and two downward earnings estimate revisions over the past 30 days. The Zacks Consensus Estimate for fourth-quarter revenues is currently pegged at $28.9 billion, suggesting a 6% fall from the year-ago actuals.

VLO beat the consensus estimate for earnings in each of the trailing four quarters, with the average surprise being 138.8%. This is depicted in the graph below:

Our proven model does not predict an earnings beat for VLO this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the chances of an earnings beat. That is not the case here, as you will see below.

The company has an Earnings ESP of -2.90% and it currently carries a Zacks Rank #3.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Valero Energy is expected to have witnessed stable performance in the fourth quarter, owing to strong refining margins and resilient demand for refined products during the period. Per the data from the U.S. Energy Information Administration, the West Texas Intermediate spot crude price averaged $59.64 per barrel compared with $70.74 per barrel in the prior-year quarter. Lower crude prices imply cheaper feedstock for Valero’s refining operations, which likely supported refining gains. These factors are anticipated to have aided VLO’s profitability by reducing input costs.

However, the company is expected to have faced considerable weakness in the Renewable Diesel segment due to a weaker market environment. Furthermore, it will witness higher depreciation and amortization expenses associated with the closing of the Benecia Refinery, which is expected to have negatively impacted earnings.

These factors are likely to have affected demand and pricing dynamics, potentially hampering the company’s quarterly performance.

VLO’s stock has soared 32.4% over the past year compared with the 16% rise of the composite stocks belonging to the industry. Phillips 66 PSX and Par Pacific Holdings PARR, two other leading refining players, have gained 15% and 100.1%, respectively.

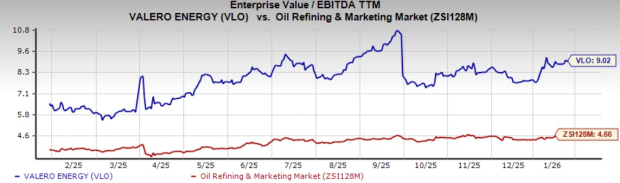

VLO appears relatively overvalued, at a trailing 12-month enterprise value to EBITDA (EV/EBITDA) of 9.02X, above the broader industry average of 4.66X, implying that the stock is currently trading at a premium.

Valero Energy is a leading refining player with a robust network of 15 refineries located across the United States, Canada and the Caribbean. The company has a combined throughput capacity of 3.2 million barrels per day, which distinguishes it from other independent refiners. Notably, VLO’s refineries have the operational flexibility to process various kinds of feedstock, including heavy sour, medium/light sour and sweet crude.

Valero boasts a strong financial and liquidity position, with a low debt-to-capitalization ratio of 18%, as of Sept. 30, 2025. The company utilizes its excess free cash flow toward share buybacks. However, the refining industry is inherently cyclical and volatile. Refining margins and crack spreads depend largely on crude oil prices and the overall demand for refined petroleum products, which fluctuate across market cycles. Furthermore, weakness across secondary products markets like naphtha and propylene stands to impact the refining player in the near term. (See the Zacks Earnings Calendar to stay ahead of market-making news.)

Phillips 66 owns an extensive and highly complex refinery network that can process a variety of feedstocks. Phillips 66 operates 11 refineries across the United States and Europe. The company recorded a 99% crude utilization rate in the third quarter, the highest since 2018.

Par Pacific Holdings is a Houston-based refining player with a combined refining capacity of 219,000 barrels per day, and operations spread across Hawaii and the Pacific Northwest. The company also operates 119 retail locations along with a logistics business segment.

Along with VLO, PSX and PARR are expected to gain from strong refining margins. In the United States, refining margins have risen markedly in 2025, driven by tightened supply due to refinery maintenance and outages, as well as resilient demand for refined fuels. The softening of crude prices is likely to have supported the macro refining environment in the fourth quarter, thereby aiding their bottom-line profitability.

Considering the backdrop, it might be wise for investors to wait for a more opportune moment to own VLO, as the company is currently somewhat overvalued.

PSX and PARR carry a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-18 | |

| Jul-17 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite