|

|

|

|

|||||

|

|

|

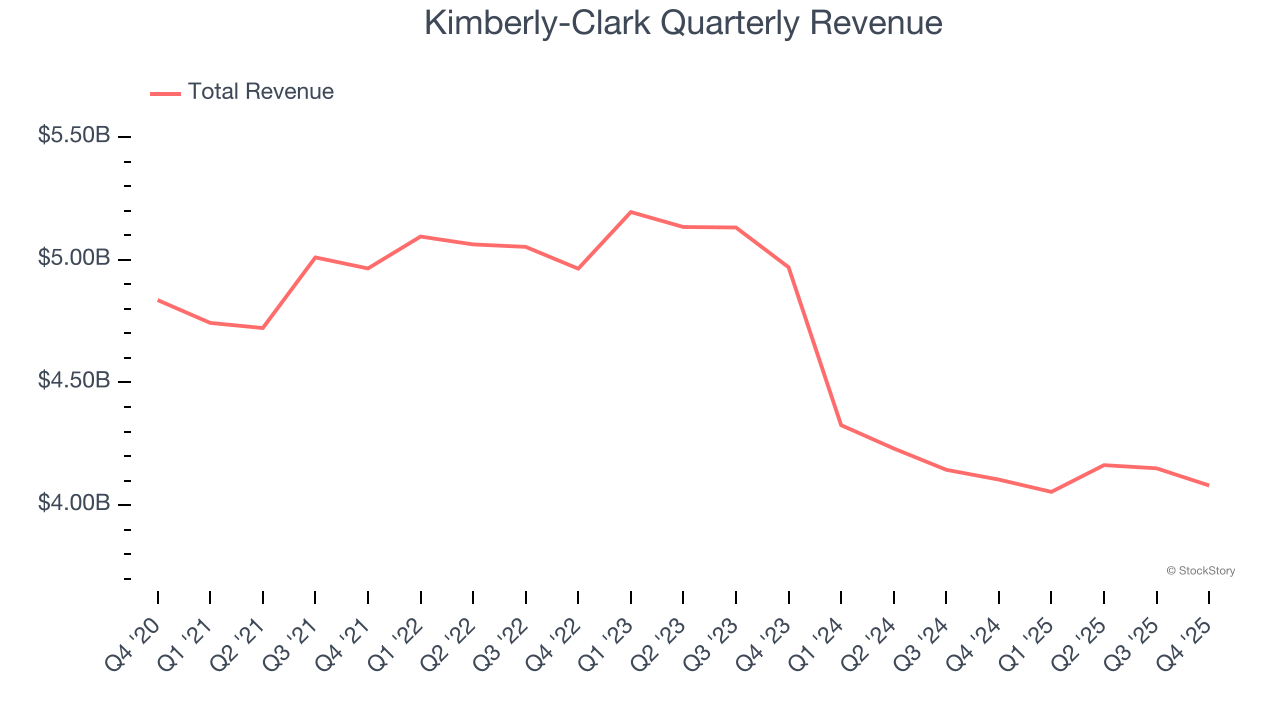

Household products company Kimberly-Clark (NYSE:KMB) met Wall Streets revenue expectations in Q4 CY2025, but sales were flat year on year at $4.08 billion. Its non-GAAP profit of $1.86 per share was 2.7% above analysts’ consensus estimates.

Is now the time to buy Kimberly-Clark? Find out by accessing our full research report, it’s free.

"In 2025, we accelerated the largest transformation in Kimberly-Clark's more than 150-year history, delivering results that underscore the strength of our business and serve as a springboard for enhanced growth and continued outperformance in 2026," said Kimberly-Clark Chairman and CEO Mike Hsu.

Originally founded as a Wisconsin paper mill in 1872, Kimberly-Clark (NYSE:KMB) is now a household products powerhouse known for personal care and tissue products.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $16.45 billion in revenue over the past 12 months, Kimberly-Clark is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. To expand meaningfully, Kimberly-Clark likely needs to tweak its prices, innovate with new products, or enter new markets.

As you can see below, Kimberly-Clark struggled to generate demand over the last three years. Its sales dropped by 6.6% annually despite consumers buying more of its products. We’ll explore what this means in the "Volume Growth" section.

This quarter, Kimberly-Clark’s $4.08 billion of revenue was flat year on year and in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 2.7% over the next 12 months. Although this projection indicates its newer products will spur better top-line performance, it is still below the sector average.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

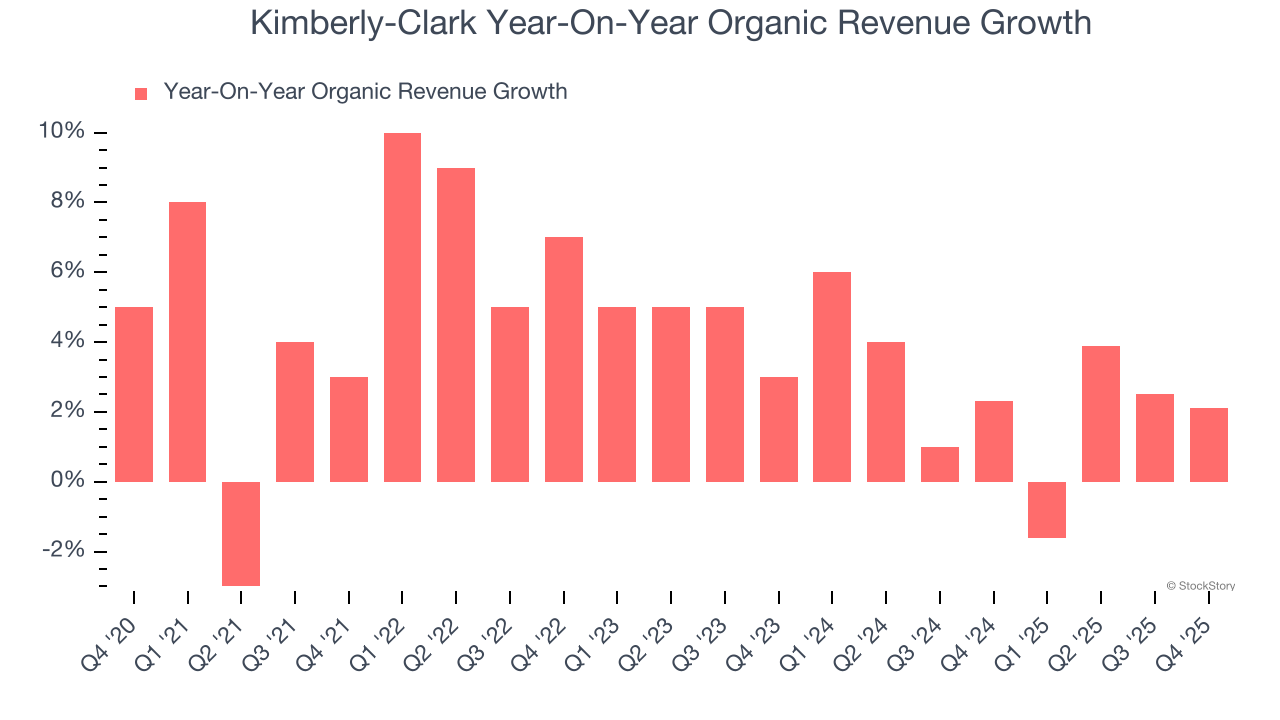

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Kimberly-Clark’s products has generally risen over the last two years but lagged behind the broader sector. On average, the company’s organic sales have grown by 2.5% year on year.

In the latest quarter, Kimberly-Clark’s organic sales rose by 2.1% year on year. This performance was more or less in line with its historical levels.

Organic revenue growth and total revenue were both in line, but EPS managed to beat. Overall, this quarter wasn't perfect, but it was solid. The stock traded up 1.1% to $102.07 immediately following the results.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

| 11 hours | |

| May-28 | |

| May-26 | |

| May-19 | |

| May-14 | |

| May-14 | |

| May-11 | |

| May-06 | |

| May-06 | |

| Apr-29 | |

| Apr-29 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite