|

|

|

|

|||||

|

|

|

Mission Produce, Inc.’s AVO recent 10% revenue growth marks a notable rebound in a business long exposed to pricing volatility and supply-driven swings. While headline growth in produce can often be misleading — frequently reflecting pricing rather than underlying strength — this uptick invites a deeper look at what is driving performance. The key question for investors is whether this improvement signals the start of a more durable, multi-segment growth story or simply a favorable turn in the cycle.

Beneath the surface, Mission Produce’s growth appears increasingly diversified. Stronger volumes in its core avocado business, supported by global sourcing and improved supply consistency, have played a central role. At the same time, contributions from adjacent segments, such as blueberries and mangoes, are becoming more meaningful. These categories benefit from rising global demand for healthy snacks and allow Mission Produce to leverage its vertically integrated platform — farming, packing, ripening and distribution — across more than one fruit, reducing reliance on any single crop or region.

Still, sustaining multi-segment growth will depend on execution as much as market conditions. Newer categories carry higher costs and margin variability, while pricing pressure remains an ever-present risk in fresh produce. However, Mission Produce’s emphasis on volume growth, per-unit margin discipline and operational efficiency suggests a more balanced growth profile is taking shape. If the company can continue scaling its non-avocado segments while maintaining profitability, the recent revenue increase may represent more than a one-off — potentially signaling the early stages of a broader, more resilient growth trajectory.

Both Corteva, Inc. CTVA and Dole plc DOLE are increasingly driving revenues through diversified, multi-segment strategies that emphasize innovation, portfolio balance and adaptability, reducing reliance on any single product, market or pricing lever.

For Corteva, revenue growth is increasingly driven by a multi-segment, innovation-led strategy rather than broad-based volume expansion. The company benefits from a balanced portfolio spanning seed genetics, crop protection and biologicals, allowing growth in one segment to offset softness in another. Demand for premium seeds and precision agriculture solutions continues to support pricing and mix, while targeted innovation helps deepen penetration across both row crops and specialty markets. This diversified approach positions Corteva for more resilient, cycle-aware growth rather than dependence on any single crop or geography.

Dole’s growth story is similarly rooted in diversification, with revenues supported by multiple fresh-produce categories including bananas, pineapples, berries and value-added products. Rather than relying solely on pricing, Dole is leveraging volume growth, improved logistics efficiency and expanded offerings to drive performance across segments. Investments in supply-chain optimization and branded, higher-margin products are helping balance volatility in individual categories. As a result, Dole’s revenue momentum increasingly reflects a broader, multi-segment platform that can adapt to shifting consumer demand and market conditions.

Shares of Mission Produce have gained 12.1% in the last six months compared with the industry’s growth of 0.1%.

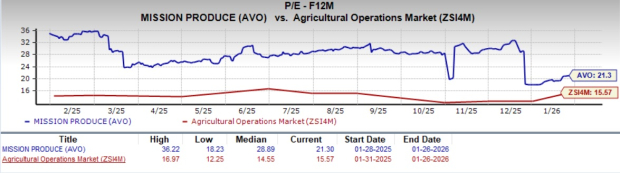

From a valuation standpoint, AVO trades at a forward price-to-earnings ratio of 21.30X, significantly above the industry’s average of 15.57X.

The Zacks Consensus Estimate for AVO’s fiscal 2026 earnings suggests a year-over-year decline of 10.13%, while that for fiscal 2027 indicates growth of 4.23%. The company’s EPS estimates for fiscal 2026 and 2027 have remained stable in the past seven days.

AVO stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-24 | |

| Jul-23 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-17 | |

| Jul-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite