|

|

|

|

|||||

|

|

|

PepsiCo, Inc. PEP has increasingly relied on pricing as a key lever to drive revenue growth in a challenging consumer environment marked by inflation and value sensitivity. In the past several quarters, higher prices and a favorable mix have helped offset rising input costs and protect margins, even as demand patterns shifted. While this strategy has supported the top line and profitability, it has also raised concerns about whether sustained pricing actions could eventually weigh on volumes, particularly in North America, where consumers are becoming more cautious and promotional intensity is rising.

In recent quarters, PepsiCo’s organic revenue growth has been driven more by pricing than by volume, with certain categories experiencing softer unit demand. Management has acknowledged pressure in parts of the packaged food business, especially within PepsiCo Foods North America, where volumes have been challenged by constrained consumer budgets and tougher comparisons. Although initiatives like price-pack architecture and permissible product innovation are helping improve value perception, the risk remains that continued price increases could push price-sensitive shoppers toward private labels or smaller pack sizes, limiting volume recovery.

Looking ahead, PepsiCo’s ability to balance pricing power with volume stability will be critical. The company is sharpening its revenue management strategy by offering more accessible price points, optimizing promotions and expanding value-oriented packs to protect demand. At the same time, investments in innovation, productivity and operational efficiency are intended to reduce reliance on pricing alone for growth. Whether PepsiCo can maintain this balance will determine if pricing remains a strength or becomes a growing risk to long-term volume and market share.

Both The Coca-Cola Company KO and Keurig Dr Pepper Inc. KDP are leaning on pricing to protect revenues and margins amid inflation, but their long-term performance hinges on how effectively they balance price realization with affordability to safeguard volumes.

Coca-Cola has also leaned on pricing power to drive revenue growth, benefiting from strong brand equity and a favorable mix, particularly in sparkling beverages and premium offerings. While pricing actions have supported margins, the company has been careful to manage volumes through smaller pack sizes, expanded zero-sugar options and targeted promotions. Coca-Cola’s global scale and diversified portfolio help cushion volume risk, though prolonged pricing pressure in value-sensitive markets could still challenge demand. Maintaining the right balance between price realization and affordability remains key to sustaining long-term volume growth.

Keurig Dr Pepper has relied on pricing to offset cost inflation, but volume sensitivity remains a key consideration, especially in its packaged beverage and coffee segments. While pricing and mix have supported revenues, higher shelf prices have weighed on volumes in certain categories. KDP is responding by emphasizing productivity savings, innovation and value-oriented offerings to limit further volume erosion. The company’s ability to balance price increases with affordability, particularly in cold beverages and coffee pods, will be critical to sustaining demand and avoiding longer-term volume risks.

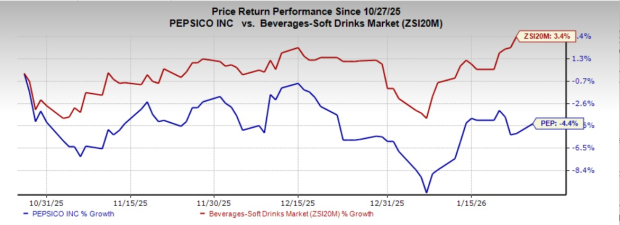

Shares of PepsiCo have lost 4.4% in the past three months against the industry’s growth of 3.4%.

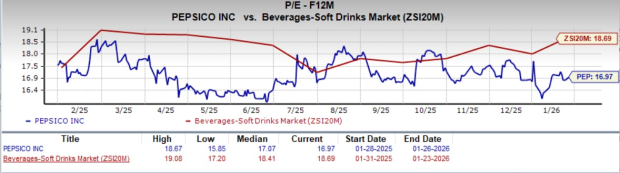

From a valuation standpoint, PEP trades at a forward price-to-earnings ratio of 16.97X, slightly below the industry’s average of 18.69X.

The Zacks Consensus Estimate for PEP’s 2025 earnings implies a year-over-year decline of 0.5%, whereas the same for 2026 earnings indicates growth of 5.4%. The company’s EPS estimates for 2025 and 2026 have remained stable in the past seven days.

PEP stock currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jun-08 | |

| Jun-08 | |

| Jun-08 | |

| Jun-07 | |

| Jun-07 | |

| Jun-05 | |

| Jun-05 | |

| Jun-05 | |

| Jun-05 | |

| Jun-04 | |

| Jun-04 | |

| Jun-04 | |

| Jun-04 | |

| Jun-04 | |

| Jun-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite