|

|

|

|

|||||

|

|

|

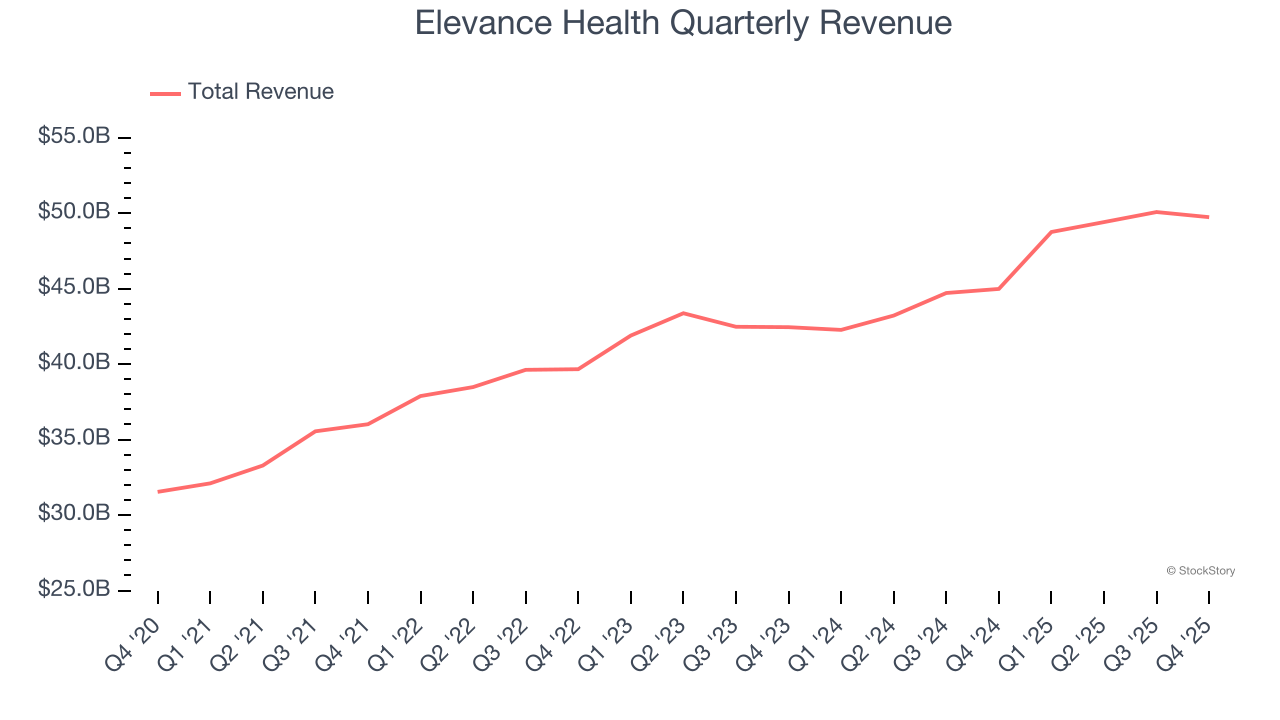

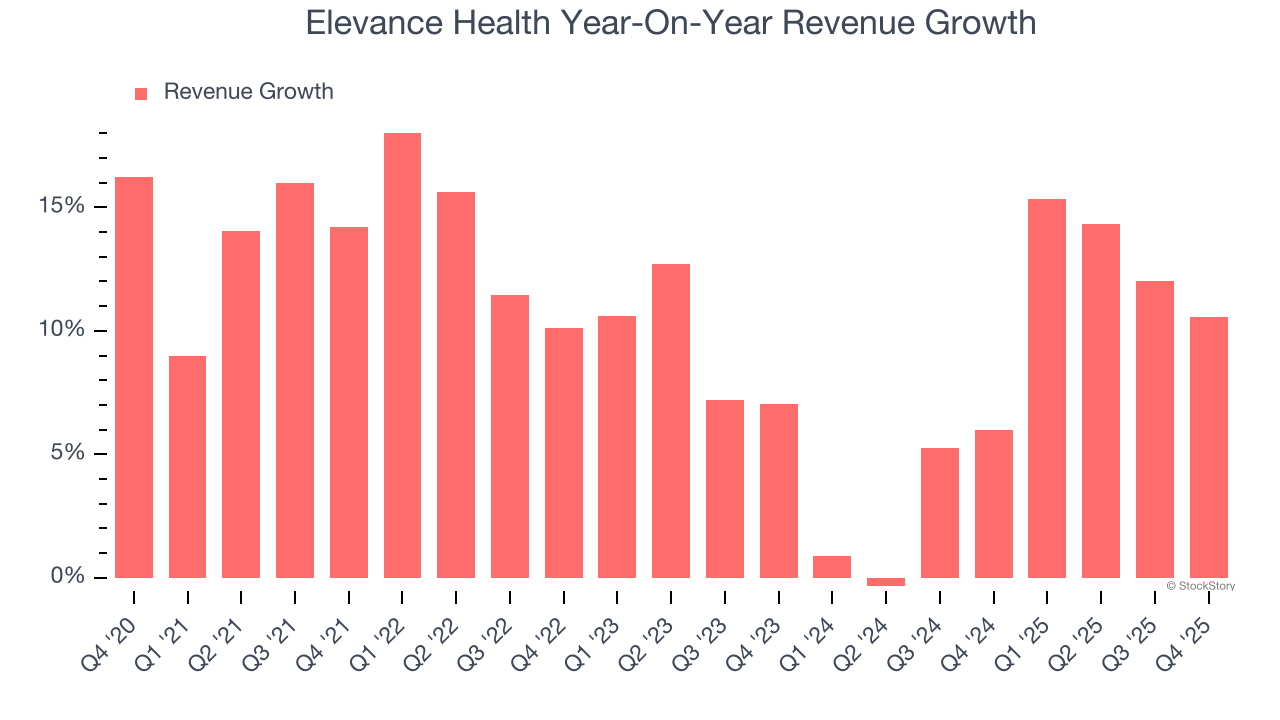

Health insurance provider Elevance Health (NYSE:EVH) met Wall Streets revenue expectations in Q4 CY2025, with sales up 10.6% year on year to $49.75 billion. Its non-GAAP profit of $3.33 per share was 7.7% above analysts’ consensus estimates.

Is now the time to buy Elevance Health? Find out by accessing our full research report, it’s free.

"Elevance Health delivered fourth quarter results in line with our outlook, reflecting disciplined execution in a dynamic environment. As we enter 2026, our focus is on advancing affordability and making healthcare easier to access and navigate for the members we serve. Through pricing discipline and targeted investments, we are strengthening the earnings power of our diversified platform and remain confident in our ability to return to at least 12% adjusted EPS growth in 2027."

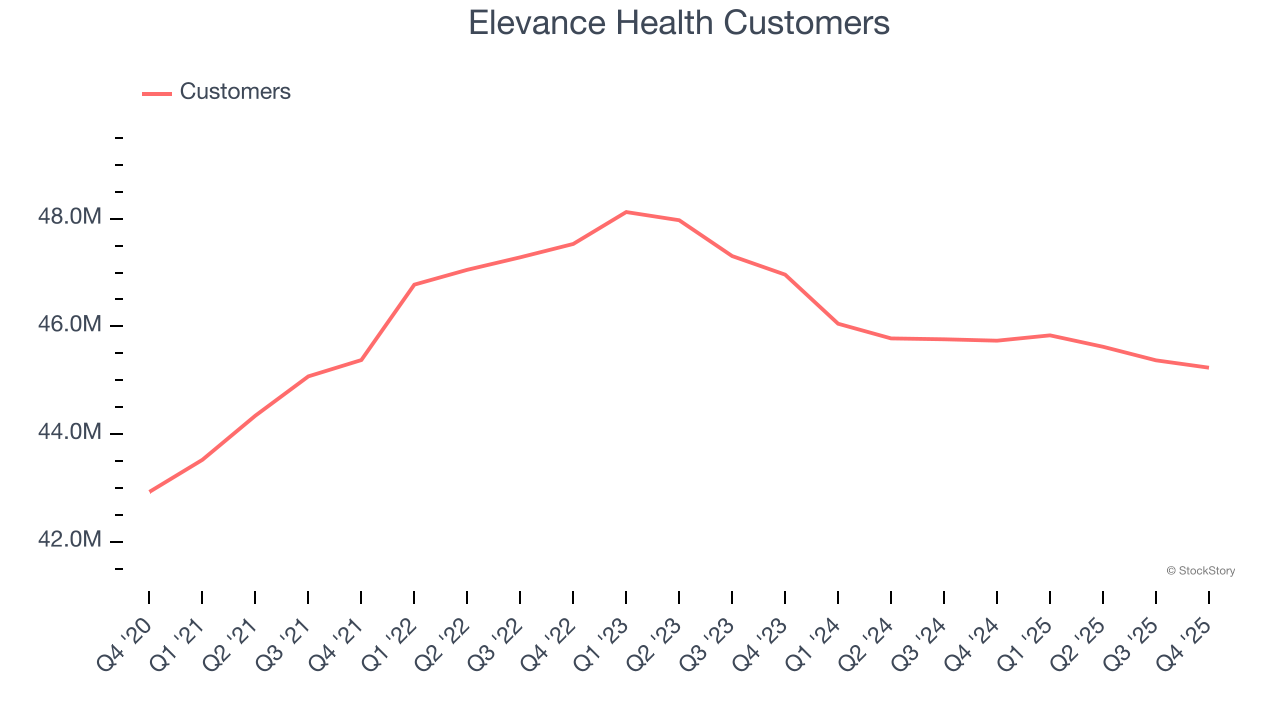

Formerly known as Anthem until its 2022 rebranding, Elevance Health (NYSE:ELV) is one of America's largest health insurers, serving approximately 47 million medical members through its network-based managed care plans.

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Elevance Health’s sales grew at a decent 10.4% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Elevance Health’s annualized revenue growth of 7.9% over the last two years is below its five-year trend, but we still think the results were respectable.

We can dig further into the company’s revenue dynamics by analyzing its number of customers, which reached 45.23 million in the latest quarter. Over the last two years, Elevance Health’s customer base averaged 2.2% year-on-year declines. Because this number is lower than its revenue growth, we can see the average customer spent more money each year on the company’s products and services.

This quarter, Elevance Health’s year-on-year revenue growth was 10.6%, and its $49.75 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

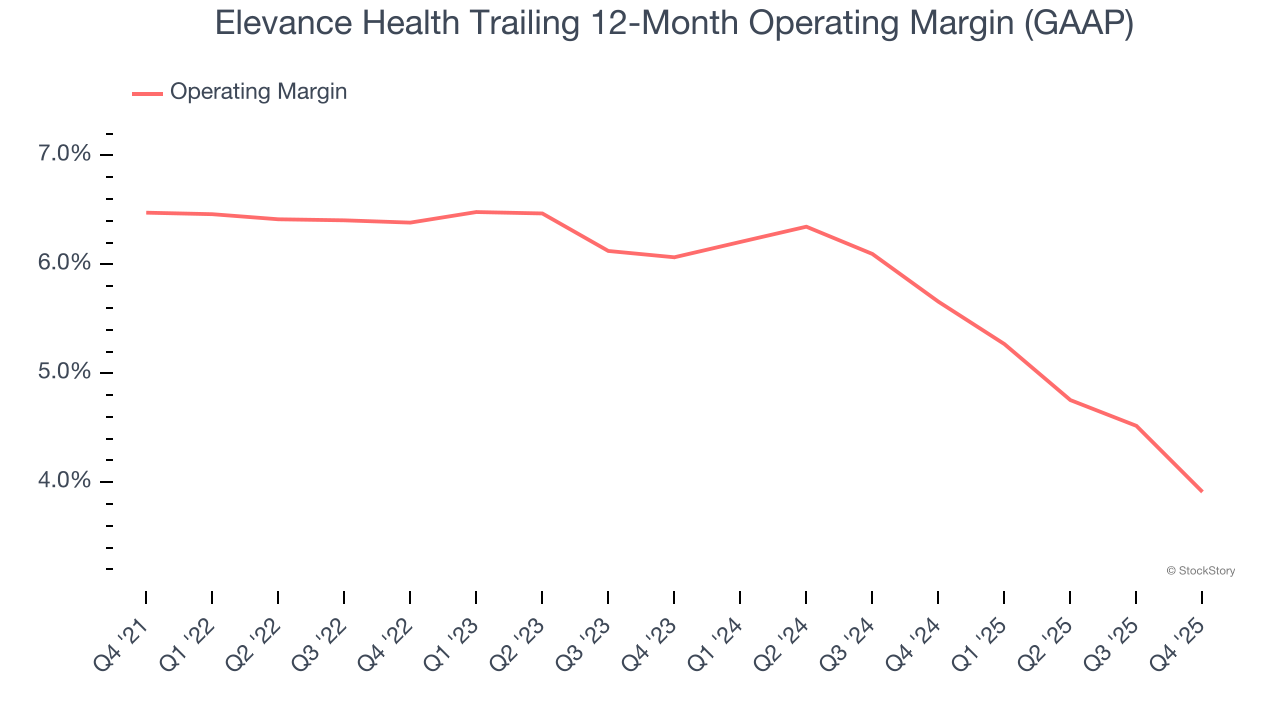

Elevance Health was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.6% was weak for a healthcare business.

Analyzing the trend in its profitability, Elevance Health’s operating margin decreased by 2.6 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 2.2 percentage points. We still like Elevance Health but would like to see some improvement in the future.

In Q4, Elevance Health’s breakeven margin was down 2.2 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

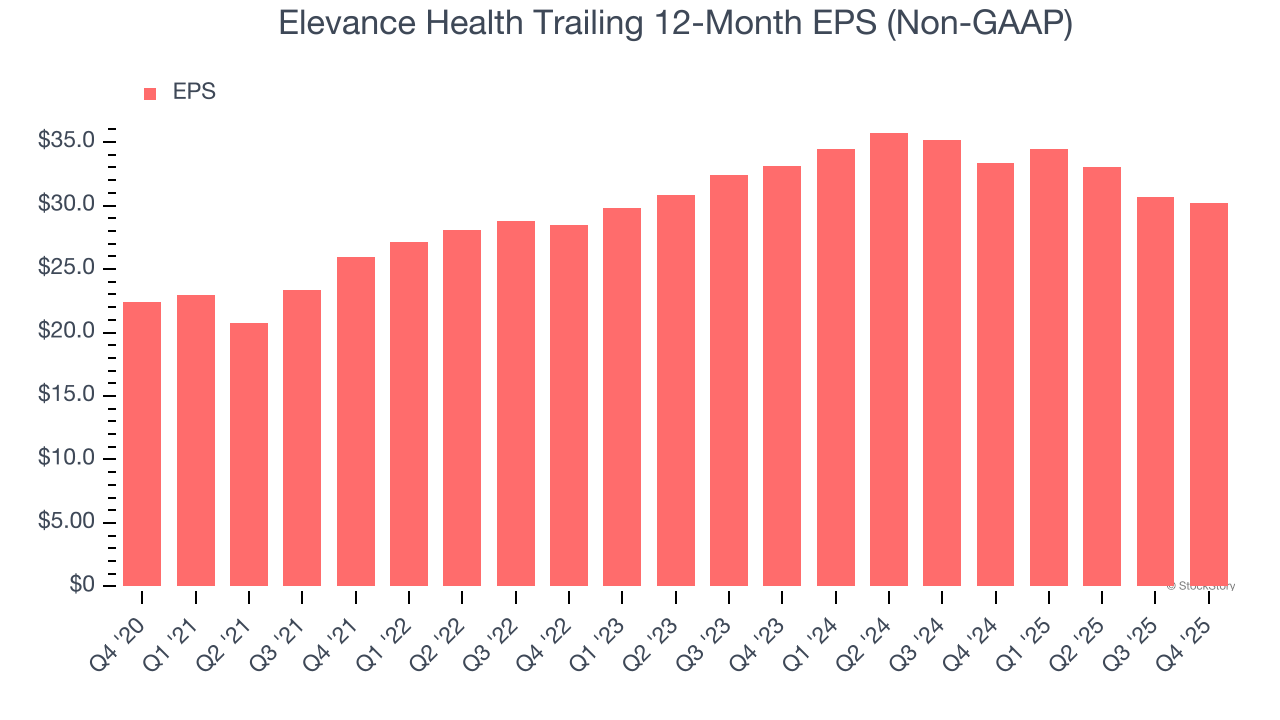

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Elevance Health’s EPS grew at a decent 6.1% compounded annual growth rate over the last five years. However, this performance was lower than its 10.4% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into Elevance Health’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Elevance Health’s operating margin declined by 2.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Elevance Health reported adjusted EPS of $3.33, down from $3.84 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 7.7%. Over the next 12 months, Wall Street expects Elevance Health’s full-year EPS of $30.17 to shrink by 11.4%.

It was good to see Elevance Health beat analysts’ EPS expectations this quarter. On the other hand, its full-year EPS guidance missed and its revenue was only in line with Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 6.7% to $302.06 immediately following the results.

Elevance Health may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| May-20 | |

| May-20 | |

| May-07 | |

| May-04 | |

| Apr-30 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-23 | |

| Apr-23 | |

| Apr-22 | |

| Apr-22 | |

| Apr-22 | |

| Apr-22 | |

| Apr-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite